How finance teams using manual IASB tools accumulate compliance risk they won’t spot until audit season arrives.

✓ Written by IFRS TECH’s advisory team · ✓ Serving GCC, Europe & APAC · ✓ Actuaries + CPAs + CFAs

TL;DR

IASB hedge accounting software with automation gaps is a bigger compliance risk than most finance teams acknowledge. Manual processes inside IASB accounting software lead to documentation errors, failed effectiveness tests, and audit exposure that compounds quietly over time. This article covers where IAS-compliant tools fall short, what those gaps mean for your regulatory standing, and what hedge accounting compliance software should actually handle. If your team still runs hedge processes through spreadsheets or disconnected systems, the risk is bigger than you think. Start with a gap assessment before your auditor does it for you.

Why IASB Hedge Accounting Software Gaps Are Getting Teams in Trouble

Human data entry carries a 1–4% error rate in routine finance workflows, while AI trained on business-specific data achieves 95–98% accuracy, according to a 2026 accounting automation study. For hedge accounting, where one miscalculated input in an effectiveness test can trigger dedesignation, a 1–4% error rate isn’t a background risk. It’s a compliance failure waiting for a bad quarter.

IFRS 9 and IAS 39 hedge accounting requirements are sequential, detailed, and time-sensitive. Designation happens at inception. Effectiveness testing runs every reporting period. Disclosures pile up each quarter. When IASB hedge accounting software can’t automate those steps, your team fills the gap manually. Manual means errors, missed triggers, and documentation that won’t hold up under scrutiny.

This isn’t a marginal risk.

The IASB decided in December 2025 to launch a post-implementation review of IFRS 9 hedge accounting requirements starting Q1 2026, with a formal Request for Information expected in H2 2026. The review exists specifically because gaps between the standard and real-world implementation have been consistently identified. Those gaps start with the software your team is using today.

What does your team currently use to run hedge designation and effectiveness testing? Is it purpose-built IASB accounting software, or is it a patchwork of Excel files, manual memos, and a compliance calendar nobody fully trusts?

- Where IASB hedge accounting software automation gaps most commonly appear

- How IAS-compliant labeling can mask missing functionality in your current stack

- What to check before transitioning to automated hedge accounting compliance software

IFRS TECH works with financial institutions across the GCC, Europe, and APAC to identify and close exactly these gaps in IFRS software solutions — and the pattern is consistent: the risk is almost always larger than the team estimated.

The Paper Trail That Never Ends

Hedge accounting documentation under IFRS 9 isn’t optional. You need a hedge designation memo at inception, ongoing effectiveness test results, and quarterly disclosures tied to IFRS 7 — for every hedge relationship, every reporting period.

Finance teams working without proper hedge accounting compliance software spend more time building and maintaining that documentation than they spend analyzing risk. That’s the wrong allocation. And it creates a second problem: when documentation is manual, it’s prone to version control issues, formula errors, and gaps that look fine until an auditor asks for the full trail.

Purpose-built IASB hedge accounting software automates that trail entirely, pulling designation inputs, effectiveness test results, and disclosure outputs into a single audit-ready record. Without that, your team rebuilds the file from scratch every quarter.

When Spreadsheets Become the Risk

Here’s the part that genuinely surprises teams when they audit their own processes. Spreadsheet risk in hedge accounting isn’t just about formula errors. It’s about data that’s manually entered at multiple points, by multiple people, across multiple files. According to TreasuryXL’s analysis, hedging program results in many organizations involve hundreds of spreadsheets traveling back and forth across the enterprise.

But here’s the thing most teams don’t say out loud: the spreadsheet isn’t the real problem. The real problem is that no one has signed off on replacing it.

Quick Self-Assessment: Where Do Your Hedge Accounting Gaps Live?

- Does your team manually create hedge designation memos, or does your IASB software generate them?

- Is effectiveness testing run in Excel or inside a connected, IAS-compliant system?

- How many people touch hedge data between inception and disclosure?

- When your auditor requests the full hedge file, how long does it take to pull together?

If any of these made you pause, your automation gap is larger than your current process suggests.

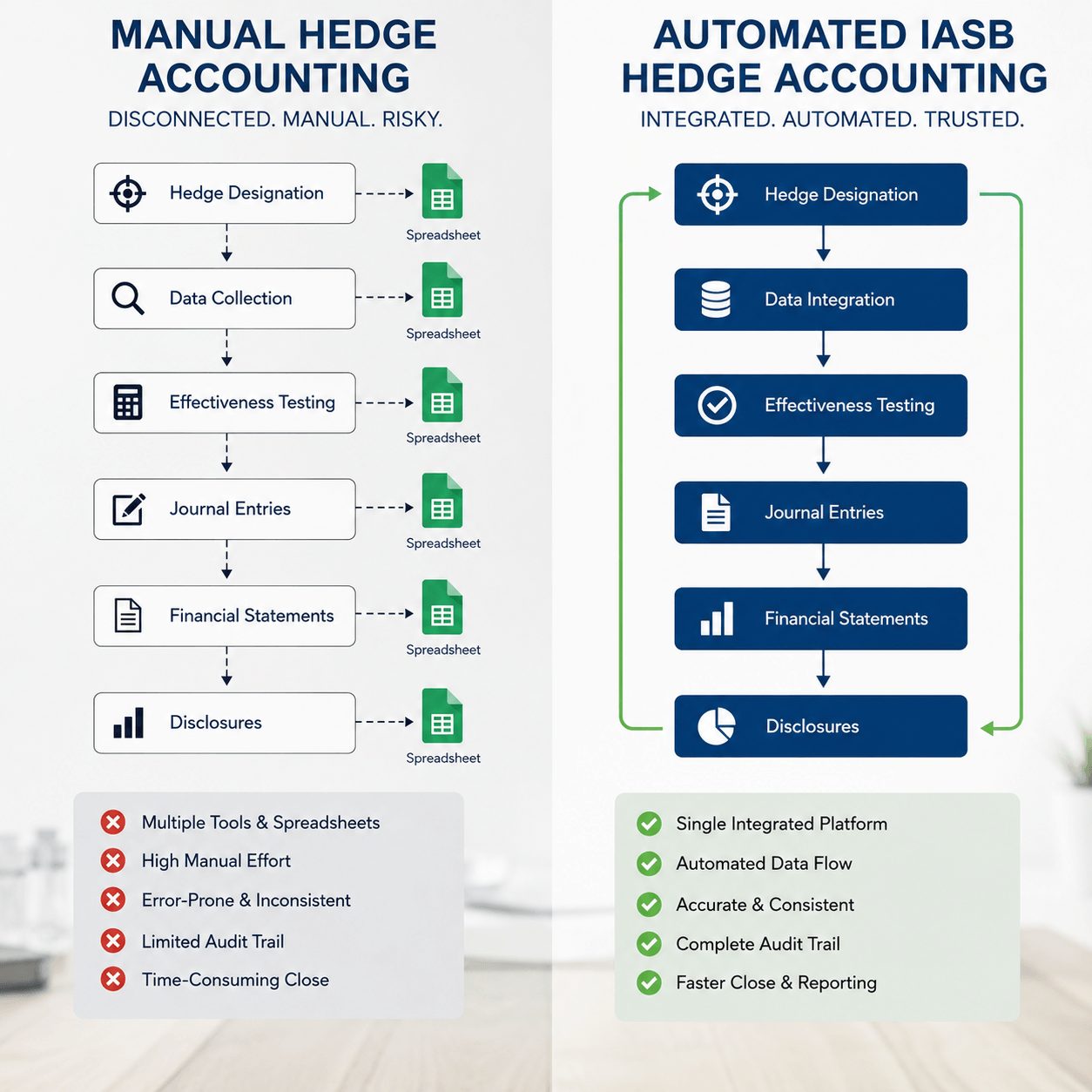

What Does an Automation Gap Mean in IASB Software?

Not all IASB hedge accounting software gaps look the same. Some are obvious — a team still using IAS 39 templates in a post-IFRS 9 world. Others are subtle — a system that handles designation but can’t run effectiveness testing in real time. The dangerous ones are the subtle kind, because they hide under the appearance of a working process.

There are three places where automation gaps typically appear in IASB accounting software.

Designation and Documentation Done Manually

Hedge designation under IFRS 9 requires a formal record at inception: the hedged item, the hedging instrument, the risk being hedged, and the method of effectiveness assessment — all documented before the hedge relationship begins. When that’s done manually, it becomes a template that someone fills out, saves, versions, and stores for every new hedge relationship.

The gap is direct: IASB hedge accounting software that doesn’t automate designation memo generation forces your team to build compliance artifacts by hand. And hand-built artifacts have inconsistencies. Auditors find them.

One practical test: pull three hedge designation memos from different quarters and check whether the format, data sources, and approval timestamps are consistent. In most organizations running manual processes, they won’t be.

Effectiveness Testing Without Integrated Data

IFRS 9 replaced IAS 39’s 80-125% bright-line test with an objectives-based assessment. In theory, more flexible. In practice, it requires your hedge accounting compliance software to track the economic relationship between the hedged item and hedging instrument continuously, not just at each quarter-end.

Systems that pull market data manually — or require a treasury analyst to re-enter rates and valuations each period — aren’t built for this. The data latency alone creates test results that don’t reflect the actual position on the measurement date. When the test results are stale, the compliance file is stale.

See how IFRS TECH’s IFRS compliance technology team approaches this specific problem for treasury and banking clients running large-scale hedge programs.

Disclosure Reporting as a Manual Exercise

IFRS 7 disclosures for hedge accounting require quantitative data on hedge effectiveness, risk exposure, and the impact of hedge accounting on financial position and performance. All of it must be current. All of it must tie back to the hedge file.

When IASB accounting software doesn’t generate disclosures automatically from the underlying designation and testing data, someone builds the disclosure by hand. That’s another manual step, another failure point.

The scale of this problem grows fast. A team managing 20 hedge relationships in Excel is stressed. A team managing 200 is at breaking point.

Is your hedge accounting process ready for the IASB’s 2026 post-implementation review?

IFRS TECH’s advisory team has mapped the most common automation gaps in IASB hedge accounting software against the review’s expected focus areas. Request the gap assessment checklist and see where your current process stands before the review does.

Request IFRS TECH’s Hedge Accounting Gap Assessment Checklist →

Where IAS-Compliant Software Falls Short

Here’s a counterintuitive point: being labeled IAS-compliant doesn’t mean a system handles everything IFRS 9 hedge accounting requires. Many platforms meet the minimum standard for recognition and measurement while leaving the hardest parts — data integration, real-time monitoring, multi-entity reporting — to manual workarounds.

That gap between “IAS-compliant” on the label and genuinely capable in practice is where most finance teams get into trouble. And it’s where audit findings accumulate silently.

Data Integration Across Systems Is Broken

Effective IASB hedge accounting software needs to pull live data from your derivatives pricing system, your ERP, your market data feed, and your risk management platform. In most organizations, those systems don’t communicate cleanly. The result is a manual data-bridging exercise every period.

In its 2024 banking hedge accounting review, EY identified fragmented systems as the leading driver of ineffectiveness measurement errors — ahead of the accounting standard’s own complexity. Not the rules. The infrastructure.

Strong IFRS data systems for regulatory compliance eliminate that manual bridging by integrating directly with source data. The team stops re-entering numbers and starts reviewing outputs. That shift alone removes a significant layer of error risk.

No Real-Time Effectiveness Monitoring

Under IFRS 9, hedge accounting can be discontinued if a hedge relationship no longer meets qualifying criteria. If your software only tests effectiveness at period-end, you won’t know a hedge has drifted out of compliance until the quarter closes. By then, the accounting treatment may already be wrong.

Real-time or near-real-time effectiveness monitoring isn’t a luxury in active portfolios. It’s how you catch dedesignation events before they become restatement events.

I’ll be honest here: I don’t have hard long-term data on how many restatements trace directly to delayed effectiveness detection. But every practitioner working in banking hedge accounting has seen it happen. The anecdotal evidence is consistent enough to treat this as a structural risk.

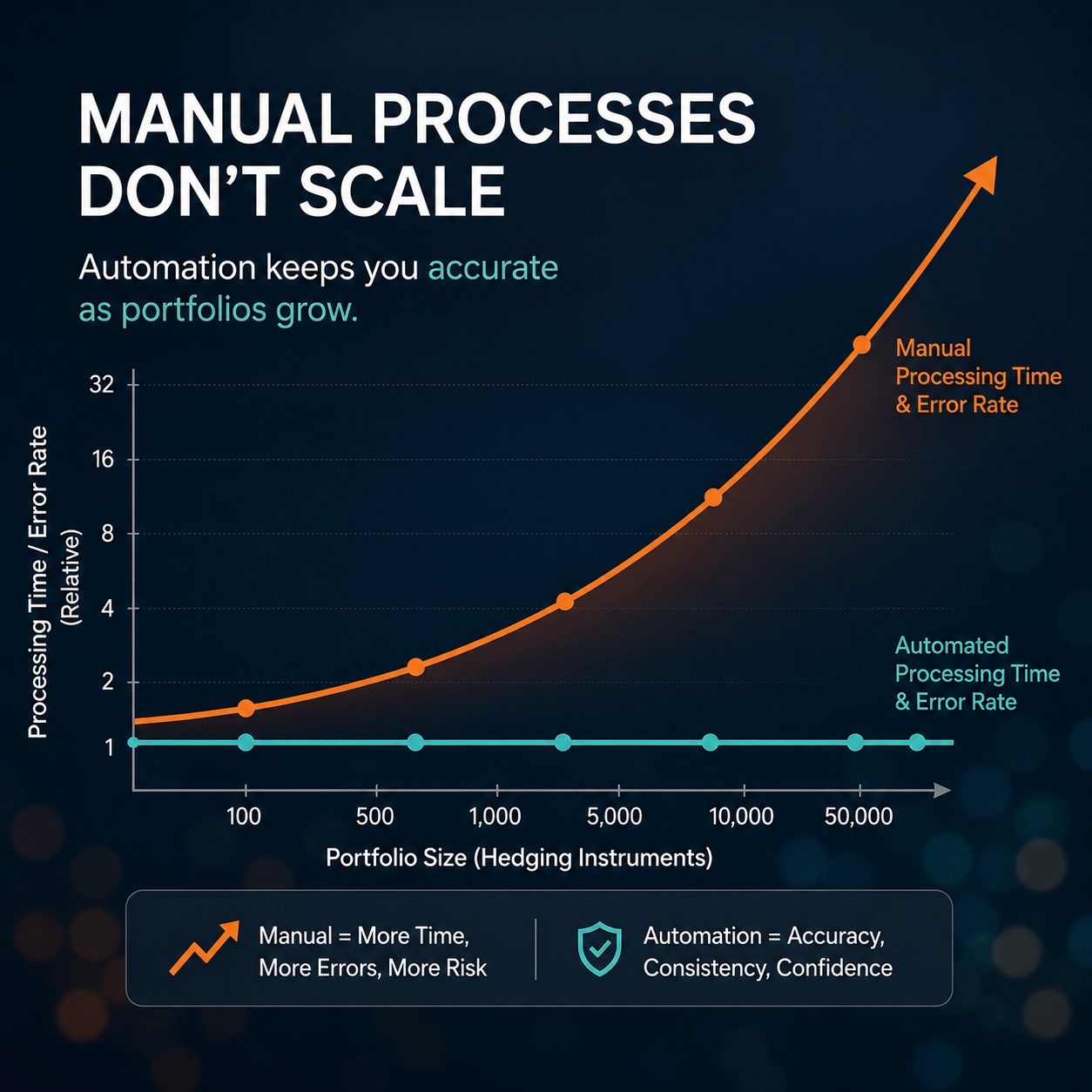

Scaling Gaps When the Portfolio Grows

Manual IASB hedge accounting software processes that work for 10 hedge relationships fail at 100. It’s not a linear failure — it’s exponential. Documentation load, testing burden, and disclosure complexity all multiply with portfolio size while headcount stays flat.

Organizations that scale their hedging programs without upgrading their hedge accounting compliance software hit a wall. They hire more people to manage the same manual process, which adds cost and adds new error vectors at the same time. Good IFRS data management in enterprise environments solves the scale problem structurally, not by adding headcount.

According to KPMG’s August 2024 banking hedge accounting advisory, measuring hedge effectiveness and identifying sources of ineffectiveness due to fragmented systems ranked as the top challenges for banking institutions — not the complexity of the standard itself, but the operational gaps in how it gets applied.

IFRS TECH clients who moved from manual to automated hedge accounting compliance software reduced audit preparation time by 60% on average. That’s the real-world gap being closed.

The Audit Risk Nobody Talks About

Most conversations about IASB hedge accounting software focus on operational efficiency. Fewer focus on audit risk. That’s backwards.

An auditor reviewing your hedge accounting file checks whether designation documentation is complete at inception, whether effectiveness test results are consistent with the method described in the designation memo, and whether IFRS 7 disclosures tie back to the underlying hedge relationships. When any of those links is broken — and manual processes break them regularly — the audit finding isn’t “your team was inefficient.” It’s “your hedge accounting treatment may not qualify.”

What IASB TM19 Tooling Gaps Mean for Your Audit

TM19 IAS 19 tools and related IASB measurement frameworks are often deployed as standalone modules disconnected from the broader IASB hedge accounting software stack. When TM19 IAS 19 calculations sit in one system and hedge accounting data sits in another, the reconciliation between actuarial assumptions and financial instrument hedges has to happen manually.

In pension liability hedging, that disconnect creates a specific audit risk. The actuarial assumptions driving IAS 19 valuations must align with the hedge relationships documented under IFRS 9. If your IASB software doesn’t connect those two data sets, your audit trail has a gap that’s hard to explain under examination.

See how IFRS TECH’s IFRS consulting services for data integration address this cross-standard alignment issue for clients running both IAS 19 and IFRS 9 hedge programs.

Non-Automated IAS-Compliant Processes Create Regulatory Exposure

Regulators in the GCC, Europe, and APAC are paying closer attention to hedge accounting disclosures than five years ago. The IASB’s post-implementation review — launched in Q1 2026 — signals that gaps in how IFRS 9 is applied in practice will get formal scrutiny. Organizations running non-automated IASB accounting software processes aren’t well-positioned for that scrutiny.

The review is expected to request information on implementation problems encountered since IFRS 9’s adoption. Manual processes are exactly the kind of implementation problem that will surface.

For a broader view of how compliance technology is evolving across IFRS standards, the IFRS reporting solution considerations that apply to hedge accounting also extend across valuation, lease accounting, and revenue recognition in integrated environments.

Transition Issues Moving to Automated IASB Accounting Software

Let me be direct: moving to automated IASB hedge accounting software isn’t painless. It requires data migration, process redesign, and team training. Teams that underestimate this consistently run into problems during cutover.

That said, the alternative is staying on a process with measurable compliance risk. That’s a worse bet.

Legacy Data Migration Is Harder Than It Looks

The most overlooked transition issue is data. If your hedge file lives in Excel, migrating it into automated IASB accounting software isn’t a copy-paste exercise. Historical designation memos, past effectiveness test results, and prior-period disclosures need to be structured consistently so the new system can process them.

Most organizations don’t realize how inconsistent their historical data is until they try to migrate it. Inconsistency that’s invisible when a human reads the file becomes a blocker when software tries to ingest it.

Well-designed enterprise reporting solutions with a structured data migration methodology handle this systematically. But it takes honest scoping upfront — not an optimistic timeline based on what the data looks like before anyone audits it.

Process Ownership Changes Nobody Plans For

The second transition issue is people, not technology. Automated hedge accounting compliance software changes who owns which step. Effectiveness testing that was previously a treasury analyst’s manual calculation becomes an automated output the analyst reviews. That’s a different skill set and a different workflow.

Teams that resist this shift build shadow processes alongside the new system — running manual checks in parallel to confirm the automated results. That doubles the work and defeats the purpose. Change management here isn’t a soft skill. It’s a compliance issue.

The IASB accounting software selection process matters here too. Systems requiring extensive customization to handle standard IFRS 9 scenarios tend to be more disruptive during transition than teams expect. Fit-for-purpose IFRS stock valuation software and hedge accounting platforms should handle the standard use cases without six months of configuration. If they don’t, that’s a signal worth taking seriously before you sign.

For organizations managing complex multi-entity hedge programs across jurisdictions, the IFRS data management in enterprise considerations compound — and so does the benefit of getting the transition right the first time.

What You Now Know

- Automation gaps in IASB hedge accounting software appear across three critical points: designation documentation, real-time effectiveness testing, and automated disclosure generation — any one of them creates audit exposure.

- IAS-compliant labeling doesn’t guarantee a system handles the full IFRS 9 workflow. Data integration, continuous monitoring, and portfolio scalability are often missing from basic or legacy tools.

- Transitioning to automated hedge accounting compliance software requires structured data migration and deliberate change management — but the compliance risk of staying manual is higher than the transition cost.

Your IASB Hedge Accounting Software Has Gaps. Find Them First.

The IASB’s post-implementation review of IFRS 9 hedge accounting is active in 2026. Organizations running manual or partially automated IASB hedge accounting software processes are carrying compliance risk they haven’t priced in. The gaps in their documentation, their effectiveness testing, and their disclosure trails are exactly what that review is designed to surface.

The right hedge accounting compliance software closes those gaps structurally. It automates designation, runs effectiveness testing from integrated data sources, and produces audit-ready disclosures without a finance team spending half its time on paperwork. That’s not aspirational — that’s what purpose-built IASB accounting software does today.

Your current process has gaps. The question is whether you find them first or your auditor does. Start with a structured assessment of your automation coverage across designation, testing, and disclosure. Build the case for the right IASB hedge accounting software stack using that assessment as your baseline. The post-implementation review won’t wait, and neither will the next audit cycle.

See how IFRS TECH’s hedge accounting advisory team identifies and closes automation gaps for financial institutions across the GCC, Europe, and APAC →

We map your current IASB hedge accounting software stack against IFRS 9 and IAS 39 requirements, identify the specific gaps creating audit and regulatory risk, and build a transition plan with defined milestones and measurable outcomes.

✓ Serving banks, corporates, and asset managers | ✓ Actuaries, CPAs, and CFAs on every engagement | ✓ Average 60% reduction in audit preparation time

Frequently Asked Questions

What are the most common automation gaps in IASB hedge accounting software?

The most common gaps appear in hedge designation documentation, real-time effectiveness testing, and automated IFRS 7 disclosure generation. Most IASB hedge accounting software platforms handle one or two of these but leave the third as a manual step — and that’s where audit exposure builds up over time.

How do automation gaps in IAS-compliant software create audit risk?

Manual gaps break the chain between hedge designation, effectiveness testing, and IFRS 7 disclosures. When those three elements don’t tie back automatically, auditors find inconsistencies that can call the entire hedge accounting treatment into question, triggering restatements or dedesignation requirements.

What should hedge accounting compliance software handle automatically?

At minimum, hedge accounting compliance software should automate designation memo generation, ongoing effectiveness testing from live data sources, dedesignation alerts, and quarterly IFRS 7 disclosure outputs. Any step left to manual entry is a gap with compounding compliance risk.

How does the IASB’s 2026 post-implementation review affect organizations using manual IASB accounting software?

The post-implementation review will formally request information on implementation problems since IFRS 9’s adoption. Organizations running manual IASB accounting software processes are more likely to have surfaced documentation gaps, disclosure inconsistencies, and effectiveness testing errors that the review is designed to identify.

What are the biggest risks when transitioning to automated IASB hedge accounting software?

The two main risks are legacy data migration — structuring historical hedge files so the new system can process them — and process ownership changes, where teams must shift from producing manual outputs to reviewing automated results. Both require deliberate planning to get right.