TL;DR

Hidden audit risks in IFRS 9 spreadsheets rarely show up in the numbers. They show up in the gaps around the numbers, missing approval trails, broken links, overlays nobody can defend six months later. Ninety four percent of business spreadsheets carry critical errors, and auditors know it. This guide walks through where those risks live: staging logic, PD and LGD assumptions, management overlays, and the audit trail your spreadsheet was never built to keep. If your ECL model still lives in Excel, read this before your next review.

Finance teams chase calculation accuracy. Auditors want something else entirely: proof.

Proof that your probability of default model hasn’t changed since last quarter. Proof that the analyst who applied a management overlay got sign-off first. Proof that the number on the screen matches the number that fed into it three spreadsheets ago.

Spreadsheets don’t keep that proof. That’s the real problem, and it’s why finance teams get blindsided by findings they thought their calculations had already answered.

Hidden Audit Risks in IFRS 9 Spreadsheets Finance Teams Miss

IAS 39 asked for evidence of loss. IFRS 9 asks for a forecast, and forecasts need a paper trail that spreadsheets weren’t built to hold.

Your PD model can be technically sound and still fail review, because auditors aren’t testing the model. They’re testing whether you can prove nobody touched it without approval.

94% of spreadsheets used in business decision-making contain critical errors, according to recent research. That’s not a rounding risk. That’s the baseline assumption an auditor walks in with.

Auditors now expect documented model validation, tested assumptions, and a justification for every override. Spreadsheets don’t generate that evidence on their own. Somebody has to manually reconstruct it, usually during the two weeks before the audit deadline.

Why IFRS 9 Spreadsheet Errors Trigger Audit Findings

Every copy-paste, every manual override, every adjusted formula is a chance for something to go wrong quietly. These errors rarely look wrong. That’s what makes them dangerous.

140 public companies reported unreliable prior financial statements in the first ten months of 2024, many tracing back to spreadsheet-based reporting. Not all IFRS 9 specifically. Still, the pattern holds: manual systems create weaknesses auditors are trained to hunt for.

It gets worse once teams start splitting the workload. One workbook for PD, another for LGD, a third that stitches both into lifetime ECL. Auditors need to trace the whole chain, raw data to financial statement line. Across three linked files with manual handoffs, that chain is basically untraceable.

What Auditors Look for in IFRS 9 Models

Consistency, first. Did your significant-increase-in-credit-risk criteria stay the same across every exposure, all period? Can you prove the formula that ran in March is the same one that ran in November?

Model governance sits at the center of this. Auditors want formal approval trails for every parameter change. Spreadsheets don’t have workflows, so teams fall back on email threads and meeting notes as their evidence. That rarely satisfies anyone reviewing the file six months later.

The European Banking Authority found nearly 40% of institutions used 12-month PD as a proxy for lifetime PD in SICR assessment. Workable in Excel. Defensible only with documentation spreadsheets don’t generate on their own.

Teams benchmarking their approach against IFRS 9 best practices and compliance frameworks tend to find the documentation gap before they find the calculation gap.

How PD, LGD, and ECL Errors Start in Spreadsheets

PD modeling pushes Excel past what it’s good at. Multiple linked sheets, historical default data, macro variables, adjustment factors, each link a place for something to slip.

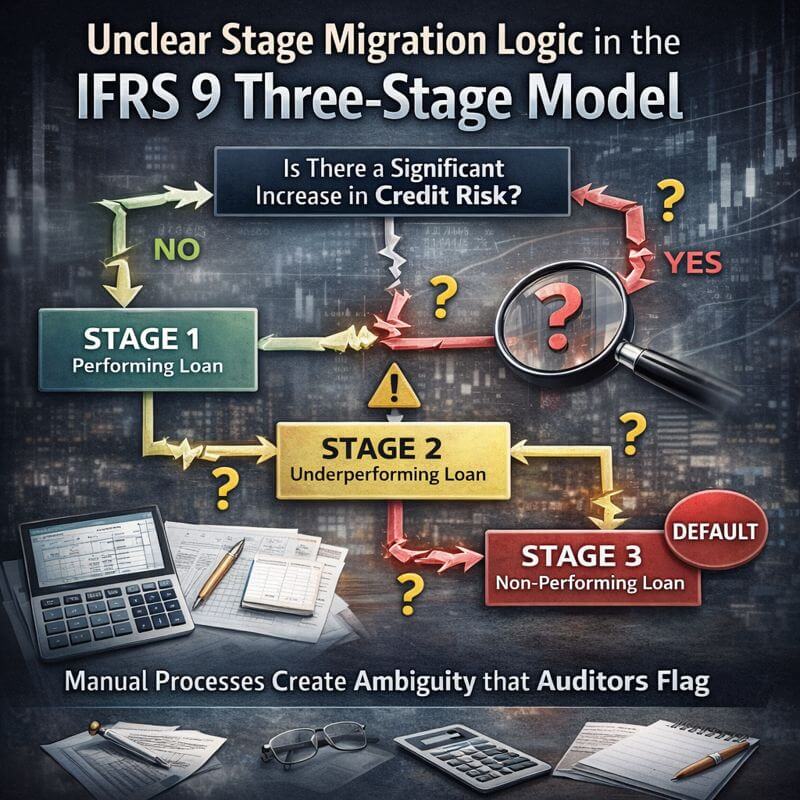

The same EBA review found 3% of exposures stayed in Stage 1 despite a threefold PD increase since origination. Staging logic that doesn’t catch deterioration is a documentation problem wearing a calculation costume.

LGD carries its own weight: collateral values, recovery rates, workout timeframes, all needing regular refresh. Keep that consistent across five spreadsheets and you’ve got yourself a full time job that isn’t in anyone’s title.

ECL then multiplies PD and LGD by exposure, discounts to present value, and folds in revolving facilities and prepayment assumptions on top. The formula that tries to do all of that in one cell is usually the formula nobody can fully explain during testing. Teams comparing that mess against structured IFRS 9 software built for banks usually start the conversation right here.

How Small Spreadsheet Errors Create Big IFRS 9 Audit Issues

One misplaced decimal. One wrong cell reference. Neither trips an alarm if the output still looks plausible. Auditors find these during sample testing, and then they start asking about everything else too.

41% of finance teams report trouble identifying and correcting spreadsheet errors, per recent CFO surveys. Tracing one error across dozens of linked worksheets is its own project.

Small errors compound. Auditors don’t look at them one at a time, they add them up. Enough small errors and the conclusion isn’t “a few mistakes,” it’s “controls aren’t operating.”

Missing Documentation and Model Assumptions

You need to explain your macro variable choices. Justify your SICR thresholds. Document the link between discount rates and effective interest rates. None of that lives inside a spreadsheet naturally, so it ends up scattered across separate Word files nobody updates in sync with the model.

Model validation has the same problem. Back testing, sensitivity checks, benchmark comparisons, all expected, none of it structured. Understanding how IFRS 9 forward-looking provisions should be documented is usually the moment teams realize how thin their current process actually is.

Broken Links and Uncontrolled Formulas

External link dependencies are the quiet killer. Move a file, rename it, and the model keeps showing cached numbers like nothing happened. Auditors testing data integrity find this fast, and it never reads well.

Nine out of ten spreadsheets over 150 rows contain errors, per recent operational risk data. IFRS 9 files run into the thousands of rows. At that scale, the odds of a clean spreadsheet approach zero.

Manual Overrides with No Review History

Overlays exist because models miss emerging risk. Fair enough. But when an analyst adjusts an ECL figure by hand, that edit leaves no trail. You might remember the reason today. Will you remember it during next year’s audit?

The EBA found overlays made up 26.3% of ECL on average for corporate portfolios. A quarter of your provision, running on judgment nobody can trace back to an approval. That’s the number auditors zero in on first.

Inconsistent Staging and Risk Classification

Stage 1 gets 12-month ECL. Stage 2 and 3 get lifetime loss. Getting that classification right, consistently, across thousands of exposures, is where nested IF statements start to buckle.

Backstop rules like 30-days-past-due should trigger automatic migration. Spreadsheets can encode that. Proving it actually fired correctly for every exposure, every period, is a different exercise entirely, and one most finance teams haven’t run.

Why IFRS 9 Spreadsheets Fail Under Audit Scrutiny

Auditors test two things: did the control stop the error, and did someone catch it if it slipped through. Spreadsheets tend to score poorly on both.

Anyone with file access can change a formula. No segregation of duties, no technical barrier between preparer and reviewer. That alone is enough for most auditors to flag control design as deficient before they’ve even opened the file.

Historical validation is its own headache. Overwrite last quarter’s file with this quarter’s update, and you’ve erased the evidence that would prove consistent methodology across periods.

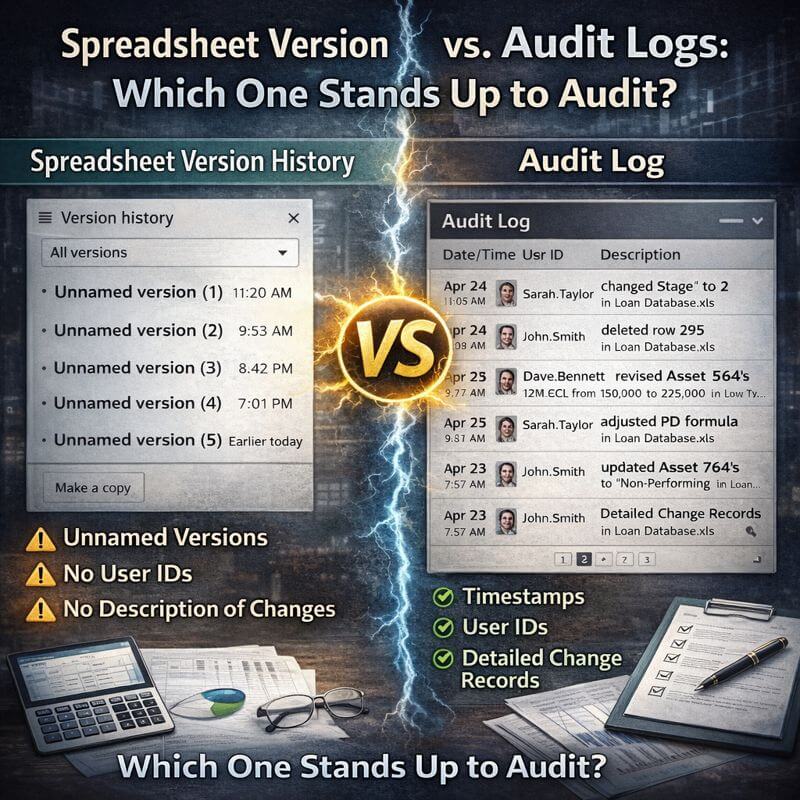

Lack of Audit Trails in IFRS 9 Spreadsheet Models

A real audit trail shows what changed, when, by whom, and why. Spreadsheets weren’t built for that, and it shows.

File names like “ECL_Model_v3_final_revised.xlsx” pass for version control in most finance teams. Multiple analysts, multiple versions, and suddenly nobody’s sure which file is the official one. Auditors find three versions with three different results and ask the obvious question.

Changes take effect the moment someone edits a cell. No review step, no approval gate, no migration process. Compare that to any controlled system and the gap becomes the finding.

Version Control and Data Integrity Risks in IFRS 9

Two analysts, one workbook, two sets of changes running at once. Without proper version control, that’s not collaboration, it’s a data integrity incident waiting to surface at month end.

Email-based file sharing doesn’t help. Files ping-pong for review, diverge, and reconciling which version has every update becomes detective work nobody signed up for.

Digital disruption ranked third among top risks in North America, cited by 48% of audit leaders, up 12 points from the prior year. IFRS 9 spreadsheet processes sit right in that blast radius.

How Outdated Data Impacts IFRS 9 Impairment Results

IFRS 9 wants current forecasts, recent default observations, fresh collateral values. Spreadsheets tend to run on whatever data someone last remembered to update.

Forget to refresh GDP assumptions in one tab while updating another, and your ECL runs on two different economic stories at once. Auditors catch this fast, because it never adds up cleanly.

The same cybersecurity concerns cited as the top risk by 88% of respondents extend inward too. Weak access control isn’t just an external threat model, it’s an internal one, and auditors have started treating it that way.

What Makes IFRS 9 Spreadsheet Models Hard to Defend

Models built organically over years by whoever was around at the time are hard to explain, mostly because the person who built the original logic left the company two reorgs ago.

A formula spanning six nested functions in one cell isn’t sophistication, it’s a liability during testing. Auditors will ask you to simplify it or rebuild it, and either way that’s more hours nobody budgeted for.

I’ll admit a limit here. I don’t have a clean industry figure for how many hours finance teams lose reconstructing methodology history during audits. Every engagement I’ve seen where this came up, though, it ate at least a week.

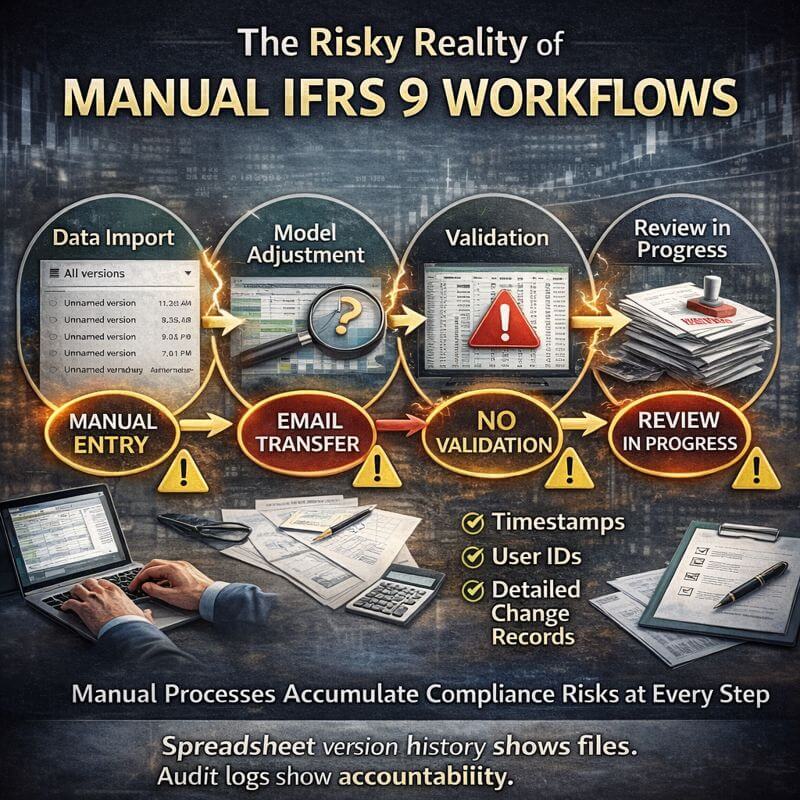

Why Manual IFRS 9 ECL Models Increase Compliance Risk

Every manual step is a place an error can enter or a control can fail. Stack enough of them and the accumulated risk outpaces what most finance teams think they’re carrying.

Key-person dependency is real here too. When one or two people understand the spreadsheet logic completely, their vacation becomes a reporting risk. Auditors read that concentration as a control gap, not a staffing footnote.

Regulatory expectations have moved since IFRS 9 first landed. Regulators now want sharper overlay governance and more rigorous validation than most spreadsheet processes were ever designed to deliver. Finance teams weighing the move from manual work to dedicated IFRS 9 compliance software are usually responding to exactly this pressure.

Spreadsheet Limitations in IFRS 9 Credit Risk Management

Portfolios grow. Spreadsheets don’t scale with them. Tens of thousands of exposures later, teams are running calculations overnight and hoping the file doesn’t crash before morning.

Scenario weighting multiplies the load further. Multiple economic scenarios, each probability-weighted, each requiring either sequential processing that eats days or manual copying that spawns yet more version control chaos.

None of this makes audits faster either. A model that takes hours to run is a model auditors can’t sample-test efficiently, so they lean harder on substantive testing instead of trusting your controls.

How Finance Teams Detect Hidden IFRS 9 Audit Risks

Internal control reviews before the external audit starts catch a surprising amount. Reconciliations between periods surface calculation drift early. Bringing in outside eyes, consultants, internal audit, tends to surface documentation and overlay gaps that the team living inside the spreadsheet stopped noticing months ago.

Benchmark against peer institutions too. If most comparable organizations have moved past manual spreadsheets and you haven’t, that gap is itself a finding waiting to happen.

When IFRS 9 Spreadsheets Stop Scaling for Banks and Lenders

Regulatory reporting keeps getting more granular. Audit committees ask sharper questions about overlay governance. Close cycles keep getting squeezed toward days instead of weeks.

Portfolio acquisitions are the real stress test. Folding an acquired book into an existing spreadsheet-based ECL model, one built from years of linked files, is about as clean as it sounds. Teams planning for that kind of growth are usually the first ones to seriously look at modern IFRS 9 software built for scale.

Frequently Asked Questions

Free Product Demo

See Rust IFRS 9 handle your audit trail live.

IFRS Tech’s advisors walk you through Rust IFRS 9’s ECL engine on your data. First demo is always free, no pitch, just the product.

Building Audit-Ready Processes That Stand Up to Scrutiny

The hidden audit risks in IFRS 9 spreadsheets rarely start as calculation errors. They start as gaps nobody’s tracking: an approval that never got written down, a link that quietly broke, an overlay whose rationale lives only in someone’s memory.

Ninety four percent of business spreadsheets carry critical errors. That statistic alone should worry anyone still running material financial reporting through Excel.

Version control failures, missing audit trails, undocumented judgment calls. Add them up and you get exactly the kind of finding external auditors are trained to catch. Teams that fix these before the review, not during it, walk into audits with far less friction.

Whether you’re weighing the build vs buy IFRS 9 software TCO question or comparing enterprise IFRS 9 ECL software options, the spreadsheet gaps above are usually what tips the decision.

Explore our IFRS software solutions

Prima Consulting helps organizations pressure-test their IFRS 9 process before regulators do it for them. Connect with Prima Consulting to assess where your current process actually stands.