Best Practices for Vetting Valuation Management Software Providers

How GCC finance teams can avoid costly vendor mistakes by testing for accuracy, compliance depth, and real IAS 19 capability before signing anything.

✓ Written by IFRS TECH’s advisory team · ✓ Serving GCC, Europe & APAC · ✓ Actuaries + CPAs + CFAs

TL;DR

Vetting valuation management software providers poorly is one of the most expensive mistakes a finance team makes — and it rarely shows up on the P&L until audit season. This article covers how to test for accuracy in real-time valuation software, which red flags most procurement teams miss entirely, and the specific compliance requirements for end of service benefits valuation in the Middle East. It also gives you a working checklist to run before any vendor conversation turns into a contract. Use it before you commit.

Pick the wrong valuation management software provider and you won’t know for six to eighteen months. By then, your IAS 19 disclosures are out, your auditors have questions you can’t answer cleanly, and you’re looking at a migration mid-reporting cycle. That’s not a hypothetical — it’s the pattern IFRS TECH sees across clients who come to us after a vendor disappointment.

The GCC market makes this worse. IFRS compliance expectations are tightening. GCC regional GDP is projected to accelerate to 4.1% in 2026, driving more scrutiny on financial disclosures and asset valuations. Regulators in Saudi Arabia and the UAE aren’t slowing down on enforcement. And most valuation management software providers are still selling on features — not proving accuracy.

This article covers three things:

- How to test valuation accuracy before you buy, not after

- The red flags most procurement checklists don’t catch

- What end of service benefits valuation in the Middle East demands from any platform you consider

IFRS TECH’s advisory team works across actuarial, accounting, and technology and the vendor mistakes we see most often are entirely preventable.

Why Choosing the Wrong Valuation Management Software Costs More Than You Think

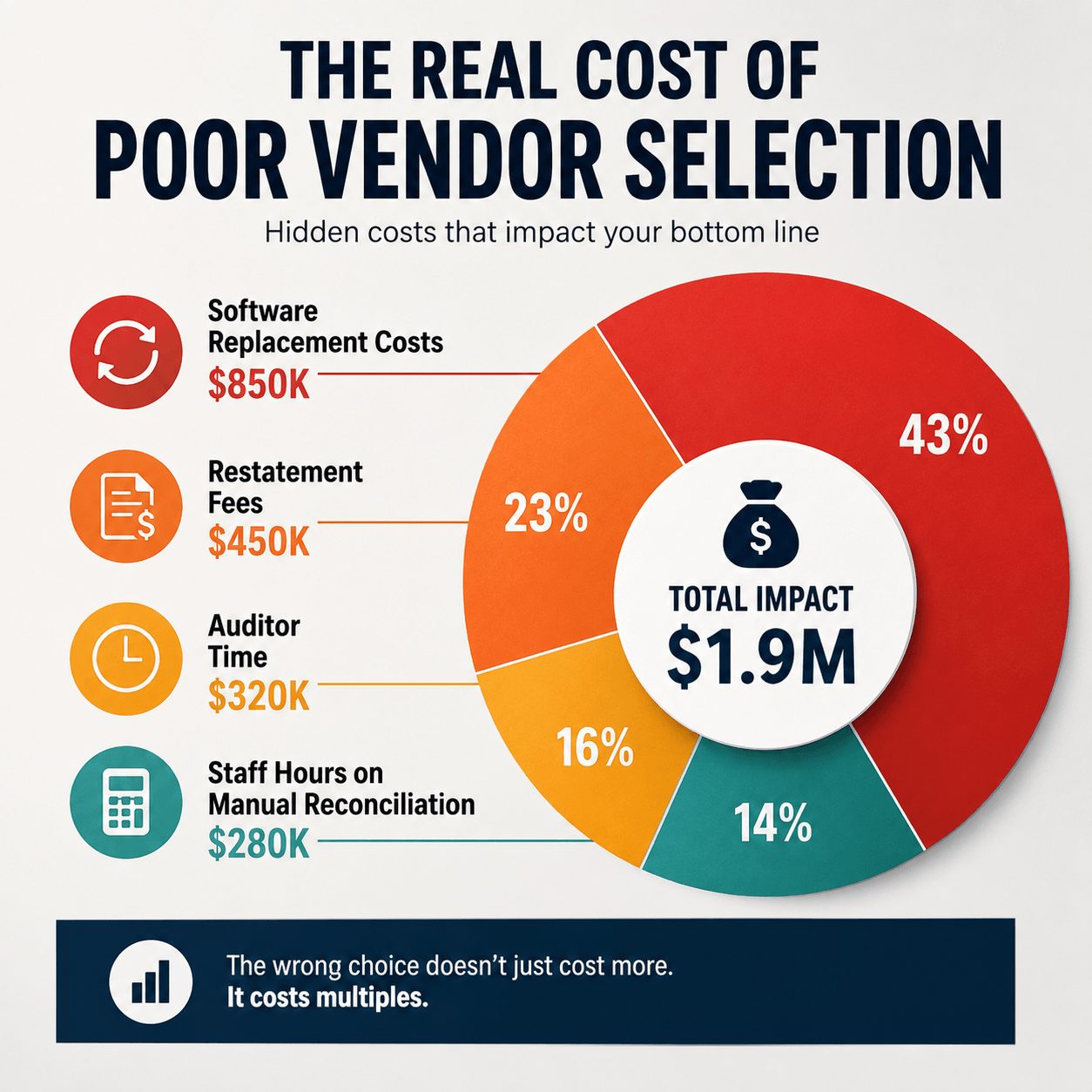

Most finance teams underestimate the cost of a bad vendor decision because the damage is delayed. You sign a contract in Q4. The errors surface during your year-end close. And by then, switching is a nine-month project, not a weekend exercise.

A structured vendor selection process makes teams 30% more likely to hit successful implementation outcomes compared to ad-hoc approaches. But most vetting processes for valuation management software providers still rely on demo-day impressions and sales decks.

That’s not vetting. That’s hoping.

The financial cost is real. Gartner puts the average annual cost of poor data quality — the kind that flows from misconfigured valuation software — at roughly $15 million per organization. Add restatement risk, auditor fees, and the opportunity cost of your team manually reconciling outputs, and the number climbs fast. And that’s before you factor in regulator attention.

One in three accountants makes multiple errors per week specifically because the tools they use can’t handle the volume or complexity they’re working with, per a 2024 Gartner survey of 497 finance professionals. That’s a tooling problem, not a people problem. The right valuation management software eliminates the manual reconciliation loop — but only if it’s actually accurate.

Quick self-assessment: How many of these apply to your current valuation setup?

- Your team manually adjusts outputs before sending to auditors

- You can’t trace an actuarial assumption back to a specific model version

- Your software vendor has never mentioned IVS 2025 or IAS 19 in your review calls

- Your EOSB calculations are still done in a spreadsheet

If two or more of these are true, your vetting process, or your current vendor, has a gap worth addressing before your next reporting cycle.

What Should Valuation Management Software Providers Actually Prove to You?

Here’s where most procurement teams get this backwards. They ask what the software can do. The right question is: what can the vendor prove it does, with your data, under your regulatory framework?

There’s a meaningful difference. A feature list is marketing. A live model run against your employee data, under IAS 19 parameters, using your actuarial assumptions — that’s evidence. Insist on the latter.

Valuation management software providers worth shortlisting should be able to demonstrate four things without hesitation:

- Methodology transparency: You can see exactly how the software applies actuarial methods — projected unit credit, individual accruals, whatever the engagement requires — and trace each output to an input assumption.

- Assumption governance: Discount rates, salary escalation, and attrition assumptions are auditable and version-controlled. Not hidden behind a black box.

- Standards alignment: The platform explicitly maps to IAS 19, IVS 2025, and where relevant, IFRS 9. Not a generic “IFRS-compliant” badge — specific standards, specific outputs.

- Regulatory configuration by jurisdiction: Saudi Arabia’s IFRS adoption timeline differs from the UAE’s. A platform that treats GCC as a single regulatory block is one that hasn’t actually worked in the region.

If a vendor can’t walk you through all four before the contract conversation, that’s your answer.

Ask for a Live Model Run — Not a Demo Reel

Vendors are good at demos. They’re practiced, polished, and designed to show the software at its best — with clean data, favorable assumptions, and no edge cases. That tells you very little about how the platform handles your reality.

Ask for a proof-of-concept run using a sanitized sample of your actual employee data. Watch what happens when you change discount rate assumptions mid-run. Ask how the system handles employees with incomplete tenure records. Ask what happens when an assumption falls outside the platform’s expected range.

The answers to those questions tell you more about accuracy in real-time valuation software than any feature list ever will.

Verify Actuarial Assumption Engines Independently

Most asset valuation software platforms have built-in assumptions engines that suggest actuarial inputs based on demographic profiles. This sounds helpful. It can also mask serious errors if you don’t check the logic.

Have your own actuarial team — or an independent advisor — run parallel calculations using the same inputs the software produces. If the outputs diverge by more than a rounding difference, find out why before you trust the platform with a live reporting cycle. This step takes one week. Skipping it can cost you a quarter.

For teams looking at how to evaluate valuation management software providers in depth, the assumption engine is always the right place to start stress-testing.

Download: IFRS TECH’s Valuation Software Vetting Scorecard

A structured 20-point evaluation framework your team can use before any vendor demo. Covers accuracy testing, compliance depth, EOSB configuration, and GCC-specific regulatory criteria.

Red Flags You’re Looking at the Wrong Asset Valuation Software Vendor

You might think red flags in vendor selection are obvious. They’re not. The most dangerous ones look like reasonable answers.

Vague Compliance Claims Without Audit Trails

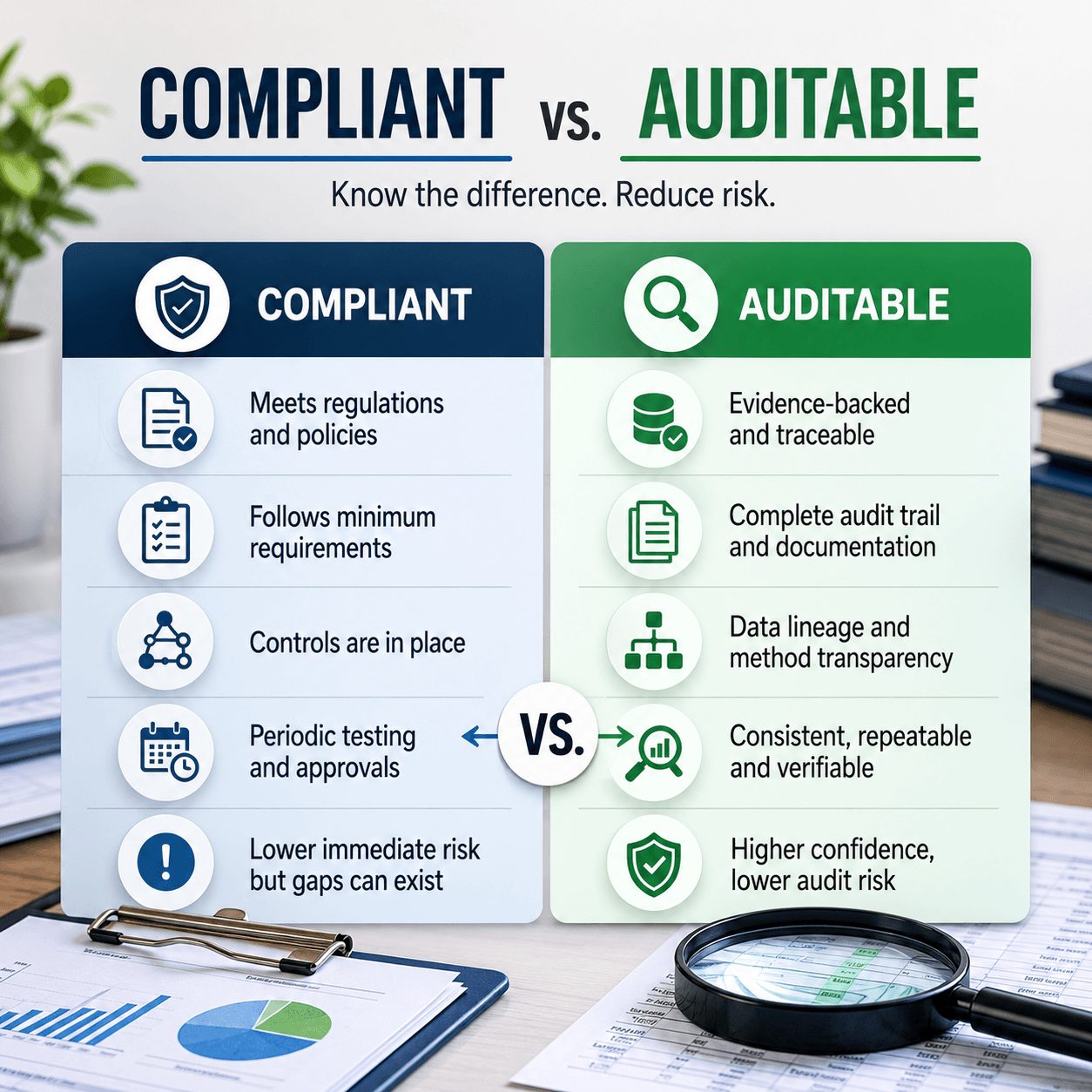

“Fully IFRS-compliant” is one of the most overused phrases in financial software marketing. Ask what that means specifically. Which standards? Which version? Can they show you how the software maps a defined benefit obligation to IAS 19.67 through IAS 19.98?

If the answer involves a lot of reassurance and no documentation, that’s a red flag. IVS 2025, effective January this year, requires that valuation documentation contain sufficient detail to allow another valuer, applying professional judgment, to replicate the valuation. Your software needs to support that. Most don’t, and most vendors won’t mention it.

The gap between “compliant” and “auditable” is where most asset valuation software failures actually live. Don’t let a vendor skip past it.

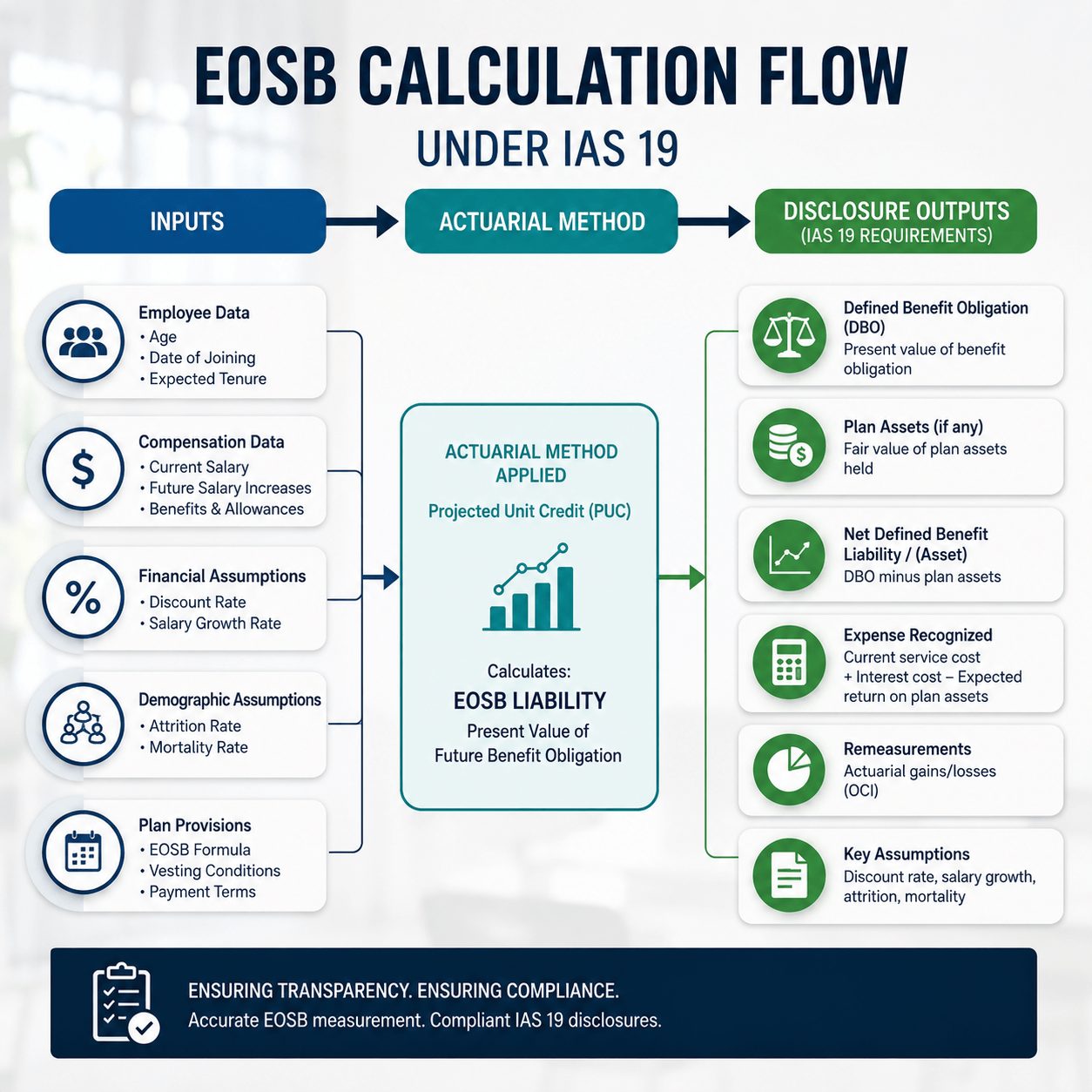

No EOSB-Specific Configuration for the Middle East

End of service benefits valuation in the Middle East operates under a different set of rules than most global platforms are built around. UAE companies have been required to prepare financial statements under IAS 19 since July 2016. Saudi Arabia mandated IFRS compliance for listed companies from January 2017. The labor law calculations underpinning EOSB — different gratuity formulas, different vesting schedules, different treatment for expatriate versus national employees — are not generic.

A platform that offers “Middle East support” as a regional toggle rather than a jurisdiction-specific configuration has probably not done the work. Ask for a specific demo of EOSB calculation under UAE labor law for an employee with eight years of service and a mid-year salary change. Watch how the software handles it. If the answer requires manual adjustment, that’s a problem.

Teams handling IFRS 9 solutions for financial institutions in parallel know this well — GCC-specific configuration is not a nice-to-have. It’s the baseline.

Lock-In Architecture Dressed Up as Integration

Some valuation management software providers build ecosystems that look like open platforms but function as traps. Data exports require proprietary formats. API access is limited or comes with per-call costs. Migrating your historical valuation data requires a professional services engagement with the same vendor.

This isn’t hypothetical. It’s a known commercial strategy. Check the contract for data portability clauses before you sign. Ask how long it would take — and what it would cost — to extract three years of historical valuations if you decided to switch. If the vendor gets uncomfortable with that question, you have your answer.

Avoid non-compliant IFRS 9 compliance software situations by vetting the exit terms as carefully as the entry features.

IFRS TECH’s advisory team has supported over 80 clients across GCC, Europe, and APAC in building valuation and compliance infrastructure — from initial software evaluation through live reporting cycles. See how enterprise IFRS 9 ECL software selection works in practice.

The Vetting Checklist for Valuation Management Software Providers

This is the practical part. Run every valuation management software provider you’re evaluating against these criteria — in writing, before any contract discussion.

Technical and Accuracy Criteria

- Live model run: Can the vendor run a proof-of-concept using your sanitized data before contract signing?

- Assumption auditability: Is every actuarial assumption version-controlled and traceable to a specific report date?

- Real-time recalculation: Can the platform recalculate valuations when an assumption changes, without requiring a full data reload?

- Data quality handling: What happens when employee records are incomplete or contain tenure gaps? Does the system flag, reject, or silently fill?

- Independent validation support: Will the vendor provide calculation methodology documentation detailed enough for a third-party actuary to review?

Compliance and Regulatory Criteria (GCC / Saudi Arabia / UAE)

- IAS 19 mapping: Does the platform explicitly map outputs to IAS 19 disclosure requirements — not just produce a number?

- IVS 2025 alignment: Does valuation documentation meet the replicability standard introduced in the January 2025 revision?

- EOSB jurisdiction configuration: Are UAE labor law formulas and Saudi Arabia-specific vesting rules separately configured — not toggled from a generic template?

- IFRS 9 interoperability: If you’re also managing ECL or impairment modeling, does the platform exchange data cleanly with your IFRS 9 ECL software for banks?

- Regulatory update process: How quickly does the vendor push configuration updates when GCC regulators change requirements? Who owns that process internally?

Vendor Stability and Support Criteria

- Actuarial expertise on staff: Does the vendor employ credentialed actuaries, or is actuarial logic outsourced to a model they licensed?

- Reference clients in your sector: Can they provide two or three references from GCC-based finance teams — not generic enterprise clients?

- SLA for calculation accuracy: Is calculation accuracy covered under a service-level agreement, or just uptime?

- Data portability: What does data export look like? Can you extract three years of historical valuations in a standard format without vendor assistance?

Teams navigating IFRS 9 compliance process architecture alongside EOSB and asset valuation will find this checklist needs to extend to interoperability — how well do your valuation tools talk to each other?

One Criterion Most Teams Skip Entirely

Here’s something I’ve observed across enough evaluations to say with confidence: almost no one asks valuation management software providers about their model update process.

Models aren’t static. Actuarial assumptions shift with economic conditions. Discount rate benchmarks move. Mortality tables update. Regulatory interpretations evolve. A platform that was accurate in 2023 can produce materially wrong numbers in 2025 if the assumption engine hasn’t been updated.

Ask the vendor: who updates the built-in actuarial assumptions, on what schedule, and how are those updates tested before they reach your live environment? If the answer is vague, or if it turns out updates require a new contract engagement, you’re buying a point-in-time tool — not a valuation management platform.

That distinction matters more in the GCC than almost anywhere else, because nearly 63% of Middle East organisations are still not fully aligned with IAS standards — which means the regulatory pressure to get valuations right is only increasing, not leveling off. Your software provider needs to keep pace with that.

End of Service Benefits Valuation in the Middle East: A Harder Test Case

EOSB is where most generalist valuation platforms fail the GCC market specifically. And it’s worth spending a moment on why, because the complexity is often underestimated at the procurement stage.

End of service benefits valuation in the Middle East isn’t just a calculation — it’s a calculation that has to account for multiple variables simultaneously: local labor law formulas that differ by country and sometimes by emirate, actuarial assumptions that need to reflect GCC-specific salary escalation and attrition patterns, IAS 19 disclosure requirements, and in some cases PDPL and CITC data regulations in Saudi Arabia. No single toggle handles all of that.

Over 60% of GCC firms identify compliance as their top concern when adopting financial technology, per EY’s GCC Banking Sector Outlook and related regional analysis. EOSB is one of the reasons why. The calculations are complex enough that even experienced teams misconfigure them — and generic platforms make it easy to produce a number that looks right but isn’t.

The right test is this: ask your shortlisted providers to calculate EOSB for a hypothetical employee with eight years of tenure, a salary that increased 15% in year six, and termination by the employer rather than resignation. Watch whether the platform correctly applies the labor law distinction — because most Middle East jurisdictions treat employer-initiated termination differently from voluntary resignation in the benefit formula. If the software doesn’t handle that distinction natively, your team will be making manual adjustments on every edge case. At scale, that’s not sustainable.

For teams also managing IFRS 9 impairment modeling tools or hedge accounting compliance software alongside EOSB, the interoperability question becomes equally important — your valuation data doesn’t live in isolation from the rest of your compliance stack.

And if I’m being honest about where the field stands: I haven’t seen long-term data on how many GCC organisations have actually remediated their EOSB configurations after discovering they were wrong. The WTW survey data is informative but dated. What I can say is that every client we’ve worked with who self-reported “IFRS-compliant” EOSB and then ran a rigorous check found at least one assumption that needed correcting. Not all of them were material. Some were.

What You Now Know

- Vetting valuation management software providers requires proof of accuracy — live model runs, assumption traceability, and jurisdiction-specific EOSB configuration — not just feature demonstrations.

- The most common red flags are vague compliance claims without audit trails, generic Middle East support that doesn’t account for UAE or Saudi Arabia labor law, and lock-in architecture that makes switching expensive.

- End of service benefits valuation in the Middle East is a harder technical test than most generic platforms are built to pass — use it as your primary screening question.

The Right Valuation Software Provider Proves It — Before You Sign

Valuation management software providers that can’t demonstrate accuracy under your regulatory framework, with your data, before contract signing are asking you to trust them on faith. That’s not how you want to enter a relationship that directly affects your financial disclosures.

The GCC compliance environment is getting more demanding, not less. IFRS 18 is coming. IVS 2025 is already in effect. The organisations that will handle the next reporting cycle cleanly are the ones that made the right vendor decision this year — based on evidence, not sales confidence.

Run the checklist. Ask the hard questions about EOSB configuration. Verify the assumption engine independently. And if a vendor gets uncomfortable when you ask about data portability terms, treat that reaction as data.

For teams working through IFRS 9 alongside valuation challenges, the IFRS 9 compliance software tools assessment process follows a similar logic — prove it, don’t promise it. And if you’re still relying on spreadsheets for any part of this, the case for change is clear in the hidden audit risks in IFRS 9 spreadsheets analysis.

See how IFRS TECH’s valuation advisory team handles EOSB and asset valuation accuracy for GCC clients →

Over 80 clients across banking, insurance, and corporate finance trust IFRS TECH to get valuations right the first time. Our team combines credentialed actuaries, CPAs, and CFAs — we don’t rely on generic platforms to do specialized work.

Book a 30-minute assessment with IFRS TECH →

Learn more about IFRS 9 advisory services from Prima Consulting →

Frequently Asked Questions

What are the most important criteria when vetting valuation management software providers?

Focus on accuracy first. Ask for a live model run with your data, verify assumption traceability, and confirm the platform has jurisdiction-specific configuration for your regulatory framework — particularly IAS 19 and local labor law for EOSB. Compliance claims without audit documentation are not sufficient for GCC reporting requirements.

How do I test for accuracy in real-time valuation software before buying?

Request a proof-of-concept run using sanitized sample data. Change a key assumption mid-run — such as the discount rate — and observe how the system recalculates. Then have an independent actuary verify the output against a manual calculation. Divergence beyond rounding is a signal to investigate before committing.

What are the red flags in selecting valuation software vendors for the GCC market?

Watch for vague IFRS compliance claims without standard-specific documentation, generic Middle East configurations that don’t account for UAE and Saudi Arabia labor law differences, and contract terms that make data export expensive or complex. These are the three most consistent failure points in GCC valuation software procurement.

Why does end of service benefits valuation in the Middle East require specialized software?

EOSB calculations under IAS 19 must account for local labor law distinctions — including different benefit formulas for employer-initiated versus voluntary terminations — alongside actuarial assumptions specific to GCC salary patterns and attrition rates. Generic platforms rarely configure these correctly without significant manual intervention.

How often should valuation management software actuarial assumptions be updated?

At minimum, annually — but the right answer is whenever underlying economic conditions shift materially. Discount rate benchmarks, mortality tables, and salary escalation assumptions can all change in a single reporting cycle. Ask your provider how updates are managed, tested, and pushed to your live environment before you rely on the platform for disclosures.