Finance teams and actuaries across the GCC and APAC regions: here’s how to pick the right actuarial valuation approach before your next audit cycle catches you short.

✓ Written by IFRS TECH’s advisory team · ✓ Serving GCC, Europe & APAC · ✓ Actuaries + CPAs + CFAs

TL;DR

Choosing the right actuarial valuation software for IAS compliance is one of the most consequential decisions a finance team makes. This article walks you through the three primary approaches — spreadsheets, external consultants, and dedicated actuarial valuation software — and what separates good decisions from costly ones. You’ll see how gratuity valuation software fits into GCC-specific reporting, what the build-vs-buy decision actually looks like in practice, and which features matter most for IAS standards compliance. Read this before you commit to any valuation solution.

What Happens When Your Actuarial Valuation Software Gets IAS Wrong?

Your external auditor flags an IAS 19 disclosure error three days before sign-off. The liability calculation doesn’t reconcile. You’ve got a spreadsheet model built two years ago by someone who no longer works there, and no one is entirely sure what assumptions it uses.

That’s not a hypothetical. According to a 2024 Gartner survey cited by Unit4’s financial reporting analysis, more than one in three accountants are making errors weekly — and that’s before you factor in the specific complexity of IAS 19 defined benefit valuations.

Here’s what makes IAS compliance unforgiving: a 1% change in the discount rate assumption can shift your defined benefit obligation by 15–20%. That’s not a rounding error. That’s a restatement-level swing that auditors notice and boards ask about.

This article covers three things:

- The main approaches to actuarial valuation software for IAS standards

- How to evaluate build vs. buy decisions for your specific situation

- What to look for when selecting IAS compliance software for gratuity, EOSB, and pension obligations

IFRS TECH works with finance teams across the GCC, Europe, and APAC to get this right. The approaches below reflect what actually works — not what looks good in a vendor presentation.

Three Core Approaches to Actuarial Valuation Software for IAS Compliance

Most organizations sit somewhere across three approaches. None is universally wrong — but one carries risks that finance teams chronically underestimate.

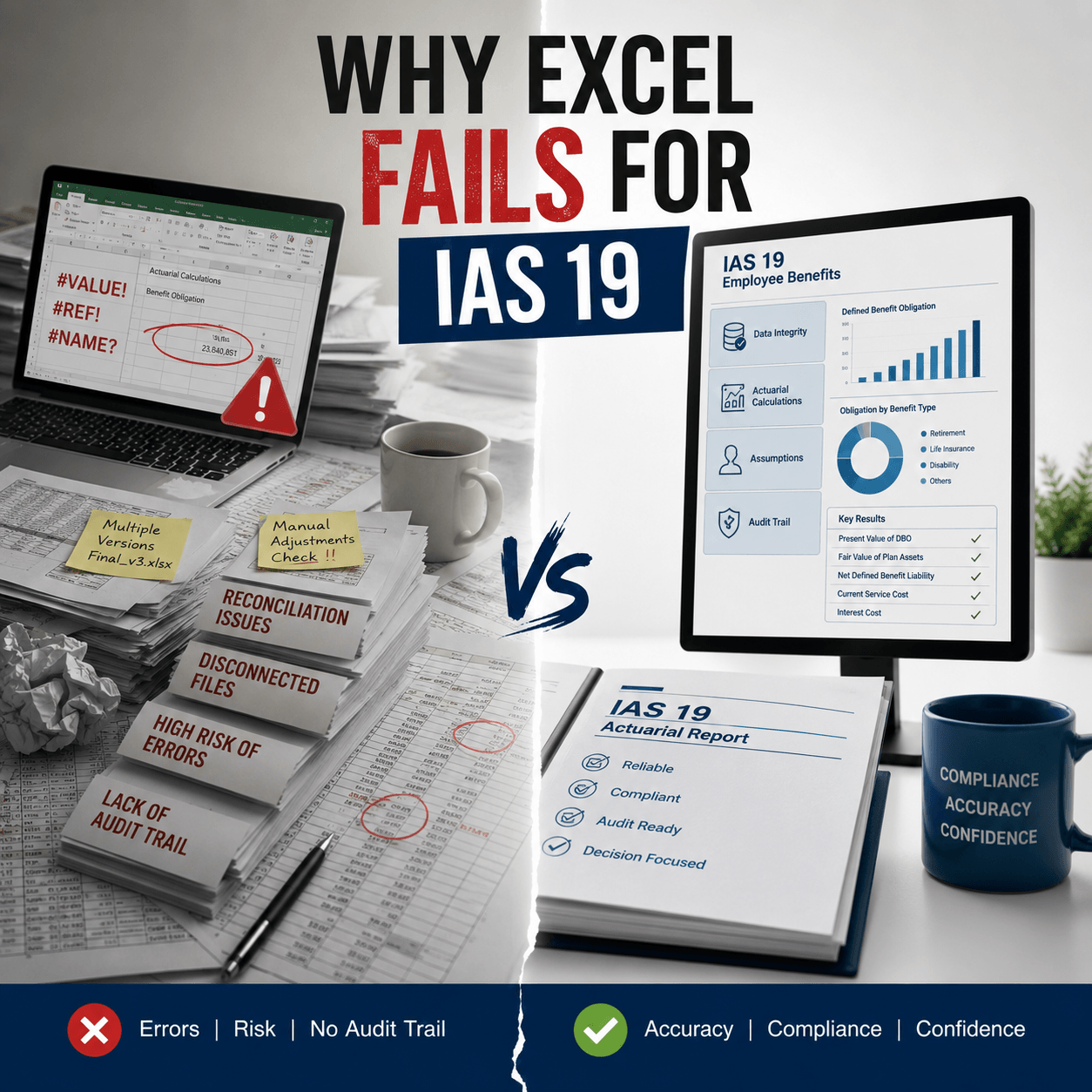

Approach 1 — Spreadsheet-Based Valuation (and Why It’s a Risk)

Spreadsheets are the default starting point. They’re familiar, cheap to set up, and easy to explain to a non-technical CFO. The problem shows up around year two or three.

Actuarial assumptions need to change. Workforce data gets messier. Discount rates shift. Someone updates a formula in column R without touching the audit trail. By the time your IAS 19 reporting package goes to auditors, you’re defending a model that’s had four contributors and zero version control.

Let’s be direct: spreadsheets fail at scale. They work reasonably well for a single-entity business with a stable workforce below 200 employees. For anything more complex — multi-entity groups, frequent workforce changes, quarterly IAS reporting — they’re a liability dressed as a solution. Full stop.

What the IAS 19 guidance doesn’t tell you plainly is that “using an actuary” doesn’t mean your process is compliant. The method needs to be documented, auditable, and reproducible. A spreadsheet built by a brilliant actuary five years ago is none of those things if no one can verify it today.

Approach 2 — External Actuarial Consultants

Bringing in an external actuary solves the methodology problem. You get professional sign-off, an actuarial report, and someone else to hold accountable during audit season. That’s real value — especially for organizations doing an annual valuation for the first time.

On the flip side, the model strains when you need valuations more than once a year. Quarterly IAS compliance software needs are common for listed companies and multinationals. Every additional run means another engagement, another invoice, another waiting period — typically weeks, not days.

There’s also a data control issue that nobody talks about openly enough. Sending your employee census data to an external firm creates privacy exposure. In Saudi Arabia, the Personal Data Protection Law (PDPL) has changed what acceptable data sharing looks like. The GCC broadly is tightening this. If your actuarial compliance software approach involves emailing workforce data to a third party, that’s worth a legal review.

External consultants remain the right answer in specific scenarios: a one-off valuation, independent expert sign-off for a transaction, or when your internal team has no actuarial capability at all. Outside those situations, there are better options.

Approach 3 — Dedicated Actuarial Valuation Software

Purpose-built actuarial valuation software handles what consultants and spreadsheets can’t — speed, repeatability, and data sovereignty in the same package.

The global actuarial modeling software market reached USD 2.05 billion in 2024 and is growing at a CAGR of 9.2% toward USD 4.48 billion by 2033, according to Dataintelo’s actuarial market research. That growth reflects how quickly organizations are moving away from manual approaches. The driver isn’t technology enthusiasm — it’s the audit-trail requirements that come with modern IFRS reporting standards.

A well-designed IAS compliance software platform does three things at once: it applies the Projected Unit Credit Method correctly, it generates audit-ready actuarial reports, and it gives your finance team direct control over output without waiting on a third party. Automation cuts valuation preparation time by up to 40%, based on analysis comparing automated platforms to manual workflows, per Insights Consultancy’s 2026 review (URL unverified — recommend manual check).

This is the approach that scales. For organizations managing gratuity in the UAE, end-of-service benefits in Saudi Arabia, or pension obligations across multiple APAC jurisdictions, scale isn’t optional.

IFRS TECH’s benefits valuation software is built for this use case — handling gratuity, EOSB, and defined benefit obligations with built-in IAS 19 methodology and instant report generation.

Build vs. Buy: The Decision Most Finance Teams Get Wrong

Here’s a counterintuitive point: organizations that try to build actuarial valuation capabilities in-house usually don’t fail because they lack technical skill. They fail because they underestimate the ongoing maintenance burden.

Building your own IAS compliance software means maintaining it. That includes keeping pace with IAS standard amendments, updating discount rate curves, ensuring your assumptions engine reflects current mortality and salary escalation data, and rebuilding audit trails every time a regulatory update drops. The IASB issued amendments to IAS 19 effective through 2025, and IFRS 18 — which affects presentation and disclosure — came into force in April 2024. Keeping a homegrown system current with all of that is a full-time job. Probably two.

Buying a purpose-built solution transfers that maintenance responsibility to a vendor whose entire business model depends on staying current. That’s a fundamentally different risk profile.

What is your finance team’s core competency? If the answer is running your business, managing treasury, and reporting accurately — not developing and maintaining actuarial calculation engines — then the build-vs-buy decision answers itself.

I’ll be honest about one limit here: I don’t have long-term total cost of ownership data across all vendor options in GCC markets specifically. Organizations in Saudi Arabia and UAE should get real quotes and compare directly. What I can say confidently is that for most mid-size multinationals, the buy option wins on cost within 18 months when you account for consultant fees avoided.

See how IFRS TECH’s actuarial valuation software team approaches IAS compliance for GCC entities →

Our advisory team can walk you through a live demo of the IAS 19 valuation tool — including gratuity, EOSB, and multi-entity reporting scenarios.

Selecting the Right Actuarial Valuation Software for IAS Standards

Not all actuarial software solutions are the same. These are the criteria that actually matter when you’re evaluating options for IAS standards compliance.

Projected Unit Credit Method — Non-Negotiable

IAS 19 mandates the Projected Unit Credit Method (PUCM) for defined benefit obligations. Any actuarial valuation software for IAS standards that doesn’t build PUCM into its core calculation engine is the wrong tool. Ask for it explicitly before you go further in any vendor evaluation.

PUCM requires projecting each employee’s benefit earned to date, applying salary escalation and discount rate assumptions, then discounting back to present value. The complexity is in the assumptions engine and in handling exceptions — early leavers, plan amendments, curtailments. Good IFRS accounting software handles all of that without manual intervention.

Integration with Your HR and Finance Systems

Employee census data is the raw input for every actuarial valuation. If you’re exporting from your HR system into a CSV, cleaning it manually, and uploading to your valuation tool, you’ve introduced an error risk from the first step. The right employee benefits valuation software connects directly to SAP, Oracle, or your ERP of choice.

IFRS TECH’s approach to share plan valuations and accounting software illustrates how integration with financial reporting workflows should be structured — not as an add-on, but as part of the reporting pipeline itself.

Audit-Ready Outputs and Disclosure Reporting

Your auditors need a signed actuarial report, finance team needs the journal entries, disclosure team needs the IAS 19 note disclosures formatted for the financial statements. The best IAS reporting software produces all three in a single run.

This is where mid-market solutions often fall short. They produce a calculation but not a disclosure-ready output. You end up reformatting results manually — which reintroduces the exact human error risk you were trying to eliminate.

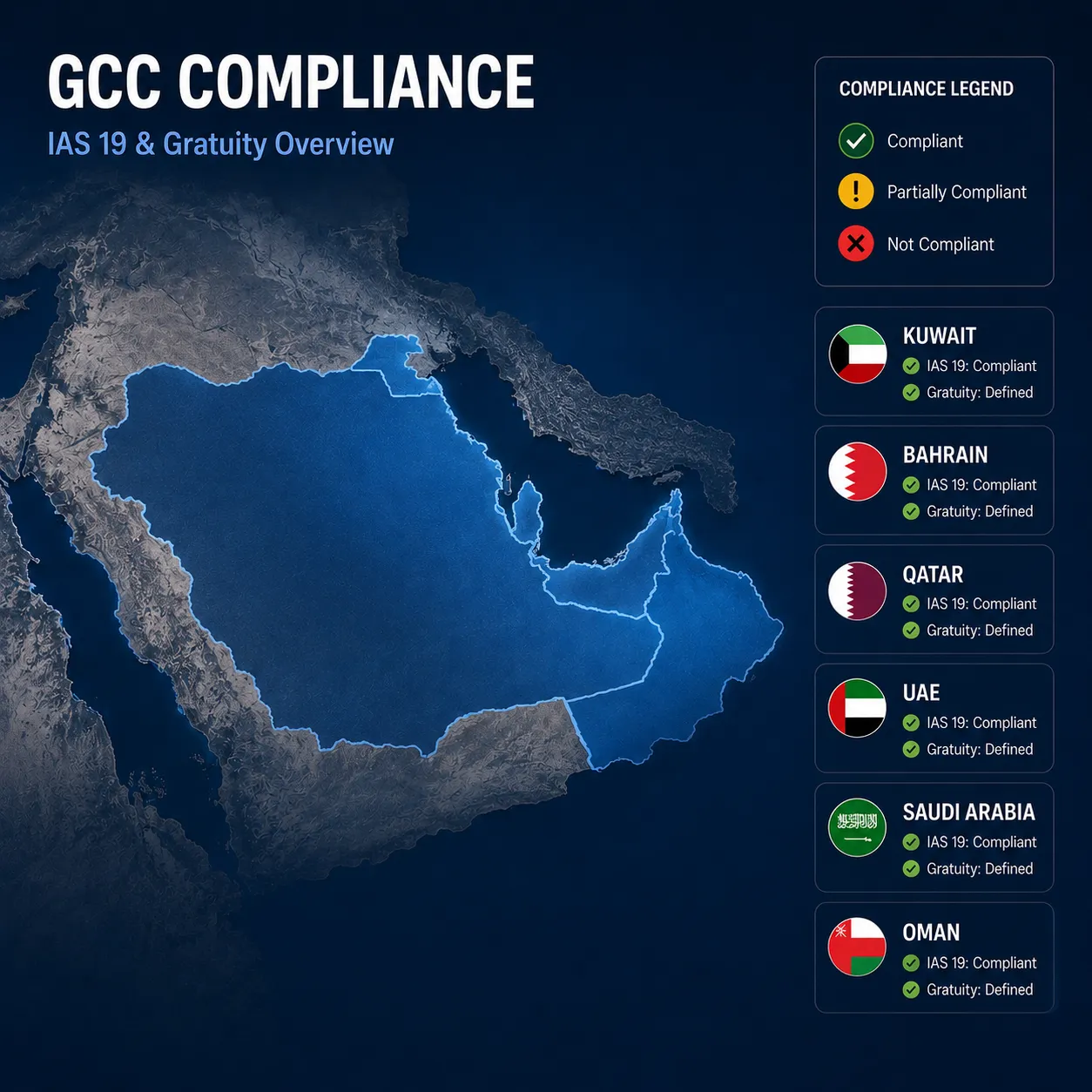

Gratuity and EOSB Valuation in the GCC Context

For organizations operating in Saudi Arabia, UAE, Kuwait, Bahrain, Qatar, and Oman, gratuity valuation software needs to handle end-of-service benefit structures that differ from Western pension models. GCC labor laws mandate specific gratuity calculations tied to years of service and final salary. IAS 19 treats these as defined benefit obligations requiring actuarial measurement.

A generic pension platform built for UK or US markets won’t have GCC-specific labor law assumptions built in. You’ll be customizing it manually — and that manual customization is where compliance gaps appear. What’s interesting is that the gap between generic actuarial tools and GCC-specific gratuity valuation software is wider than most regional finance teams realize until audit season.

What the Numbers Say About Actuarial Software Adoption

The market data tells a clear story. Actuarial modeling software grew from USD 588 million in 2024 to USD 626 million in 2025, with forecasts pointing to USD 993 million by 2032, according to Research and Markets’ market forecast. That’s consistent compounding growth — not a trend spike.

The driver isn’t technology enthusiasm. It’s compliance pressure. IFRS 18, effective from April 2024, changed how entities present and disclose financial statements. IAS 19 amendments continue to tighten disclosure requirements. Every regulatory update raises the bar for what “compliant” means — and manual processes struggle to keep up.

Cloud-based actuarial valuation tools are accelerating the shift. Deployment timelines for cloud platforms run in weeks. On-premise implementations take months, according to IFRS TECH’s review of IAS 19 valuation tools across deployment models. For organizations that need to be operational before the next reporting deadline, that difference is decisive.

Organizations that treat compliance technology as a business transformation — not a box-ticking exercise — consistently report better stakeholder outcomes. A KPMG 2024 Insurance Report finding, cited in prima consulting’s IFRS 17 best practices guide, put that satisfaction gap at 32%. The exact number is sector-specific, but the direction holds across most IFRS compliance programs.

Finance teams that get this right spend less time defending calculations and more time using them. That’s the whole game.

Where Most IAS Compliance Programs Fail

Most actuarial valuation software programs don’t fail because of bad technology. They fail because no one owns the assumptions review cycle.

Actuarial assumptions — discount rates, salary escalation, mortality rates, employee turnover — need to be reviewed and updated at least annually. In many organizations, no one is formally responsible for this. The initial implementation gets done, the valuation runs, reports get filed, and eighteen months pass before anyone checks whether the discount rate still reflects current market conditions.

A 1% shift in discount rates can move your defined benefit liability by 15–20%. In the rising-rate environment of 2023 and 2024, organizations that updated assumptions on time reported lower liabilities and cleaner audit outcomes. Those that didn’t had to explain why their IAS 19 numbers looked stale compared to peers. That’s an uncomfortable conversation.

The technology is the easy part. The discipline is harder. Your IAS compliance software should include a built-in workflow for annual assumption review — not just a calculation engine. If your current platform doesn’t have that, build the review cycle into your financial calendar manually and assign a named owner.

And here’s a hard truth: if your CFO doesn’t know what assumptions your current IAS 19 model uses, that’s an audit risk — regardless of which software you’re running.

“The question isn’t whether your valuation method is technically correct. The question is whether you can defend every assumption in front of an auditor at 9am on short notice.” — IFRS TECH Advisory Team

IFRS TECH’s team of actuaries and CPAs works directly with clients across the GCC and APAC to build this kind of process discipline — not just deploy actuarial compliance software.

See how IFRS TECH’s IAS compliance team handles actuarial assumption governance →

✓ Served 80+ clients across GCC, Europe & APAC · ✓ Actuaries + CPAs on every engagement

What You Now Know

- Three approaches exist — spreadsheets, external consultants, and dedicated actuarial valuation software — each with distinct trade-offs on cost, speed, data privacy, and audit readiness. For most mid-size and growing organizations, purpose-built software wins on almost every axis beyond a single-entity, annual-only valuation.

- The build-vs-buy decision is usually answered by maintenance cost — keeping a homegrown IAS compliance solution current with IASB amendments and local labor law changes requires ongoing resource investment that most finance teams can’t justify when vendor-maintained platforms exist.

- GCC-specific context matters — gratuity and EOSB valuations under IAS 19 require software built with GCC labor law assumptions, not a repackaged Western pension tool. The difference shows up in audit.

You’ve covered the core approaches to actuarial valuation software for IAS compliance — what separates spreadsheet risk from scalable solutions, what the build-vs-buy math really looks like, and why the GCC context demands tools built for it. The next step is matching what you’ve read here to your actual reporting cycle. If you’re running annual valuations today and growing toward quarterly, get the right actuarial compliance software in place before the next deadline — not during it.

See how IFRS TECH’s actuarial valuation software team delivers IAS-compliant reporting for GCC entities →

✓ Instant audit-ready reports · ✓ Built-in PUCM engine · ✓ Gratuity & EOSB ready · ✓ No third-party data sharing

Frequently Asked Questions

What is actuarial valuation software for IAS compliance?

It’s a platform that automates the calculation of defined benefit obligations — including gratuity, pensions, and EOSB — using the Projected Unit Credit Method required under IAS 19. Good IAS compliance software produces audit-ready reports, applies correct discount rates, and generates full disclosure notes without manual data reformatting.

How does gratuity valuation software support IAS reporting in the GCC?

Gratuity valuation software built for GCC markets applies region-specific labor law assumptions — service-based benefit accruals, local discount rates, and jurisdiction-specific turnover patterns — within the IAS 19 Projected Unit Credit framework, producing compliant reports for Saudi Arabia, UAE, and other GCC jurisdictions.

What is the difference between actuarial valuation software and IFRS accounting software?

Actuarial valuation software performs the underlying benefit obligation calculations. IFRS accounting software handles broader financial reporting and disclosure. The best solutions connect both — so actuarial output feeds directly into your financial statements without manual transfer.

When should an organization move from consultants to dedicated actuarial valuation tools?

When valuations exceed once per year, when multi-entity reporting is involved, or when external data sharing creates privacy concerns under local data protection law. At that point, dedicated actuarial software solutions typically deliver faster turnaround and lower cost per run than consultant-led approaches.

What features matter most in actuarial valuation software for IAS standards compliance?

The non-negotiables: a built-in Projected Unit Credit Method engine, direct HR system integration, audit-ready report generation, and disclosure-formatted IAS 19 output. For GCC organizations, gratuity valuation software with local labor law assumptions is an additional requirement most generic platforms don’t meet out of the box.