TL;DR

Manual IFRS compliant accounting platforms break down fast when your organization grows across multiple entities, currencies, and jurisdictions. Spreadsheets can’t apply IAS and IFRS rules consistently, and version conflicts, intercompany mismatches, and missing audit trails quietly build up until auditors find them. Regulatory pressure is growing too, with IFRS 18 set to change financial statement presentation requirements by 2027, and manual tools can’t update themselves. You’ll learn why scaling IAS compliant systems manually creates real compliance risk, and what that risk actually costs your finance team over time. Read the full article to see where your current setup is most exposed.

Scalability Issues in Manual IFRS Compliant Accounting Platforms

Your team closes the books every month. Formulas break, files conflict, and someone always asks which version is the latest. That’s not a workflow problem. That’s what IFRS compliant accounting platforms are supposed to solve, and manual tools simply can’t.

Companies operating across multiple entities, currencies, and jurisdictions face scaling problems that spreadsheets and basic software were never designed to handle. The pressure to report accurately under IFRS 9, IFRS 15, IFRS 16, IFRS 17, and IAS standards is real, and it compounds fast when your tools don’t grow with your business.

This article breaks down why manual IFRS compliant accounting platforms fail at scale, what those failures cost, and what the regulatory environment now demands from any system claiming compliance.

Why IFRS Compliant Accounting Platforms Break Under Scale

Most finance teams start with manageable data volumes. One entity, one currency, one set of books. That’s where manual tools appear to work. They’re familiar, fast to set up, and easy to justify when the complexity is low.

But IFRS compliance isn’t low complexity. It requires consistent application of technical accounting standards across every transaction, disclosure, and reporting period. That requirement doesn’t stay manageable when your organization grows.

IFRS or a local implementation of IFRS is now required by public companies in 167 countries. That’s the regulatory baseline. Once you add multiple subsidiaries, intercompany transactions, and cross-border currency translation, manual IFRS compliant accounting platforms hit their limit quickly.

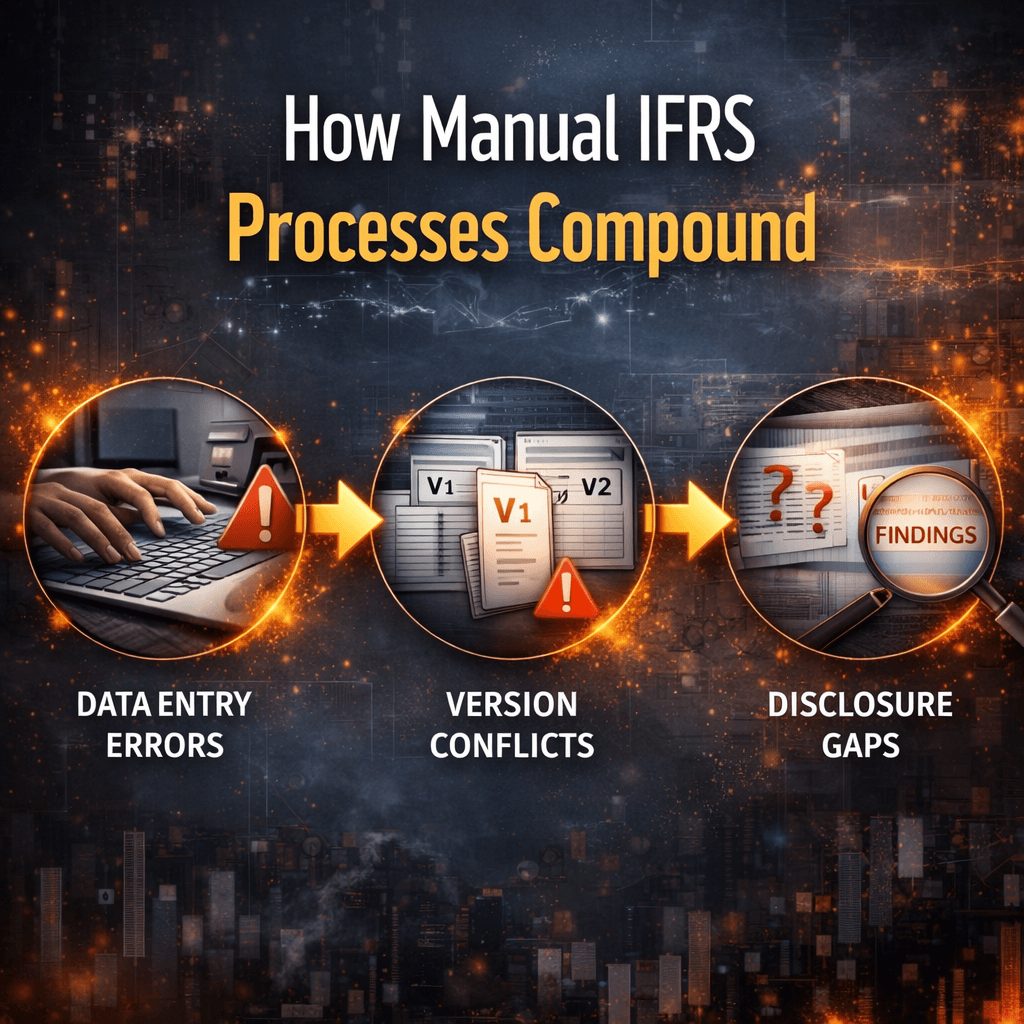

The failure isn’t sudden. It’s gradual. Teams add more tabs, more workarounds, and more manual steps. Each addition raises the error risk. None of it is visible to auditors until something goes wrong.

What Manual Tools Actually Look Like at Scale

When companies rely on spreadsheets or basic software to manage IFRS compliance, a few patterns repeat across industries and geographies.

Version Control and Data Integrity Break Down First

Manual IFRS compliant accounting platforms depend on human discipline to maintain file version control. Finance teams work across time zones, copy files, and edit them locally. That process creates conflicts that go undetected until reporting is due.

More than 80% of multinationals use spreadsheets for managing financial reporting. The same research found that most organizations had rules for controlling these systems, but compliance with those rules was essentially non-existent. That gap between policy and practice is where IFRS reporting errors originate.

Intercompany Eliminations Become Unmanageable

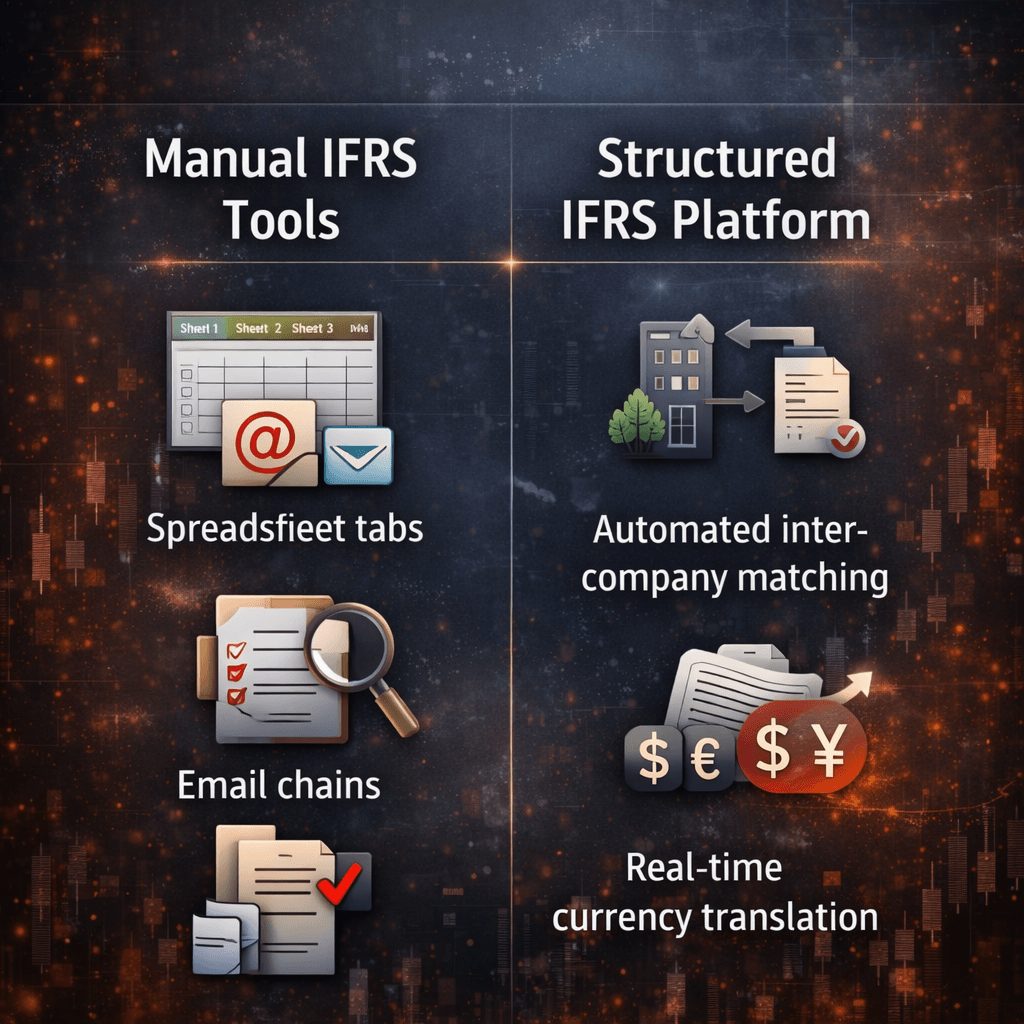

Multi-entity IFRS reporting requires eliminating intercompany balances before consolidated statements can be prepared. Every transaction between related entities has to be identified, matched, and removed from the consolidated view.

Manual ias compliant tools rely on finance teams to track these transactions through linked spreadsheet tabs or exported data. When entities run on different systems with different charts of accounts, matching becomes guesswork. Errors compound each period, and by year-end, the intercompany elimination process can take weeks.

ifrs financial reporting platforms shows how this problem gets worse as organizations grow, particularly when new subsidiaries are added without a standardized data structure in place.

Currency Translation Errors Compound Over Time

IAS 21 governs how organizations translate financial statements from functional currencies into presentation currencies. The rules differ depending on whether an item is a monetary or non-monetary asset, and exchange rates vary between transaction date, reporting date, and average period rates.

Manual IAS accounting software can’t apply those rules consistently across hundreds of transactions without human review of every line. Teams running multi-currency books in spreadsheets often apply a single exchange rate across all items, which violates IAS 21 and creates misstatements that compound across periods.

How Regulatory Pressure Is Making Manual Tools Riskier

The IFRS regulatory system is characterized by continuous change. Standards get amended, new guidance is issued, and disclosure requirements expand. Teams relying on manual ifrs erp environments have to track those changes themselves and update every formula, template, and schedule manually.

IFRS 18, effective for annual periods beginning on or after January 1, 2027, fundamentally changes how organizations present financial statements. It introduces required subtotals in the profit or loss statement and new disclosure requirements for management-defined performance measures. Manual tools don’t update themselves. Every change requires a manual rebuild, which reintroduces the same risks of error and inconsistency.

That’s on top of IFRS 9, IFRS 15, IFRS 16, and IFRS 17, each of which carries its own data granularity requirements. IFRS 16 alone requires organizations to track right-of-use assets and lease liabilities for every qualifying lease arrangement. According to a Deloitte South Africa webinar poll, 74% of attendees still rely on Excel to manage their IFRS 16 compliance, despite the standard being in effect since 2019.

That’s a compliance exposure that auditors are increasingly flagging. Poor lease data creates inaccurate reporting, missed renewal deadlines, and audit findings that are entirely preventable.

The Specific Scaling Problems in Multi-Entity IFRS Environments

Scaling IFRS compliance across multiple legal entities isn’t just about having more data. It’s about maintaining consistency across structures that are inherently different.

Different Charts of Accounts Across Entities

Subsidiaries acquired over time often operate on different general ledger structures. Mapping those structures to a consolidated chart of accounts for IFRS reporting is a manual exercise that breaks down when any subsidiary adds new accounts or changes account codes mid-period.

Inconsistent Application of IFRS Standards Across Jurisdictions

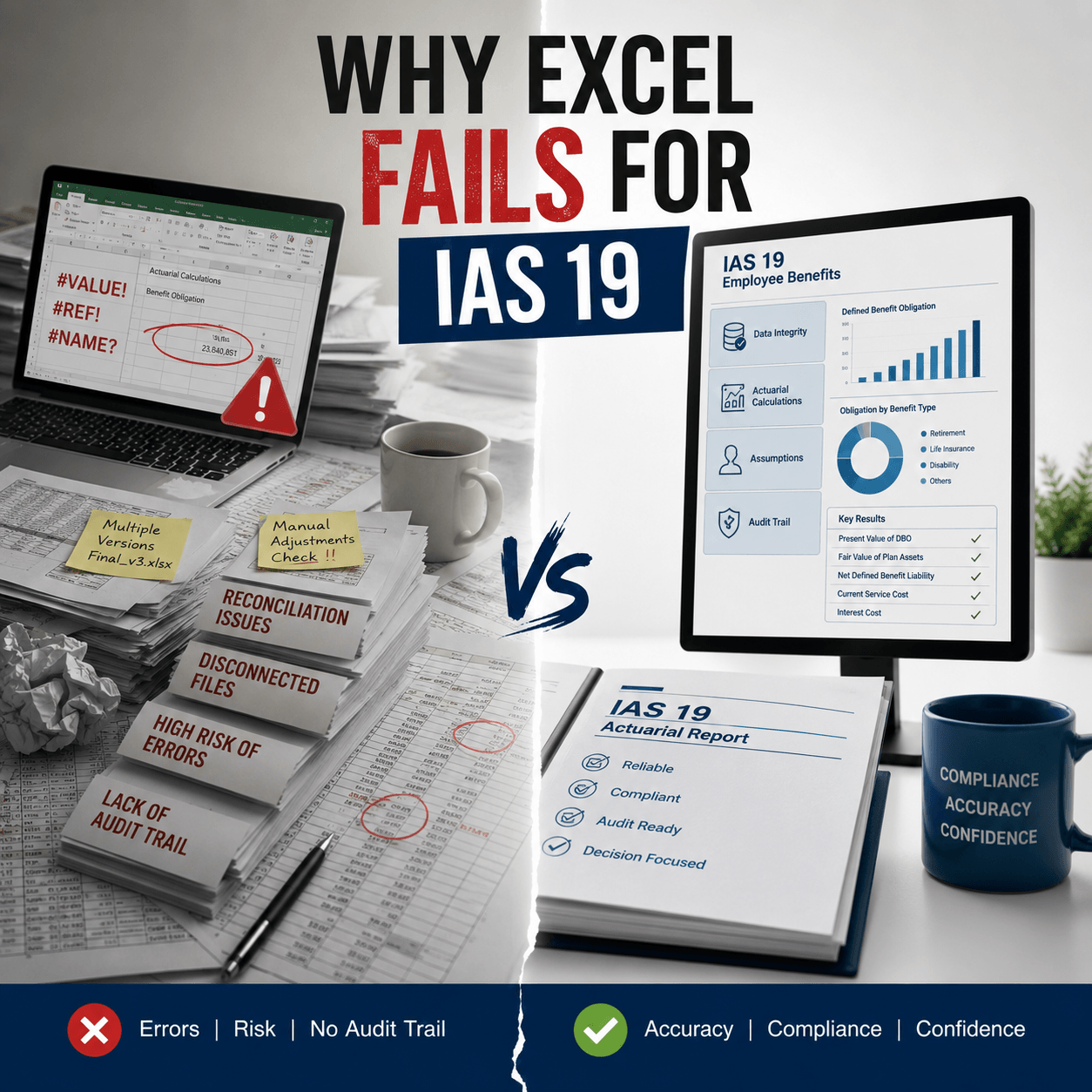

When subsidiaries operate under local GAAP and produce IFRS adjustments at period-end, the adjustments depend on local finance teams applying the same accounting judgments as group finance. Without integrated ias accounting software, those judgments differ. Revenue recognition timing under IFRS 15, impairment assessments under IAS 36, and employee benefit calculations under IAS 19 all require consistent application that manual tools can’t enforce.

ifrs accounting software integration covers how misalignment between entity-level and group-level systems creates the audit findings that regulators are now scrutinizing more closely.

Month-End Close Times Grow With Each Entity

Manual reconciliation slows month-end close proportionally to the number of entities in scope. A 2024 QuickBooks business survey found that companies spend an average of 25 hours per week on manual reconciliation and data correction. In multi-entity environments, that number compounds quickly as entities, currencies, and pricing models increase.

Finance teams spend those hours chasing balances instead of analyzing them. That means leadership doesn’t have timely insights when they need them most.

Audit Risks From Poor IFRS Accounting Scalability

Regulators and external auditors evaluate IFRS compliance by looking at evidence. They want to see consistent application of accounting policies, documented accounting judgments, and complete audit trails that trace every adjustment back to its source.

Manual ias compliant systems rarely produce that evidence cleanly. Audit trails in spreadsheets are either absent or unreliable. Accounting judgment documentation is stored in emails or separate files. Adjustments are made without version-stamped records.

The result is longer audit cycles, more queries, and a higher risk of qualified opinions. Deloitte’s survey data shows that 50% of organizations [nofollow] cite lack of defined ownership as a major challenge in multi-entity financial processes. That ownership gap is exactly what auditors look for when assessing internal controls.

A qualified audit opinion isn’t just a regulatory problem. It affects credit ratings, investor confidence, and the ability to operate in regulated markets.

Data Problems in Manual IFRS ERP Systems

The term “IFRS ERP” is often used loosely to describe any accounting system that produces IFRS-formatted outputs. But producing the right format isn’t the same as applying the right rules. Many basic ERP configurations generate reports that look IFRS-compliant but contain measurement errors, missing disclosures, or classification mistakes.

Those problems are invisible until an auditor or regulator looks closely. By then, restating prior periods is expensive, disruptive, and reputationally damaging.

The root cause is usually data quality at the input stage. Manual data entry into accounting systems without validation rules allows misclassified transactions, incorrect effective dates, and missing required fields to pass through unchecked.

Transition Challenges to Automated Compliant Software

Moving from a manual environment to an integrated IFRS compliant accounting platform isn’t plug-and-play. Organizations face real transition challenges that slow adoption and sometimes lead teams to underestimate what the change involves.

Data migration is the first friction point. Historical data in spreadsheets is often structured inconsistently across periods. Cleaning that data before migration takes time and requires finance team involvement alongside any implementation partner.

Change management is the second. Finance teams who built the manual systems often resist replacing them. That resistance is understandable. The manual tools feel controllable because the team built them. The answer isn’t to force the change. It’s to show clearly what the current system is costing in time, audit risk, and regulatory exposure.

The third challenge is integration. Most organizations run ERP systems alongside their accounting platforms. An IFRS compliant platform that doesn’t connect to the ERP through reliable data feeds creates a new manual step instead of removing old ones.

People Also Ask: IFRS Compliant Accounting Platforms

What is an IFRS compliant accounting platform? It’s a system that applies IFRS standards automatically across financial processes, including measurement, disclosure generation, intercompany elimination, and audit trail creation. Unlike general accounting tools, it enforces standard-specific rules consistently across entities and periods.

Why do manual IFRS tools fail at scale? Manual tools depend on human consistency to apply IFRS rules correctly. As entity count, transaction volume, and standard complexity grow, human consistency breaks down. Version conflicts, intercompany mismatches, and inconsistent accounting judgments accumulate faster than manual review can catch them.

What are the audit risks of manual IFRS compliance? Auditors look for complete audit trails, documented accounting judgments, and consistent policy application. Manual systems rarely produce clean evidence of any of those three things. The result is extended audit cycles, more queries, and potential qualified opinions.

How does IFRS 16 create problems for manual systems? IFRS 16 requires tracking right-of-use assets and lease liabilities for every qualifying lease. Manual systems require finance teams to maintain that data in spreadsheets with custom formulas. Formula errors, missed lease modifications, and incorrect rate inputs are common and difficult to detect before audit.

What’s the difference between IFRS-formatted and IFRS-compliant reporting? IFRS-formatted means the output follows IFRS presentation layouts. IFRS-compliant means the underlying measurements, disclosures, and classifications all meet IFRS requirements. Many basic systems produce the first without the second.

When should an organization move away from manual IFRS tools? The clearest signal is when month-end close times, audit queries, or intercompany reconciliation errors grow faster than your entity count. If your compliance process takes more time each period without delivering more insight, it’s scaling in the wrong direction.

The Real Cost of Staying Manual

Manual IFRS compliance tools feel like a cost-saving choice because the software is familiar and the upfront cost is zero. That’s the wrong calculation. The real cost is the hours finance teams spend on reconciliation, the audit risk they carry, and the regulatory exposure they accumulate every period they don’t fix the underlying data problems.

The regulatory environment is only getting stricter. IFRS 18 alone requires structural changes to financial statement presentation that manual templates cannot absorb without a complete rebuild. Organizations that wait for a compliance failure to force the change will find the transition far more disruptive than if they had started earlier.

The question isn’t whether your current IFRS compliant accounting platform will eventually fail. The question is how much it costs you between now and when that happens.

If you want to understand where your current compliance infrastructure stands and what closing the gaps would actually require, Prima Consulting provides the advisory, regulatory, and implementation expertise to help finance teams assess that honestly.