TL;DR

Your IAS 19 actuarial valuation software can only be as reliable as the data feeding into it. When HR, payroll, and ERP systems don’t connect cleanly to your valuation model, you get inconsistent employee records, mismatched assumptions, and liability figures that won’t hold up under audit scrutiny. This article walks you through the most common integration challenges in IAS 19 actuarial valuation software, how they create compliance exposure, and what steps you can take to fix them. Read on to see whether your current setup is putting your next audit at risk.

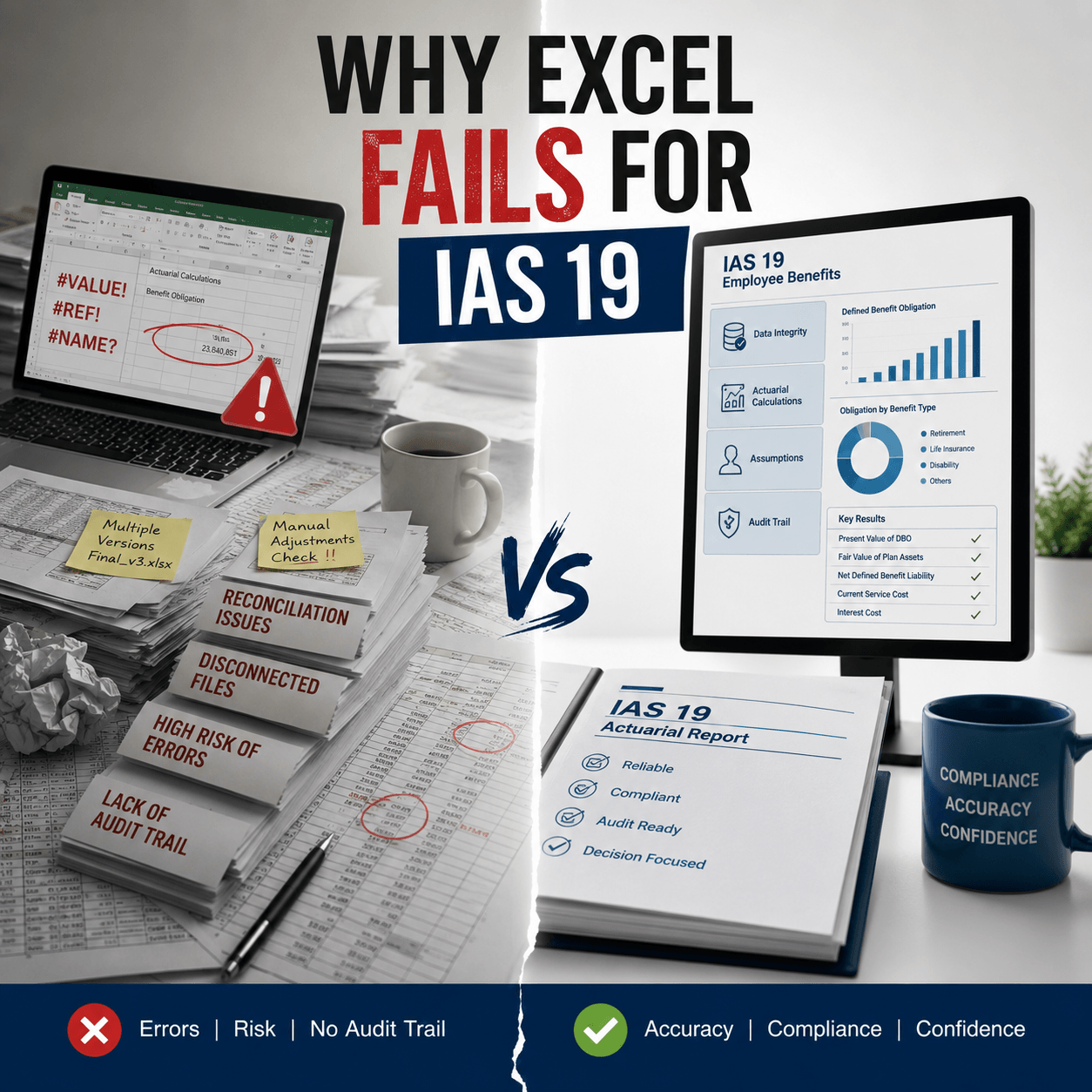

Your IAS 19 actuarial valuation software may run the math perfectly.

But if it can’t talk cleanly to your HR, payroll, or ERP system, the output is only as good as the data going in.

That gap between systems is where most valuation problems start.

You end up with inconsistent employee records, mismatched assumptions, and liability figures that don’t hold up under audit.

This article breaks down why integration challenges in IAS 19 actuarial valuation software are so common and what they cost you when left unresolved.

IAS 19 Actuarial Valuation Software: Key Integration Issues

Most organizations using IAS 19 valuation tools run into the same set of problems.

The valuation engine works well in isolation, but it doesn’t receive clean, timely data from the systems that feed it.

The result is a reporting cycle that relies on manual checks, workarounds, and last-minute fixes.

Data Migration and Legacy System Compatibility

Legacy HR and payroll platforms weren’t built to share data with actuarial models.

They often store employee records in formats that don’t map directly to the fields your valuation software needs.

When you migrate data from these older systems, field definitions can differ, date formats may conflict, and employee group categories rarely line up.

Every mismatch is a potential error in your defined benefit obligation.

Integration with HR, Payroll, and ERP Systems

A clean IAS 19 calculation needs consistent input from multiple systems at once.

You’re pulling hire dates, salary histories, contract types, and benefit entitlements from HR.

You’re drawing payroll figures from a separate platform.

And you’re posting the final liability to a general ledger that may sit inside an ERP.

When those three systems run on separate data cycles, your valuation reflects three different snapshots in time.

That misalignment creates discrepancies that are hard to trace and harder to explain to auditors.

Data Accuracy and Validation Challenges

Even when systems are technically connected, the data flowing through them may not be accurate.

Re-hires can appear as new employees, early retirements may go unrecorded, and expatriate staff are sometimes grouped with local employees even when the benefit formula differs.

A 2023 PwC survey found that 55% of actuaries spend more than half their working time managing data issues rather than modeling.

That’s not a modeling problem. That’s an integration problem.

How Integration Impacts IAS 19 Compliance

Poor integration doesn’t just slow you down.

It creates compliance exposure at every stage of the reporting cycle.

Audit Readiness and Reporting Delays

Auditors reviewing IAS 19 disclosures want a clear, version-controlled trail from the raw employee data to the final liability figure.

When data moves manually from HR to the valuation model, that trail breaks.

You can’t reproduce a prior-period run easily, and you can’t show the auditor which version of the salary-growth assumption was used at what point in the cycle.

That’s exactly the kind of weakness that leads to extra scrutiny, extended audit timelines, and in serious cases, qualified opinions.

Risk of Manual Workarounds and Errors

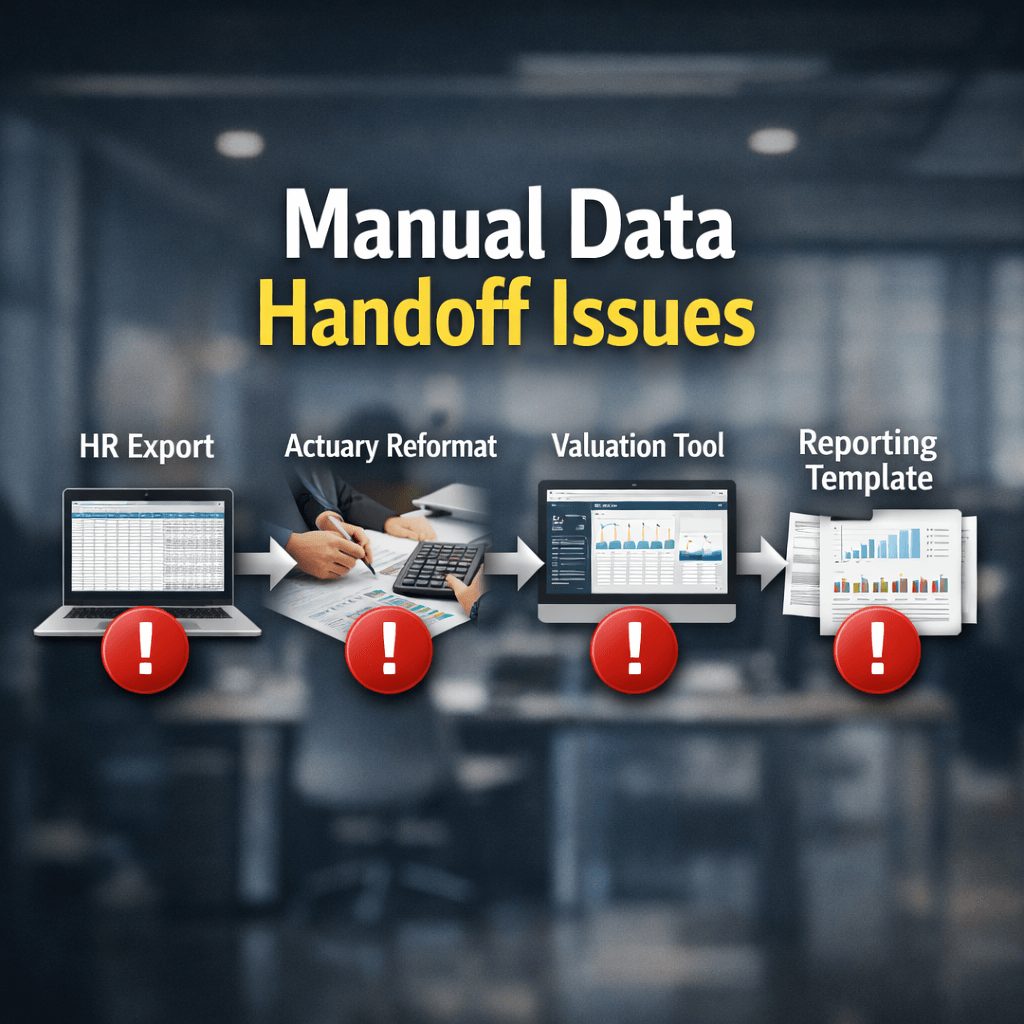

When integration fails, teams fill the gaps with spreadsheets.

An HR analyst exports a file, an actuary reformats it, someone pastes figures into the valuation model, and then a finance manager copies results into the reporting template.

Each handoff is a point of failure.

A single copy-paste error in a salary figure or a missed employee record can distort your pension actuarial valuation software output materially.

You may not catch it until the auditor does.

Errors creep in at every step

Governance, Controls, and Data Security

Integration gaps also create governance problems.

When the HR team owns the employee data and the actuarial team owns the model, and no formal handoff process connects them, you get assumption drift.

Different versions of the discount rate or salary growth curve end up being used in different departments, often without anyone noticing until the reconciliation stage.

On top of that, manual data transfers increase the risk of unauthorized access to sensitive employee information.

A well-governed integration process includes defined access controls, automated reconciliation checkpoints, and a clear record of who approved each assumption set.

Common System and Process Gaps

The problems with IAS 19 actuarial valuation integration aren’t random.

They follow predictable patterns across organizations, regardless of size or industry.

Inconsistent Employee Data Structures

Different departments often classify employees differently.

HR may label a worker as a fixed-term contractor while payroll treats the same person as a full-time employee.

In a GCC context, expatriates and nationals frequently fall under different End-of-Service Benefit (EOSB) entitlement formulas, but the HR system doesn’t always flag that distinction in a way the valuation model can read.

The actuarial software then applies the wrong benefit formula to the wrong population, and the liability estimate moves in the wrong direction.

Lack of Real-Time Data Synchronization

Most IAS 19 pension valuation platforms run on periodic data loads, not live feeds.

That means the valuation reflects the workforce as it existed on the export date, not the current date.

If a large group of employees leaves or joins between the data snapshot and the valuation run, the liability figure can be off by a meaningful amount.

For organizations with high staff turnover or rapid hiring cycles, this timing gap is a consistent source of valuation inconsistency.

Handling Plan Amendments and Complex Benefits

When a company changes its EOSB formula or modifies a defined benefit plan, the actuarial model needs to reflect that change from the correct effective date.

In a manually integrated environment, plan amendments often get applied late or inconsistently across different employee groups.

This is one of the most common sources of IAS19 actuarial valuation errors that attract audit flags, because the change is visible in the financial statements but the underlying data trail doesn’t support it clearly.

How to Overcome Integration Challenges

The good news is that most integration problems are solvable.

They require a structured approach to how data flows, how assumptions are managed, and what controls sit between your systems.

Standardizing Data Across Systems

Start by agreeing on a shared data dictionary across HR, payroll, and finance.

Define which fields are mandatory for IAS 19 purposes: effective hire date, contract type, nationality, benefit eligibility category, promotion date, and current gross salary.

Once every system uses the same field definitions and the same classification rules, the data that reaches your valuation model is already clean enough to use without manual reformatting.

Choosing Compatible and Scalable Software

Not all actuarial valuation software handles integration the same way.

When selecting a platform, check whether it supports direct API connections to your HR and ERP systems, whether it logs every data import with a timestamp and version number, and whether it can separate employee groups automatically based on benefit type.

A system that scales with your workforce without requiring a full re-implementation every few years will save you significant time in the medium term.

You can find a detailed breakdown of what to look for in IAS 19 pension valuation platforms before making a selection.

Using APIs and Automation for Seamless Integration

An API-based connection between your HR system and your valuation model removes the manual export step entirely.

Changes in the HR system, whether a new hire, a promotion, or a contract-type update, flow into the valuation model on a defined schedule with no human intervention required.

Automated reconciliation checks can then flag any record that doesn’t pass validation before it enters the model, giving your team a chance to review and correct it before the valuation runs.

That’s what a closed-loop integration looks like in practice: HR feeds the model, the model feeds the balance sheet, and every step is logged and traceable.

Clean data. Clear audit trail. Faster reporting

What Features Reduce Integration Risk?

If you’re assessing your current setup or evaluating new valuation management software, certain features directly reduce the risk of integration failure.

Built-in IAS 19 Compliance Frameworks

A platform built specifically for IAS 19 actuarial valuation will include pre-configured benefit formulas, discount rate input fields, and demographic assumption tables aligned to the standard.

That removes the risk of applying a generic calculation engine to a compliance-specific problem.

It also means the output is structured in a way that maps directly to your disclosure requirements under IAS 19.

Automated Data Mapping and Validation

Automated mapping means the software knows which HR field corresponds to which valuation input, without a human having to re-do that translation every cycle.

Validation rules built into the import process can catch missing records, out-of-range salary figures, and duplicate employee IDs before they reach the model.

That’s the difference between catching an error at the data entry point and catching it after an auditor flags it in the financial statements.

Custom Reporting and Audit Trails

Audit-ready actuarial valuation software produces a complete calculation log for every run.

That log should show which employee dataset was used, which version of each assumption was applied, and when the run was executed.

When an auditor asks you to reproduce the December 31 valuation with the assumptions in place at that date, a proper audit trail makes that a two-minute task instead of a two-week reconstruction project.

When Should You Upgrade Your Valuation System?

You may not need a complete system overhaul right now.

But there are clear signs that your current setup is creating more risk than it’s worth.

Signs Your Current System Is Failing

You spend more time cleaning and validating data than running the actual valuation.

Your team can’t reproduce a prior-period calculation without going back to email chains and saved spreadsheet versions.

Auditors have raised questions about how assumptions were applied or why figures changed between interim and year-end reporting.

You’re managing multiple employee groups across different jurisdictions and the model treats them all the same.

Any one of these is a signal worth acting on.

Benefits of Modern Actuarial Software

A well-integrated IAS 19 actuarial valuation system shortens your reporting cycle, reduces your dependence on manual data handling, and gives you a defensible audit trail from day one.

According to a 2025 survey of 200 global C-suite executives, 95% of insurance and financial services professionals report significant challenges with legacy core technology platforms.

That finding reflects a broader shift: organizations are recognizing that manual, fragmented systems don’t just slow things down, they introduce real compliance risk.

Modern actuarial software built for IAS 19 removes that risk by design.

One creates delays

The other gives control and accuracy

FAQs: IAS 19 Valuation Software Integration

What is IAS 19 actuarial valuation software?

It’s a platform that calculates the present value of defined benefit obligations, such as pensions and end-of-service benefits, using actuarial assumptions and employee data under the IAS 19 accounting standard.

It replaces or supplements external actuarial consultants by giving your internal team direct control over the calculation model.

Why does HR data integration matter for IAS 19?

The entire liability calculation depends on employee-level data: hire dates, salaries, tenure, and benefit entitlements.

If that data arrives late, incomplete, or misclassified, the output of even a well-built actuarial model will be unreliable.

What are the most common integration challenges in IAS 19 software?

The most common problems are inconsistent employee classification between HR and payroll, manual data transfers that introduce errors, and a lack of version control for assumptions.

These issues often go undetected until an audit raises a question about how a specific figure was derived.

How do integration failures lead to audit qualifications?

Auditors check whether the assumptions and data used in your IAS 19 calculation are consistent, documented, and traceable.

When data flows manually and assumptions aren’t version-controlled, you can’t always answer those questions clearly, and that gap can result in qualified audit findings.

What data fields are critical for an IAS 19 valuation?

At a minimum, you need each employee’s effective start date, contract type, nationality, current gross salary, and benefit eligibility category.

For EOSB-based benefits in GCC jurisdictions, the entitlement formula and years of qualifying service are also required.

How often should HR data be synced with the actuarial model?

For interim valuations, a monthly sync is standard practice.

For year-end reporting, the data snapshot should be taken on a defined cut-off date and locked before the valuation run begins, so the calculation corresponds to a specific, documented workforce position.

What should we look for in valuation management software?

Look for built-in IAS 19 compliance logic, automated data mapping from your HR and payroll systems, assumption version control, and a full audit trail for every calculation run.

Scalability and multi-jurisdiction support are important if your workforce spans more than one country or benefit regime.

IAS 19 Actuarial Valuation Software Needs More Than Good Math

Integration challenges in IAS 19 actuarial valuation software are not a niche technical problem.

They’re a direct compliance risk that affects your audit readiness, your reporting accuracy, and the credibility of your financial statements.

The root cause is almost always the same: data moving manually between HR, payroll, and the valuation model.

No proper controls or version tracking sit between those systems.

Getting that data flow right means standardizing your inputs and choosing software that connects to your existing systems.

It also means building audit trails into the process from the start.

That’s what separates organizations that breeze through IAS 19 audits from those that spend weeks on reconciliation every reporting cycle.

That’s what separates organizations that breeze through IAS 19 audits from those that spend weeks on reconciliation every reporting cycle.

If you want to assess where your current setup stands, the advisory team at Prima Consulting works with organizations worldwide on IAS 19 valuations, integration strategy, and audit-ready actuarial frameworks.

Talk to them about what a cleaner, more defensible valuation process could look like for your team.