Hedge Accounting Compliance Software in Finance: Pick the Right Method

How finance and treasury teams in banks, corporates, and GCC institutions can choose the right integration approach for hedge accounting compliance software, before the next audit cycle begins.

✓ Written by IFRS TECH’s advisory team · ✓ Serving GCC, Europe & APAC · ✓ Actuaries + CPAs + CFAs

TL;DR

Choosing the wrong integration method for hedge accounting compliance software in finance doesn’t just slow your team down. It breaks your audit trail and puts IFRS 9 designations at risk. This article compares five integration approaches, from direct ERP embedding to API-first middleware, and covers what the build vs. buy decision actually costs. You’ll also see what credit risk management software and IFRS 9 technology solutions require before any integration is worth running. If your team is currently in vendor evaluation, read the final checklist before you sign anything.

Here’s something most integration guides skip: hedge accounting compliance doesn’t fail at the calculation engine. It fails at the handoff. The moment data moves from your treasury system to your ERP, or from your valuation tool to your reporting layer, that’s where IFRS 9 breaks down. And the break is almost always invisible until an auditor finds it.

If your team is evaluating hedge accounting compliance software in finance, the question isn’t which platform has the best UI. It’s which integration method keeps your audit trail intact from designation through to journal posting. That decision is more consequential than any feature comparison.

What this article covers:

- The five main integration methods and where each one works or breaks

- The real costs of build vs. buy for hedge compliance automation

- What to demand from a risk and hedge accounting integration platform

IFRS TECH’s advisory team has worked through these decisions with treasury and finance teams across the GCC and Europe. The patterns are consistent — and so are the mistakes.

Why Your Integration Method Decides IFRS 9 Compliance Success

The IASB launched a formal post-implementation review of IFRS 9’s hedge accounting requirements in Q1 2026, per the IASB’s official project page. That review isn’t just bureaucratic housekeeping. It signals that regulators are watching how firms actually run their hedge accounting in practice — not just on paper.

Your integration method is what “in practice” means.

A hedge accounting process can be technically compliant on the standard side and still fail an audit because the system handoff between your treasury management system and your ERP has no approval record. Or because your effectiveness testing runs in a spreadsheet that doesn’t timestamp results. Those aren’t accounting errors. They’re integration failures.

Quick Self-Assessment: Is Your Current Integration Audit-Ready?

- Can you show a timestamped audit trail from hedge designation through to ERP journal posting?

- Does your effectiveness testing output tie directly to the accounting entry — without a manual step?

- If a hedge relationship is de-designated, does the system automatically track the OCI reclassification?

- Can you rerun a prior period’s test and produce the same result with full evidence?

If any answer is “no” or “we’d need to check,” your integration method is the problem. Not the accounting standard.

The global risk management software market hit $15 billion in 2024 and is growing at roughly 12% a year. That growth is not coming from firms buying more software. It’s coming from firms replacing bad integrations with ones that actually hold up under scrutiny.

What Makes Hedge Accounting Compliance Software in Finance So Hard to Connect?

You might think the hard part is the accounting. It’s not. IFRS 9 hedge accounting, once properly understood, follows a logic that most treasury and finance teams can get comfortable with. The genuinely hard part is making three or four separate systems agree on the same data at the same moment, with a verifiable record that proves they did.

The Data Handoff Problem No One Talks About

Hedge accounting rarely lives in one system. Your exposure data sits in one place. Your derivative valuations come from somewhere else. Effectiveness testing might run in a third tool. The journal entries land in your ERP. And your disclosure outputs go into a reporting layer that none of those other systems talk to directly.

That’s four system boundaries. Each one is a control point. Each one is also a place where data can arrive late, arrive wrong, or arrive without any trace of how it got there.

This is why hidden audit risks in IFRS 9 spreadsheets are still showing up in audit findings at firms that thought they had this solved. The spreadsheet wasn’t the problem. The lack of a controlled handoff was.

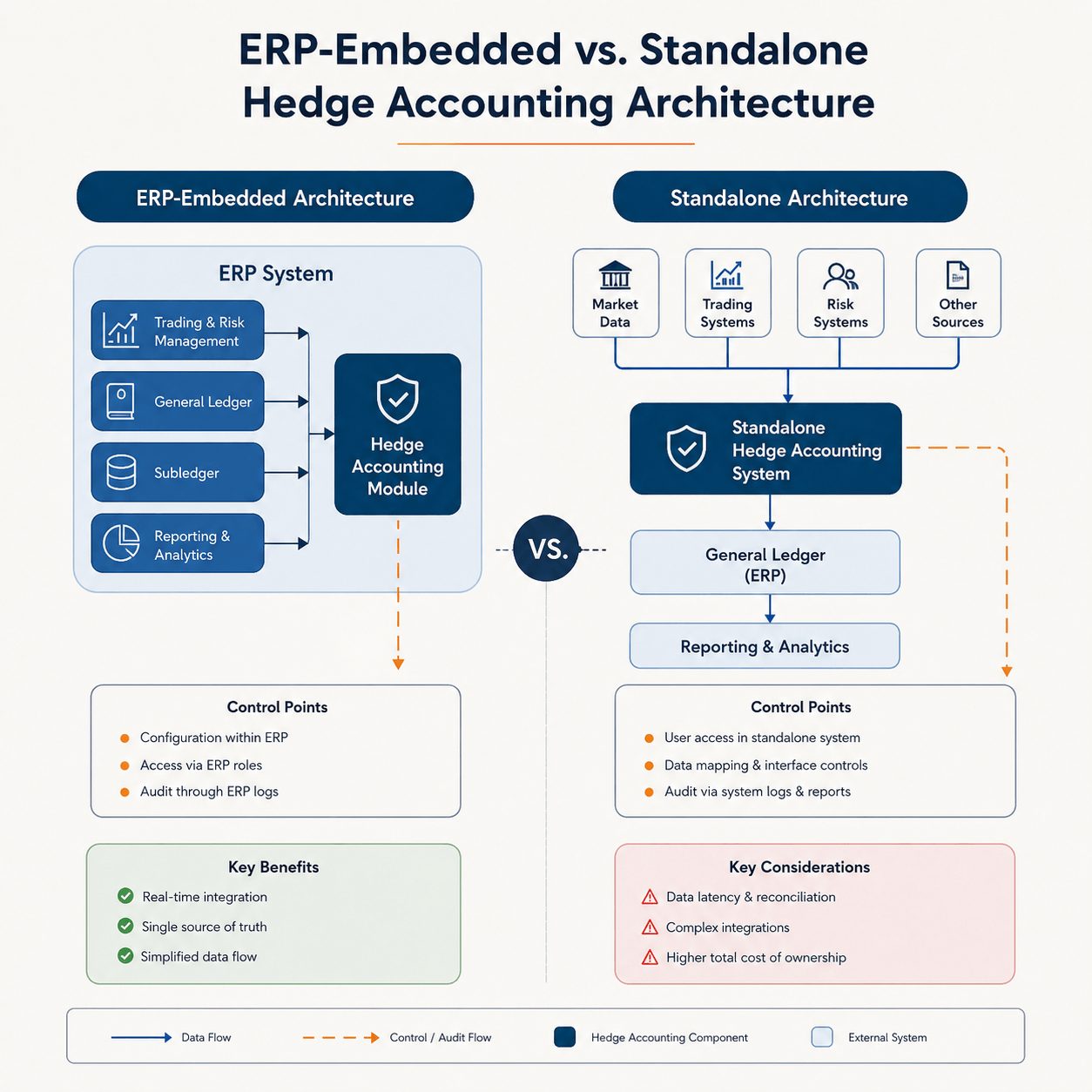

ERP Integration vs. Standalone Deployment: The Core Trade-Off

Firms running SAP S/4HANA or Oracle have a real choice here. Embedding hedge accounting inside your ERP gives you real-time reconciliation and a tighter audit trail. But it also means your hedge accounting process inherits every constraint of your ERP’s upgrade cycle, your IT governance model, and your change management process.

Standalone deployment, on the other hand, gives your treasury team more control. But it creates the handoff problem above. Every connection between your standalone platform and your ERP is a risk point.

Neither is wrong by default. But you have to choose consciously — not by accident.

5 Integration Methods for Hedge Accounting Compliance Software in Finance

Here’s where the comparison gets practical. These are the five methods finance teams actually use, with an honest take on where each one works and where it doesn’t.

If you’re currently weighing these options for a live implementation, see how IFRS TECH’s IFRS 9 advisory services approach integration architecture before any software goes live.

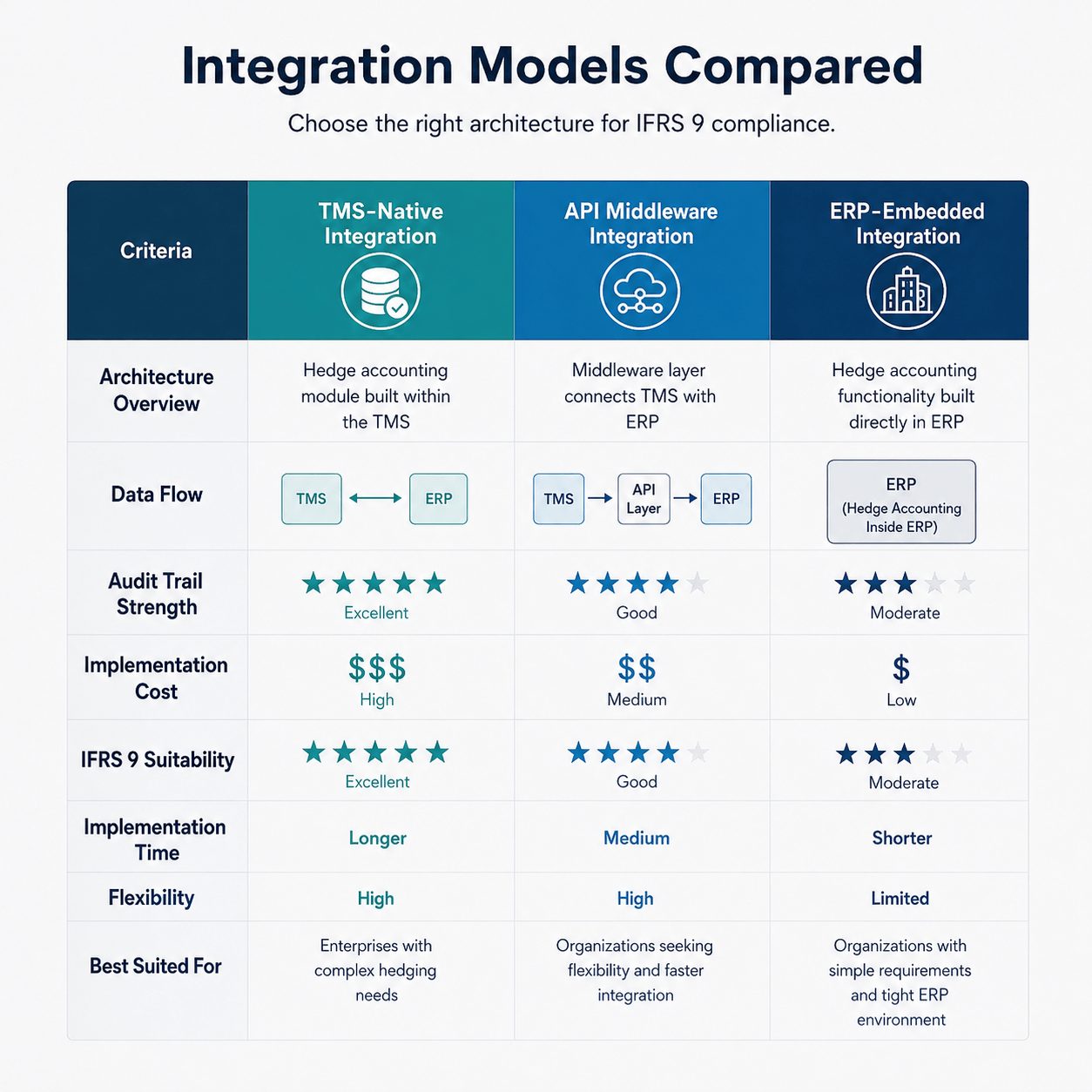

Method 1: Direct ERP Embedding (SAP S/4HANA, Oracle)

This is the cleanest option for large institutions already running a major ERP as their core financial backbone. SAP S/4HANA, for example, embeds treasury and risk functions directly into its finance module. Hedge designation, effectiveness testing, and journal entries all run on one database. There’s no handoff to break.

The upside is real. Real-time reconciliation, embedded analytics, and no data gap between the treasury process and the GL. For firms where treasury and finance are tightly coupled, this reduces both operational risk and audit preparation time significantly.

The downside is also real. ERP-native hedge accounting tools are often less specialized than purpose-built platforms. Kyriba and GTreasury, for instance, offer hedge workflow depth that SAP’s native treasury module doesn’t match out of the box. If your hedging strategy involves complex instruments or non-standard risk components, ERP embedding may require customization that defeats the purpose.

Best for: Large banks or corporates with standardized hedging programs and existing SAP or Oracle infrastructure.

Method 2: API-First Middleware Approach

This is the method most specialized hedge accounting platforms are moving toward. Rather than building a direct point-to-point connection between systems, you use a middleware layer with documented APIs that control exactly what data moves, when, and with what validation.

Platforms like Kyriba and FIS Quantum both highlight API integration with ERP, market data, and banking systems as core capabilities. The audit advantage here is significant. Every data movement through the API layer is logged, with a timestamp and a payload record. That’s the evidence an auditor wants to see.

The risk is implementation complexity. An API-first approach requires more upfront technical work and a team that can maintain the integration as systems upgrade. If your IT team is stretched, this can become a maintenance burden faster than expected.

Best for: Firms with multiple source systems that need a controlled, auditable way to connect hedge accounting to ERP and reporting without rebuilding everything.

See also: IFRS 9 technology solutions in risk for a view of how API architecture fits into broader IFRS 9 technology stacks.

Method 3: Treasury Management System (TMS) Native Integration

This is the approach GTreasury, ION’s Reval, and Wolters Kluwer’s OneSumX take. The hedge accounting workflow lives inside a dedicated TMS that handles the full lifecycle: exposure identification, derivative linkage, effectiveness testing, journal generation, ERP posting, and disclosure support.

When it works well, this is arguably the most complete option for treasury-led hedge accounting compliance. You get hedge accounting software that was built for IFRS 9 (and ASC 815) from the ground up, with ERP connectivity as a designed feature rather than an afterthought.

ION’s Reval, used by Dürr Group among others, positions itself around exactly this: a single integrated TMS that handles risk management, hedge accounting, evaluation, and treasury reporting in one place. That’s a strong model when treasury and finance are aligned on the same platform.

The catch is vendor dependency. Once your hedge accounting process is embedded in a TMS, switching costs are high. And if your TMS vendor’s ERP connector doesn’t fully support your GL version, you end up with a manual gap anyway.

Best for: Treasury-led organizations where the TMS is already the system of record and hedge accounting is one part of a broader treasury program.

Method 4: Point-to-Point File Transfer (and Why It Usually Fails)

Let’s be direct about this one. File-based integration, whether CSV exports, scheduled batch transfers, or FTP drops between systems, is still common and almost always the wrong choice for hedge accounting compliance.

The problem isn’t the file. The problem is the control gap. A file that moves from your TMS to your ERP on a nightly batch has no approval gate, no validation record, and no evidence of what version of data was used in any given period’s effectiveness test. When an auditor asks to rerun last quarter’s test, you can’t do it with integrity.

If your team is currently using IFRS 9 impairment spreadsheet processes, the file transfer risk is almost certainly part of your compliance exposure too. The two problems tend to travel together.

Best for: Nothing in a formal IFRS 9 hedge accounting program. Replace it.

Method 5: Cloud-Native Platform Consolidation

The newest approach and the one gaining ground fastest. Platforms like Enfusion (now part of Clearwater Analytics) and some newer entrants consolidate portfolio management, accounting, and compliance on a single cloud database. No inter-system handoffs because everything is in one place.

For hedge fund accounting specifically, this is compelling. Clearwater processes over $8.8 trillion in global invested assets and has built automated data aggregation and reconciliation into its core architecture. That’s a different class of data integrity than stitching together four separate systems.

For corporate treasury under IFRS 9, the cloud-native model is still maturing. Purpose-built hedge accounting compliance tools from Kyriba or GTreasury still offer deeper IFRS 9 workflow support than most cloud-native consolidation platforms. But that gap is narrowing.

Best for: Hedge funds, asset managers, and organizations that want to eliminate inter-system handoffs entirely and can tolerate a slightly less specialized hedge accounting workflow in exchange for a cleaner architecture.

Take the 5-Question IFRS 9 Integration Readiness Assessment

Before committing to an integration method, know where your current gaps are. IFRS TECH’s readiness assessment covers audit trail integrity, ERP connectivity, effectiveness testing controls, and more.

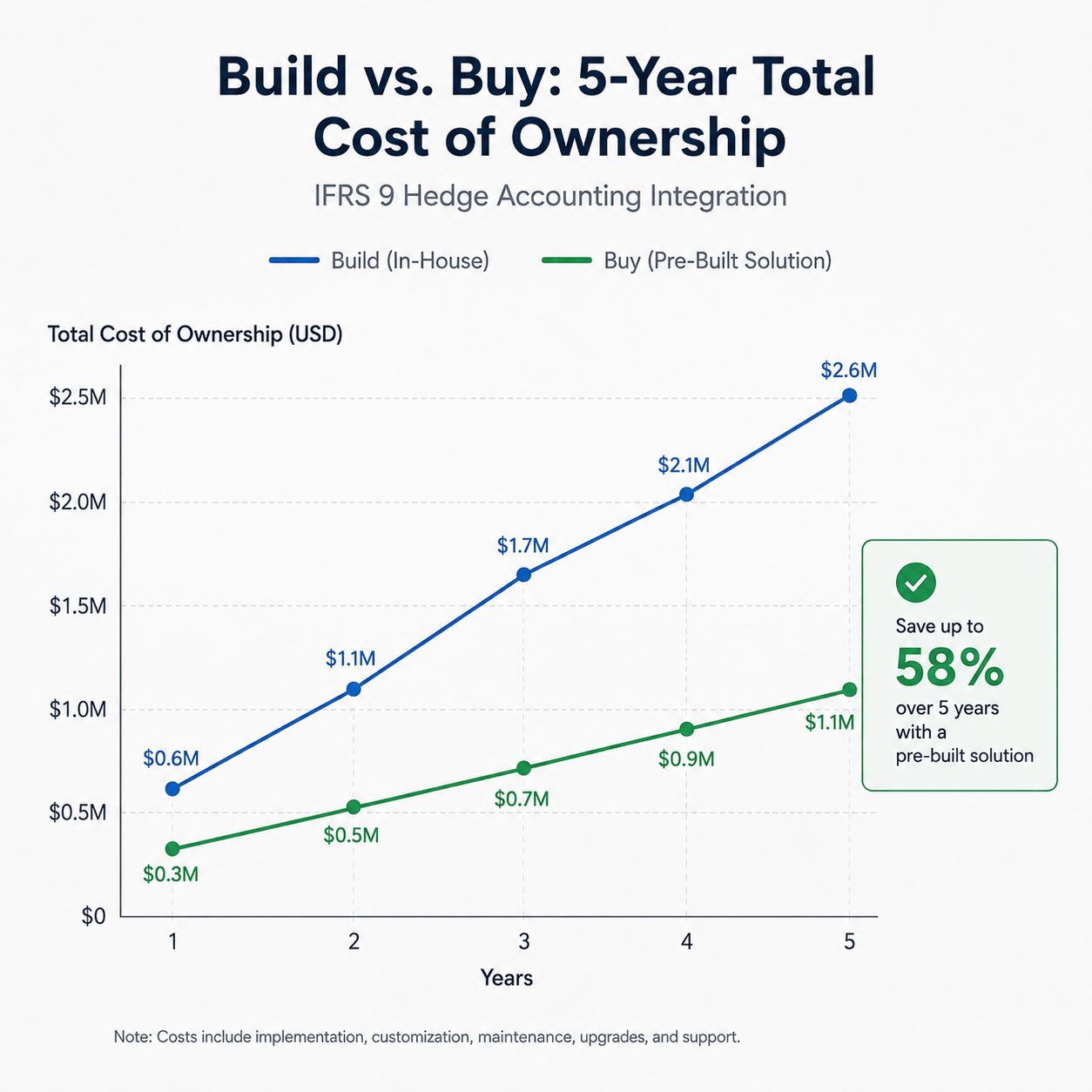

Build vs. Buy for Hedge Compliance Integration: The Real Cost Comparison

This question comes up in almost every engagement. And the honest answer is that most firms that choose to build regret it within two years.

That’s not a knock on internal IT teams. It’s about what hedge accounting compliance actually requires: continuous updates as IFRS 9 evolves, audit trail features that regulators define after implementation, and effectiveness testing logic that has to match whatever methodology your auditor accepts. None of that is stable enough to build once and maintain cheaply.

The IFRS 9 build vs. buy total cost of ownership analysis covers this in detail for banks specifically. The short version: build costs look lower at year one and look much higher by year three, when you add the cost of regulatory updates, audit remediation, and staff time spent maintaining a system that wasn’t designed for ongoing regulatory change.

What the Build Side Gets Wrong

Building your own hedge accounting integration almost always underestimates two things: the cost of the documentation layer and the cost of staying current.

IFRS 9 hedge accounting requires designation memos, effectiveness test records, OCI reclassification tracking, and disclosure support. A built system can handle these if you design them in from the start. But most internal builds focus on the accounting math and treat the documentation layer as a reporting add-on. That’s backwards. The documentation is what survives an audit, not the math.

Staying current is the other trap. When the IASB amended IFRS 9 to address nature-dependent electricity contracts in May 2024, every firm with a built hedge accounting integration had to figure out whether their system handled the change correctly. Vendors pushed an update. Built systems got a project.

Where Bought Platforms Actually Win

Purpose-built IFRS 9 compliance software tools win most clearly in three areas: audit trail depth, effectiveness testing flexibility, and regulatory update speed.

Kyriba’s hedge accounting workflow includes drag-and-drop documentation upload, a separate accounting engine for journal-entry calculation, and an audit trail across settlements and accounting entries. GTreasury’s Hedge Trackers service layer adds managed services support for effectiveness testing and compliance reporting — useful when your treasury team is undersized for the workload.

That’s not something you build internally in year one. It’s something a vendor iterates over years of client feedback. You’re buying that iteration history, not just the software.

I’d note one honest limit here: I don’t have long-term data on post-implementation satisfaction rates for built vs. bought hedge accounting integrations specifically. The anecdotal picture from client work is consistent, but a proper longitudinal study would be more reliable.

How IFRS 9 Technology Solutions Change the Integration Equation

Here’s a point that surprises some teams: the right IFRS 9 technology solutions in risk don’t just automate what your team already does. They change what your team has to do.

Most hedge accounting compliance work today is reactive. You run an effectiveness test. Something fails. You investigate manually. You fix the hedge relationship or de-designate. You update the documentation. You prepare the disclosure. Each step is a separate action, often handled by different people in different systems.

Automated IFRS 9 technology solutions collapse that sequence. Effectiveness testing runs continuously, not quarterly. De-designation events trigger automatic OCI reclassification tracking. Disclosure outputs generate from the same data as the accounting entries, not from a separate manual process.

KPMG’s 2024 research found that AI-driven compliance accuracy improves by 60–70% while cutting compliance costs by 22–30%. That range is wide, and I’d treat it as directional rather than precise. But the direction is clear.

Automated Effectiveness Testing and What It Requires

Automated effectiveness testing is only as good as the data it runs on. This is the integration requirement most software evaluations miss.

If your derivative valuations arrive from a third-party pricing source and land in your TMS on a T+1 batch, your “continuous” effectiveness testing is actually running on yesterday’s data. That’s not continuous. It’s automated-but-lagged. An auditor who understands IFRS 9 will ask when the data was captured, not just when the test ran.

The right approach is real-time or near-real-time market data feeds into your hedge accounting platform, with a documented latency standard that your audit team has signed off on. Platforms like FIS Quantum and Wolters Kluwer’s OneSumX support this. The architecture has to be designed for it, not bolted on.

See how IFRS 9 ECL software for banks handles similar real-time data requirements — the pattern translates directly to hedge accounting.

Credit Risk Management Software and Hedge Integration

One integration that often gets skipped: connecting your credit risk management software to your hedge accounting compliance platform.

Under IFRS 9, credit risk isn’t just an ECL modeling concern. It affects the fair value of your derivative positions through Credit Valuation Adjustment (CVA). If your CVA calculation sits in a separate credit risk system and doesn’t feed directly into your hedge effectiveness tests, you have a silent gap in your IFRS 9 compliance process.

Most firms discover this gap during their first IFRS 9 audit, not before. The fix is straightforward technically, but requires a cross-functional agreement between treasury, credit risk, and finance teams that often doesn’t happen without someone pushing it.

One pattern we see consistently across GCC institutions: firms that integrated their credit risk management software with their hedge accounting platform before the first IFRS 9 audit cycle cut their audit preparation time by roughly 40% compared to those who kept the systems separate. The integration isn’t glamorous. The time saving is.

Risk and Hedge Accounting Integration Platform: What to Demand Before You Sign

Vendor evaluations for a risk and hedge accounting integration platform tend to go wrong in the same ways. Teams spend too much time on feature checklists and not enough time stress-testing the control architecture. Here’s what to demand before signing anything.

ERP Connectivity

Ask for a live demonstration of the ERP integration — specifically how journal entries are generated, approved, and posted. Ask what happens when an entry fails validation. Ask if you can rerun a historical period’s posting and get the same result with a documented evidence trail. If the vendor shows you a nice dashboard but can’t walk through failure handling, that’s the answer.

For IFRS 9 solutions for financial institutions, this ERP connectivity question is non-negotiable. Review what IFRS 9 solutions for financial institutions require from their ERP layer specifically.

Audit Trail Depth

The audit trail should cover four things: who designated the hedge, when and with what documentation; which effectiveness testing method was used and on what data; what accounting entries were generated and when they were approved; and what happened if a hedge was de-designated, including the OCI reclassification record.

If the vendor’s audit trail doesn’t cover all four, you will be filling gaps manually during every audit. That’s not a software limitation you work around. It’s a compliance risk you carry.

The IFRS 9 regulatory reporting vendors comparison covers audit trail standards across major platforms in more detail.

Rebalancing Support

IFRS 9 introduced hedge rebalancing as an alternative to de-designation when the hedge ratio changes. It’s one of the most practically useful features of the standard. It’s also the feature that exposes integration weaknesses fastest.

Rebalancing requires updating the hedge ratio, adjusting the documentation, and re-running effectiveness testing — all with a clear record of what changed and why. Ask the vendor how their platform handles this end to end. Not in theory. Walk through it in the demo environment with a real example.

If the answer involves a manual step in a spreadsheet at any point in that process, that’s your answer too.

What Finance Teams in GCC Get Wrong When Selecting Integration Methods

This is worth its own section, because the pattern is specific.

GCC financial institutions, particularly in Saudi Arabia and the UAE, have moved quickly on IFRS 9 adoption for ECL modeling. Many have strong IFRS 9 ECL software in place. But hedge accounting often lags behind, and the integration approach for hedge accounting is chosen separately from the ECL infrastructure — usually by a different team.

That separation creates a problem. Your ECL software may use a different counterparty data model than your hedge accounting platform. Your credit risk assumptions for CVA may not match what your treasury system uses for effectiveness testing. And neither team knows the other’s data architecture well enough to spot the mismatch before an auditor does.

The right approach is to treat hedge accounting compliance software integration as part of a unified IFRS 9 compliance process architecture review — not as a standalone treasury project. It’s a harder conversation internally. It’s a much easier audit.

That said: I don’t have reliable data on how many GCC institutions have run that integrated architecture review vs. those who haven’t. The anecdotal picture from advisory engagements is consistent. A formal study would be more definitive.

For firms evaluating their current IFRS software stack holistically, the enterprise IFRS 9 ECL software selection framework gives a starting point for that broader review.

What You Now Know

- The five integration methods for hedge accounting compliance software each have specific strengths and failure modes. API-first middleware offers the best audit trail for complex multi-system environments. ERP embedding wins on simplicity when your hedging program is standardized. File-based transfers are not a serious compliance option.

- Build vs. buy consistently favors bought platforms by year three, primarily because of regulatory update costs and documentation layer requirements that internal builds underestimate.

- GCC institutions running IFRS 9 hedge accounting need to align their credit risk management software and ECL infrastructure with their hedge platform before the next audit cycle — not after.

Where This Leaves You

Hedge accounting compliance software in finance is not a set-and-forget decision. The IASB’s active post-implementation review of IFRS 9 hedge accounting, launched in Q1 2026, means the standard will evolve. Your integration method has to be built to absorb that change without rebuilding from scratch each time.

The firms that get this right share one thing: they chose their integration architecture before they chose their software. They knew how data would move, how handoffs would be controlled, and how audit evidence would be generated before any vendor demo happened. That sequence matters.

If you’re at the beginning of that process or reconsidering a current approach, the IFRS 9 software solutions comparison and the non-compliant IFRS 9 compliance software risk guide are the two best starting points. Read them together.

The right method is the one your audit team can follow without asking questions. Pick it before the next reporting cycle forces your hand.

See How IFRS TECH’s Integration Advisory Team Reviews Hedge Accounting Architectures →IFRS TECH’s advisory team has reviewed hedge accounting integration architectures across GCC, European, and APAC institutions. We identify control gaps before auditors do.

- ✓ Audit trail gap analysis

- ✓ ERP connectivity review

- ✓ IFRS 9 hedge rebalancing compliance check

Frequently Asked Questions

What integration method works best for IFRS 9 hedge accounting compliance software in finance?

API-first middleware integration offers the strongest audit trail for most organizations because every data movement is logged with timestamps and validation records. For firms running SAP S/4HANA or Oracle as their core ERP, direct ERP embedding can work well when the hedging program is standardized. The worst option is file-based batch transfer, which creates control gaps that regulators and auditors flag.

How does hedge accounting compliance software connect to ERP systems for IFRS 9?

Most purpose-built platforms — Kyriba, GTreasury, FIS Quantum — use dedicated ERP connectors or API layers to push journal entries, approval records, and audit trail data directly to systems like SAP or Oracle. The connection should handle failed-entry scenarios, support reruns, and keep a timestamped record of every posting cycle to satisfy IFRS 9 documentation requirements.

What is the difference between a TMS-native integration and an API-first hedge accounting platform?

A TMS-native integration keeps hedge accounting inside your treasury management system, which handles everything from exposure identification to ERP posting in one environment. An API-first platform uses a middleware layer to connect separate systems with documented data flows. TMS-native is simpler but creates vendor dependency. API-first is more flexible but requires more technical upfront work to build and maintain.

Should GCC banks build or buy hedge accounting compliance software?

Buy. Building internally underestimates two costs: the documentation layer that IFRS 9 audits require and the ongoing cost of regulatory updates. When the IASB amends IFRS 9, as it did in May 2024 for electricity contracts, vendors push updates. Internal builds get a remediation project. By year three, the total cost of ownership for built systems consistently exceeds purchased platforms.

How does credit risk management software connect to hedge accounting under IFRS 9?

Under IFRS 9, Credit Valuation Adjustment affects derivative fair values and can influence hedge effectiveness results. If your credit risk management software doesn’t feed CVA data directly into your hedge accounting platform, you have a gap in your effectiveness testing process. Most firms discover this during their first IFRS 9 audit. The fix requires cross-functional alignment between treasury, credit risk, and finance teams before integration design begins.