TL;DR

Most finance teams running IFRS compliance on spreadsheets don’t see the risk until it’s too late. IFRS compliance software solutions exist precisely because spreadsheets weren’t built for complex, multi-variable IFRS calculations. Research shows 94% of business spreadsheets contain errors. For IFRS 9, IFRS 16, and IFRS 17 reporting, that’s not a process issue. That’s a compliance failure waiting to happen. This article breaks down the real dangers hiding in your spreadsheet-based ifrs reporting solution, from broken audit trails and version control gaps to data errors that trigger regulatory scrutiny. Read on to find out if your current ifrs system software is putting your organization at risk, and what it takes to fix it.

Hidden Risks in IFRS compliance software solutions Built on Spreadsheets

You’ve probably seen it before. A finance team running IFRS compliance software solutions on a web of spreadsheet files, each linked to the next, all managed by one or two people who know exactly where everything is. It feels familiar. It feels controllable. It’s not.

Research shows that 94% of business spreadsheets used in decision-making contain errors. For organizations handling complex IFRS reporting, that’s not a process risk. That’s a compliance risk.

This article breaks down why spreadsheets fall short as IFRS compliance software solutions, where the real dangers hide, and what signals tell you it’s time to think differently.

Why IFRS compliance software solutions Fail with Spreadsheets

The problem isn’t that spreadsheets are bad tools. The problem is that IFRS compliance is not a spreadsheet task. IFRS 9, IFRS 16, and IFRS 17 all require multi-variable calculations, forward-looking assumptions, and audit-ready documentation. Spreadsheets weren’t built for any of that.

That said, millions of finance teams still rely on them. And that reliance creates real, measurable risk.

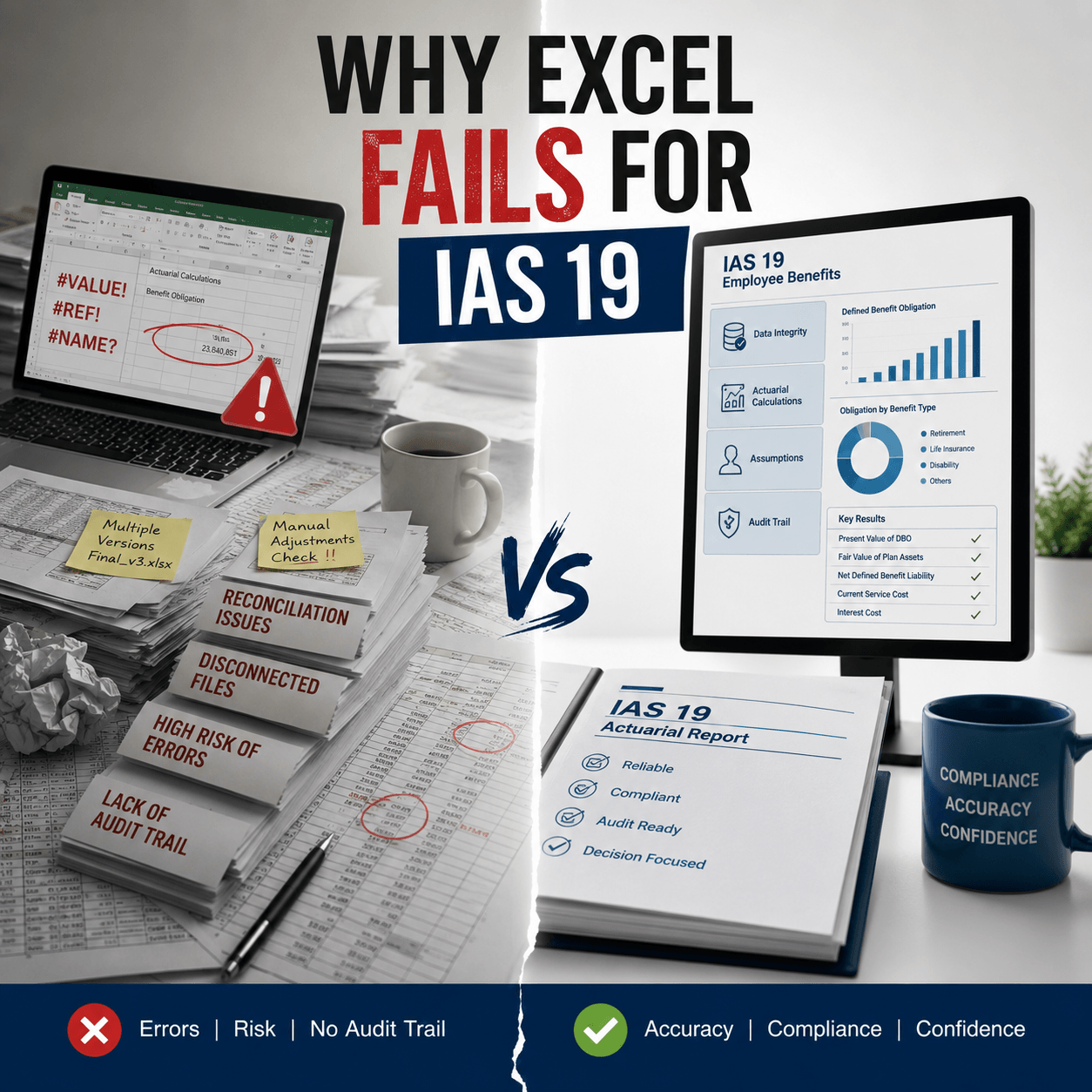

Formula Errors and Broken Links

IFRS calculations involve layers of inputs. Probability of default, loss given default, and exposure at default interact across time horizons and scenarios. One broken cell reference, one pasted formula that doesn’t update correctly, and your entire provision schedule shifts without warning.

Broken links between data sources cause what analysts call “silent failures.” The file looks fine. The numbers calculate. But the outputs are wrong, and nobody knows until an auditor finds it.

Version Control and Audit Trail Gaps

Think about how your team currently tracks changes to IFRS models. If the answer involves file names like “ECL_model_final_v3_REVISED_USE THIS ONE.xlsx,” you already know the problem.

Spreadsheets have no native version control. There’s no log of who changed what, when, and why. For IFRS 9 staging decisions and IFRS 16 remeasurements, auditors expect exactly that kind of traceability. Without it, you’re exposed.

Data Integration and Quality Issues

IFRS models pull data from multiple systems: loan management platforms, general ledgers, external economic feeds, and actuarial models. Manually pulling that data into a spreadsheet introduces inconsistency at every step.

A field renamed in one system, a date format that doesn’t match, a manual copy that skips a row. These are small errors that compound into large restatements. In just the first 10 months of 2024, 140 public companies told investors that previous financial statements were unreliable and required restatements.

Key Risks in Manual Financial Models

Manual IFRS models aren’t just error-prone. They’re structurally fragile. The risks compound as portfolios grow and reporting cycles become more frequent.

Inconsistent Assumptions and Calculations

PD and LGD assumptions in IFRS 9 models should be applied consistently across reporting periods. In a spreadsheet environment, manual overrides happen. Different team members apply different rounding conventions. Macroeconomic overlays get updated in one tab but not another.

For an ifrs reporting solution to be audit-ready, assumptions must be governed and applied uniformly. Spreadsheets don’t do that.

Weak Scenario Analysis and Adjustments

IFRS 9 requires forward-looking information, including multiple economic scenarios weighted by probability. Running that in a spreadsheet requires complex conditional logic that breaks under stress testing. Large scenario runs cause performance issues, timeouts, and incomplete outputs.

What’s interesting is that the failure often doesn’t show up as an error message. The file just produces an output that looks reasonable, even when the underlying scenario logic is incomplete.

Dependence on Key Personnel

Here’s the thing: most spreadsheet-based IFRS models only one or two people fully understand. When those people leave, go on leave, or are simply unavailable at quarter close, the model becomes a black box.

That’s not a documentation problem. That’s an operational risk that regulators in markets like the UAE and Saudi Arabia are increasingly calling out in inspection findings.

How Spreadsheet Errors Impact Financial Reporting

Errors in IFRS models don’t stay inside the finance function. They flow through to financial statements, regulatory filings, and investor disclosures.

Misstated Financial Results

An IFRS 9 provision that’s understated by 5% on a large loan book isn’t a rounding issue. It’s a material misstatement. It affects profit before tax, regulatory capital ratios, and dividend calculations.

88% of spreadsheets contain errors. That figure isn’t theoretical. It means most organizations relying on spreadsheet-based IFRS tools are reporting on numbers that can’t be fully trusted.

Increased Audit Findings and Compliance Risks

Auditors reviewing IFRS 9 ECL models look for documentation of methodology, evidence of model validation, and a complete change log. Spreadsheets don’t produce any of that automatically.

As a result, audit findings in IFRS-related areas have increased. Teams spend significant time reconstructing decisions after the fact, which is expensive and often incomplete.

Profit Volatility and Capital Pressure

Inconsistent assumptions from one period to the next cause provision volatility that’s hard to explain. Analysts and investors notice when loss allowances jump or drop sharply without clear economic cause.

That kind of volatility creates pressure on capital adequacy, triggers analyst questions, and, in regulated environments, can draw regulatory scrutiny. Because of that, finance teams end up spending more time explaining their numbers than improving them.

Governance and Control Challenges

Beyond the technical errors, spreadsheet-based IFRS processes create serious governance gaps. These gaps tend to be invisible until an audit or regulatory review exposes them.

Lack of Transparency and Documentation

Good governance requires that any person reviewing an IFRS model can trace every assumption back to its source. That means documented methodology, traceable data inputs, and a clear record of approvals.

In a spreadsheet environment, that documentation is usually informal. It lives in email threads, meeting notes, and individual memory. That’s not documentation. That’s risk.

Model Validation Limitations

IFRS 9 and IFRS 17 both require periodic model validation. Validating a complex, interlinked spreadsheet model is technically difficult and time-consuming. You can’t run automated validation checks. You can’t diff two versions of a model in a structured way.

For ifrs compliance technology to meet regulator expectations, model governance needs to be built into the system. A spreadsheet can’t deliver that.

Regulatory Compliance Gaps

Regulatory expectations around IFRS tools are increasing. Central banks and financial regulators across global markets expect institutions to maintain controlled, documented processes for expected credit loss estimation and lease liability calculation.

Spreadsheet processes regularly fail these expectations. Breaches with a noncompliance factor cost $174K more on average and $4.61M overall in 2025. The financial exposure from a compliance gap is real and growing.

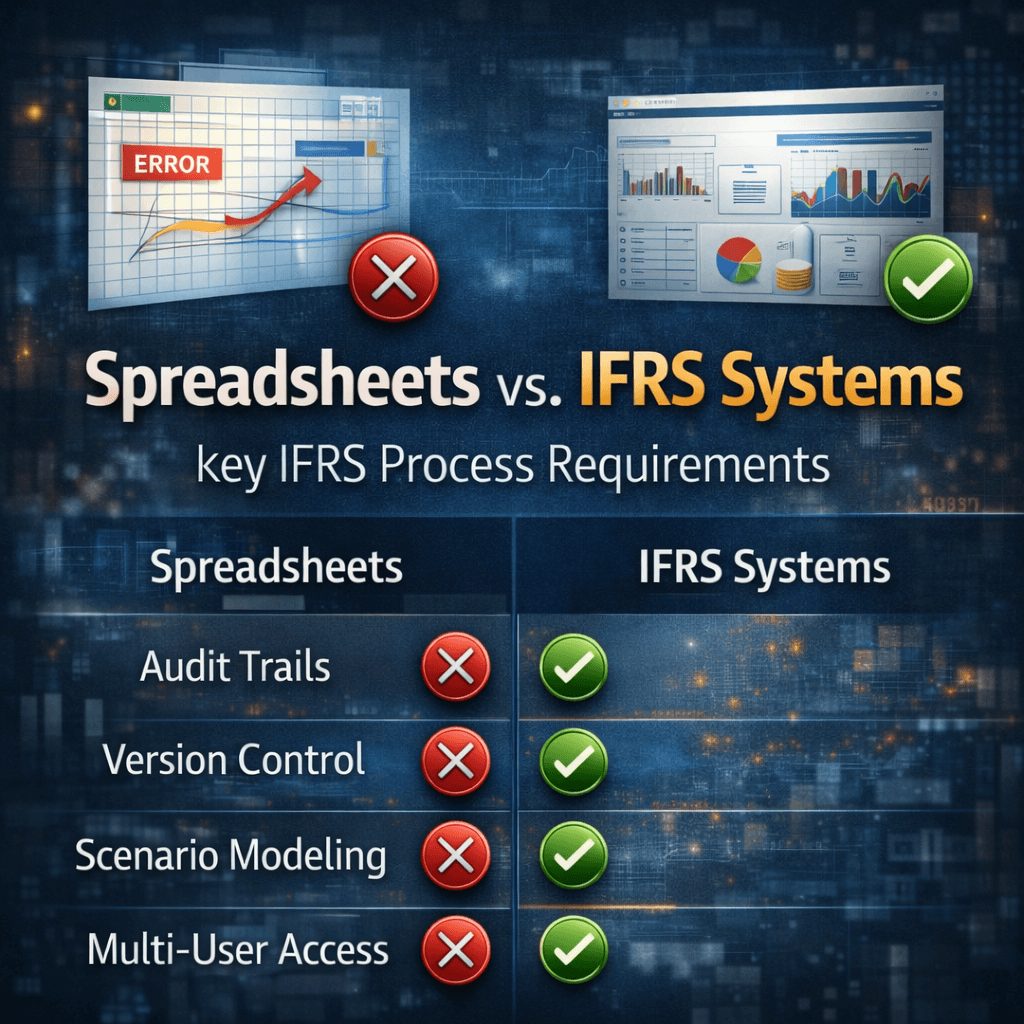

Spreadsheet vs IFRS compliance software solutions

The comparison isn’t about complexity or cost. It’s about fitness for purpose. IFRS compliance has specific technical requirements that spreadsheets weren’t designed to meet.

Accuracy and Automation Benefits

Purpose-built IFRS systems apply calculation logic consistently across every record, every period, and every scenario. There’s no formula drift, no copied-cell errors, and no manual overrides that go unlogged.

Automation also means that when inputs change, outputs update systematically. You’re not chasing broken links across seventeen tabs.

Scalability and Performance

70% of CFOs still rely heavily on Excel for planning, forecasting and reporting. That reliance becomes a performance bottleneck as portfolios grow. A 50,000-loan book in a spreadsheet-based ECL model doesn’t run efficiently. Stress testing across multiple scenarios can take hours, or simply crash.

Dedicated IFRS tools process large data volumes without performance degradation. Scenario runs that take hours in a spreadsheet take minutes in a structured system.

Security and Data Control

Spreadsheets circulate by email. They’re saved to desktops, shared drives, and USB drives. Access controls are weak or nonexistent. You can’t track who opened a file, who changed a cell, or who emailed a version to an external party.

In contrast, purpose-built IFRS platforms maintain role-based access, full activity logs, and centralized data storage. That’s what regulators and auditors want to see.

When to Replace Spreadsheets with IFRS Software

Knowing when to move is just as important as knowing why. Some organizations wait until a crisis forces the decision. Others identify the warning signs early.

Warning Signs and Risk Indicators

You’re probably past the safe threshold if any of the following are true. Your IFRS model is maintained by fewer than three people. Quarter-close consistently takes more than two weeks. Auditors have flagged methodology documentation as insufficient. You’ve had to restate provisions in the last two years.

These aren’t edge cases. They’re patterns that show up repeatedly in organizations that delayed the transition.

Business and Regulatory Triggers

Regulatory triggers often accelerate the decision. A new central bank guideline on ECL model governance, a change in IFRS standard interpretation, or an external audit finding can all create the pressure that moves an organization from spreadsheets to a controlled system.

Growth is another trigger. Acquisitions, new product lines, and entry into new markets all increase the complexity of IFRS processes beyond what spreadsheets can handle reliably.

Best Practices to Reduce Spreadsheet Risk

If a full transition isn’t immediate, there are steps that reduce risk in the interim. These aren’t substitutes for proper systems, but they close some of the most dangerous gaps.

Strengthening Controls and Audit Trails

At a minimum, implement a formal change log for every IFRS model. Every modification should record who made the change, what changed, and why. This should be stored separately from the spreadsheet itself.

Model reviews should involve at least two qualified people who can independently verify the outputs. One-person models are an audit finding waiting to happen.

Improving Data Integration and Governance

Standardize data extraction processes so that inputs to IFRS models come from a single, controlled source. Manual data entry into IFRS calculations is where most errors originate.

Create formal documentation for every assumption used in your IFRS models. This documentation should be updated at every reporting period and approved by a senior responsible person.

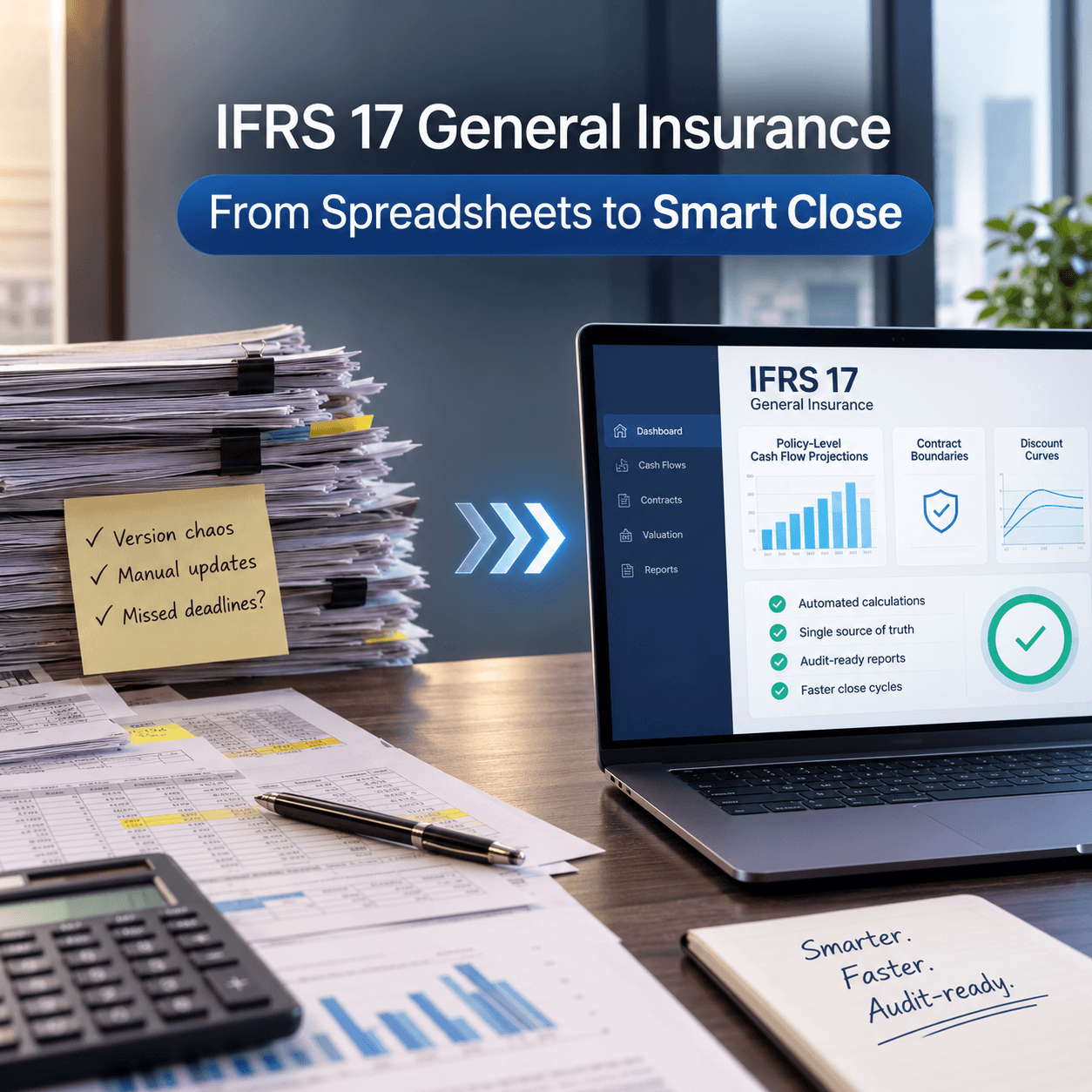

How to Transition to IFRS compliance software solutions

When you’re ready to move, the transition process matters. A poorly managed migration introduces new risks while trying to eliminate old ones.

Step-by-Step Implementation Guide

Start with a complete inventory of your current spreadsheet-based IFRS processes. Document every calculation, every data source, and every assumption currently in use. This baseline is essential for any system implementation.

From there, run parallel calculations between your existing spreadsheets and the new system for at least two reporting periods. Differences need to be investigated and resolved before you decommission the manual process.

Then, train your team on the new system before go-live. User error during transition is a real risk, and it can be avoided with proper preparation.

Build vs Buy Decision Framework

Most organizations with complex IFRS requirements are better served by a purpose-built system than by a custom build. Custom builds carry the same documentation and governance risks as spreadsheets if they aren’t properly managed.

The key question is whether your organization’s requirements are standard enough for a vendor solution, or specialized enough to require custom development. In most cases, the IFRS calculations themselves are standard. What varies is the data architecture and integration requirements.

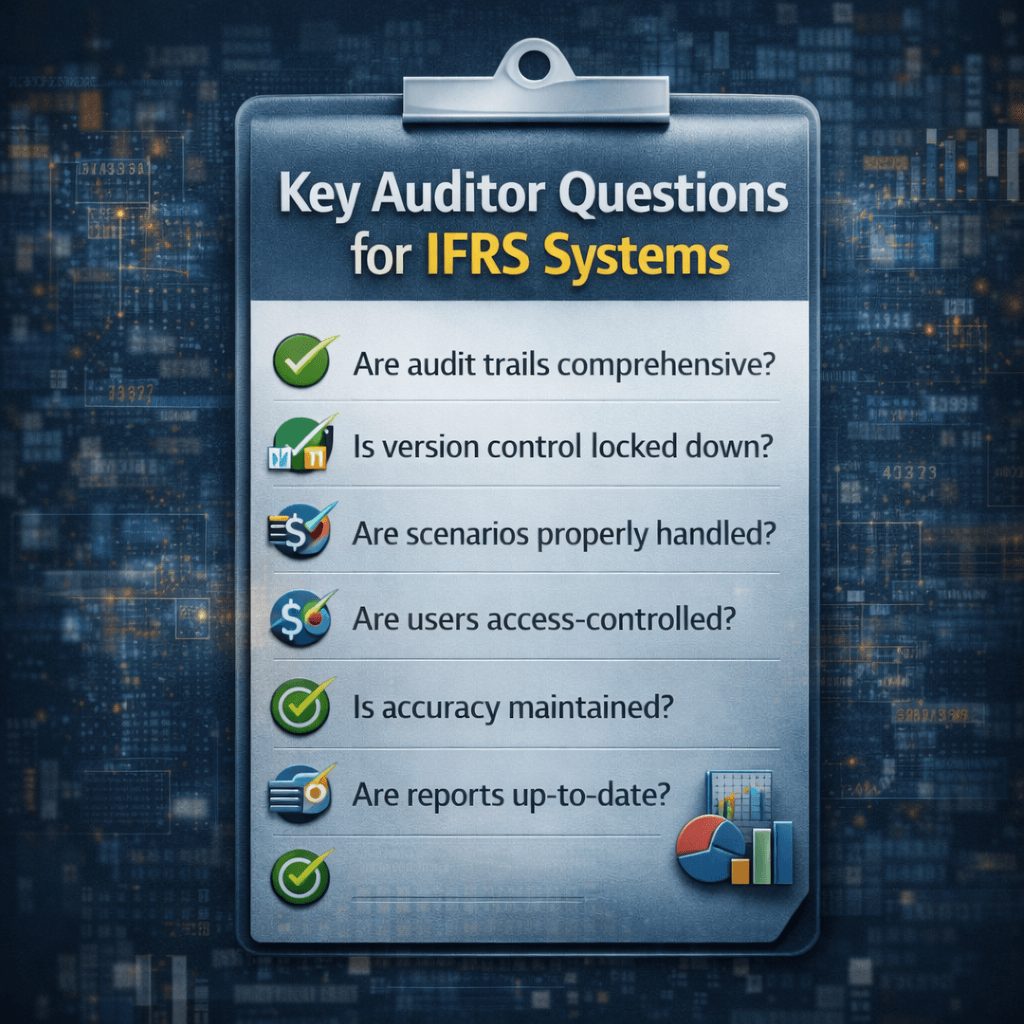

What Auditors Expect from IFRS Systems

Auditors reviewing IFRS processes have a clear set of expectations. They want to see a system that produces traceable, reproducible outputs. They expect documented methodology that matches actual calculation logic and look for evidence of model validation and change control.

When those expectations aren’t met, audit findings follow. Remediation is expensive, time-consuming, and disruptive to normal reporting cycles. Investing in a controlled system upfront is far less costly than managing audit findings after the fact.

FAQs on IFRS compliance software solutions

Can spreadsheets meet compliance requirements?

Spreadsheets can produce IFRS-compliant outputs in simple cases, but they don’t meet the governance, documentation, and auditability requirements that regulators increasingly expect. For organizations with significant loan portfolios, lease volumes, or insurance liabilities, spreadsheet-based processes carry material compliance risk.

What are the biggest spreadsheet risks?

The main risks are formula errors that go undetected, absent audit trails, version control failures, dependence on key personnel, and poor scalability. Any one of these can cause a material misstatement or an audit finding. In practice, most organizations relying on spreadsheets face several of these risks simultaneously.

How do firms improve reporting accuracy?

The most effective steps are centralizing data inputs, removing manual data entry from IFRS calculations, implementing formal change controls, and moving to purpose-built IFRS tools. Organizations that combine structured data governance with automated calculation logic see significant reductions in error rates and audit findings.

The Real Cost of Waiting

Spreadsheet-based IFRS processes feel manageable right up until they aren’t. Errors accumulate silently. Audit exposure builds over time. And when the problem surfaces, it usually surfaces at the worst possible moment.

The risks of spreadsheets in IFRS compliance software solutions for compliance aren’t theoretical. They’re documented in restatements, audit findings, and regulatory actions across global markets. You don’t need a crisis to justify improving your process. The data already makes the case.

If your organization is carrying spreadsheet risk in your IFRS reporting, the team at Prima Consulting can help you assess where the gaps are and what a controlled, audit-ready process looks like in practice.