TL;DR

If your team still relies on spreadsheets for IBNR, you’re carrying more risk than you think. IBNR software gives non-life insurers a faster, more accurate way to manage loss reserving, from automated claims data processing to built-in regulatory compliance. This guide covers how end-to-end IBNR solutions work, what features matter most, and how they compare to manual methods across accuracy, scalability, and reporting. You’ll also find a practical framework for choosing the right ibnr solution for your organization. Read on to decide if it’s time to make the switch.

IBNR Software for Non-Life: End-to-End Solutions Evaluated

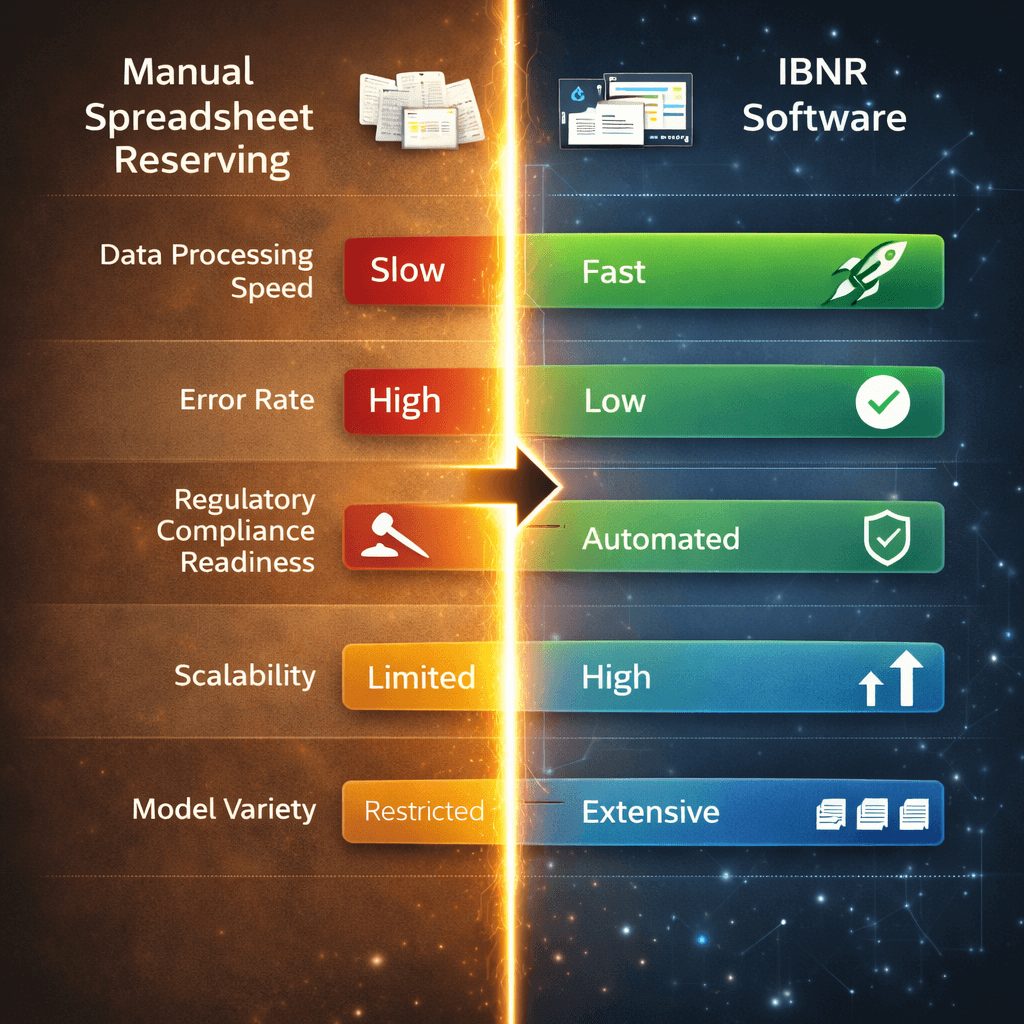

Your actuarial team spends days rechecking spreadsheet formulas. A single error in a reserve triangle can throw off your IBNR software estimate by millions.

That’s a real problem for non-life insurers today. Gross claims payments in the non-life sector grew by 7.5% in 2024, according to the

Gross claims payments in the non-life sector grew by 7.5% in 2024 (src). That growth puts direct pressure on reserve accuracy. And with the non-life insurance market expected to reach $5.18 trillion by 2029 (src), the stakes keep rising.

So, what separates IBNR software from the manual process your team might still rely on? This guide breaks it down clearly.

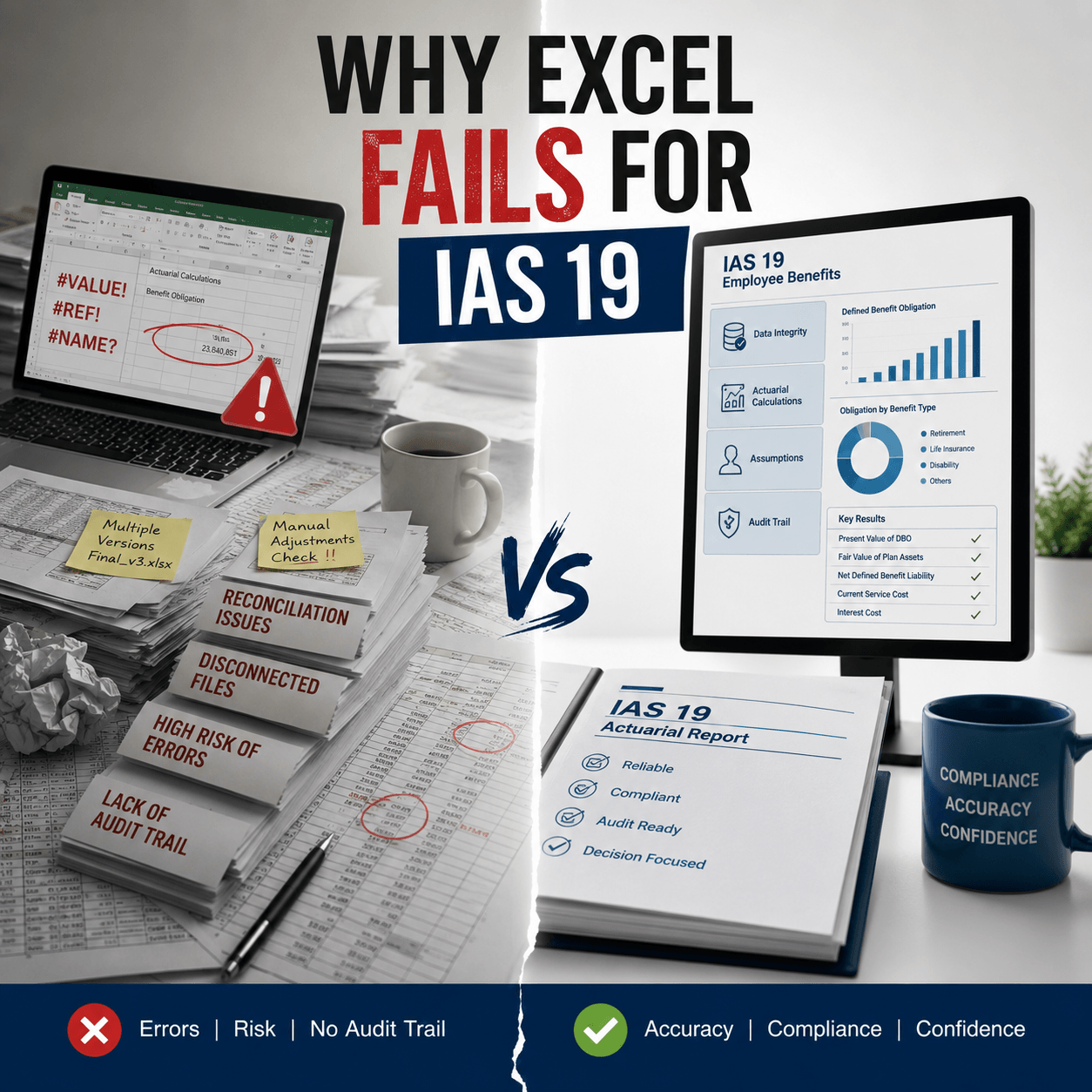

What Is IBNR Software in Non-Life Insurance?

IBNR stands for Incurred But Not Reported. These are claims that have already happened but haven’t been filed with the insurer yet.

Non-life insurers must estimate this liability every reporting period. The challenge is that you’re projecting future claim activity using historical data, and that data is never perfect.

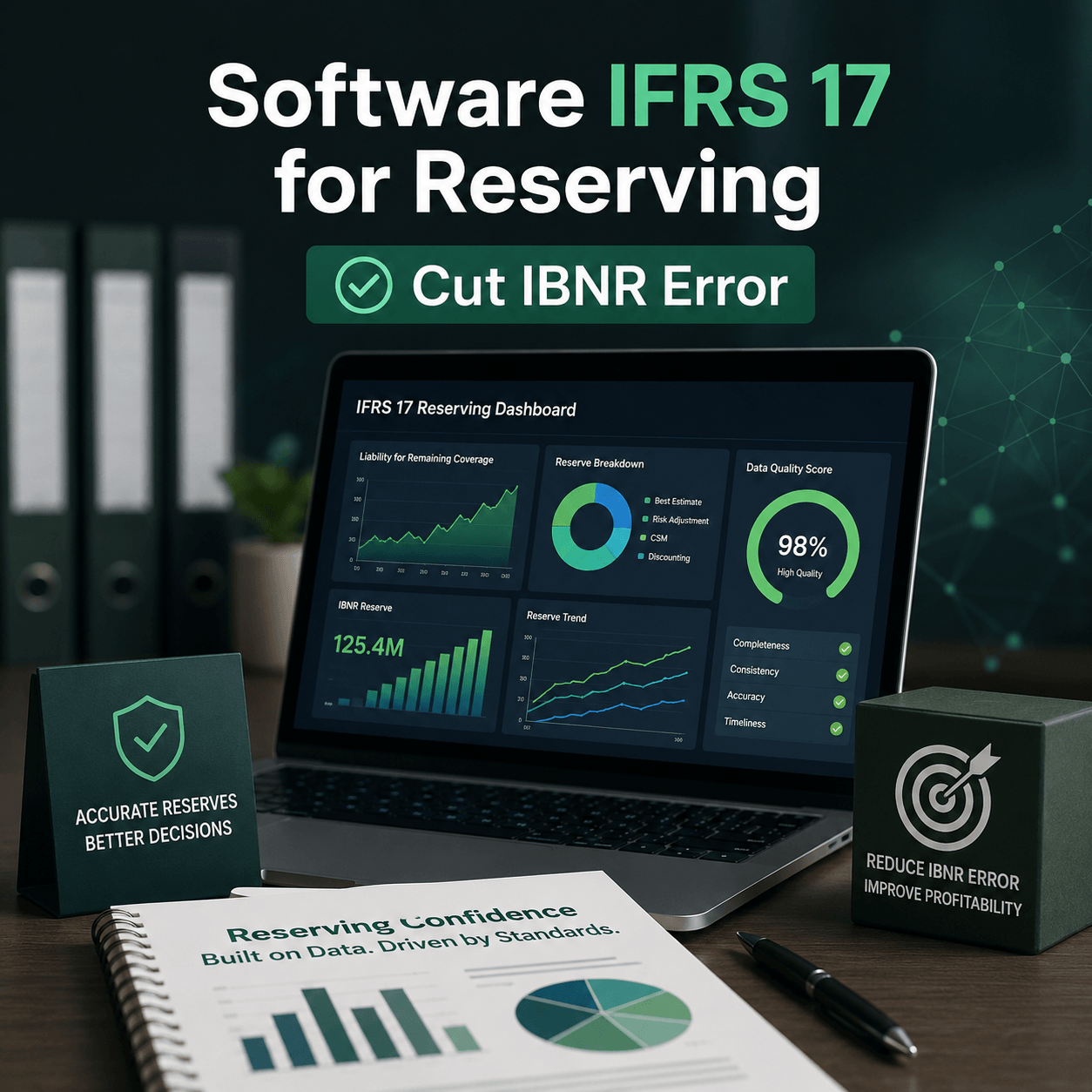

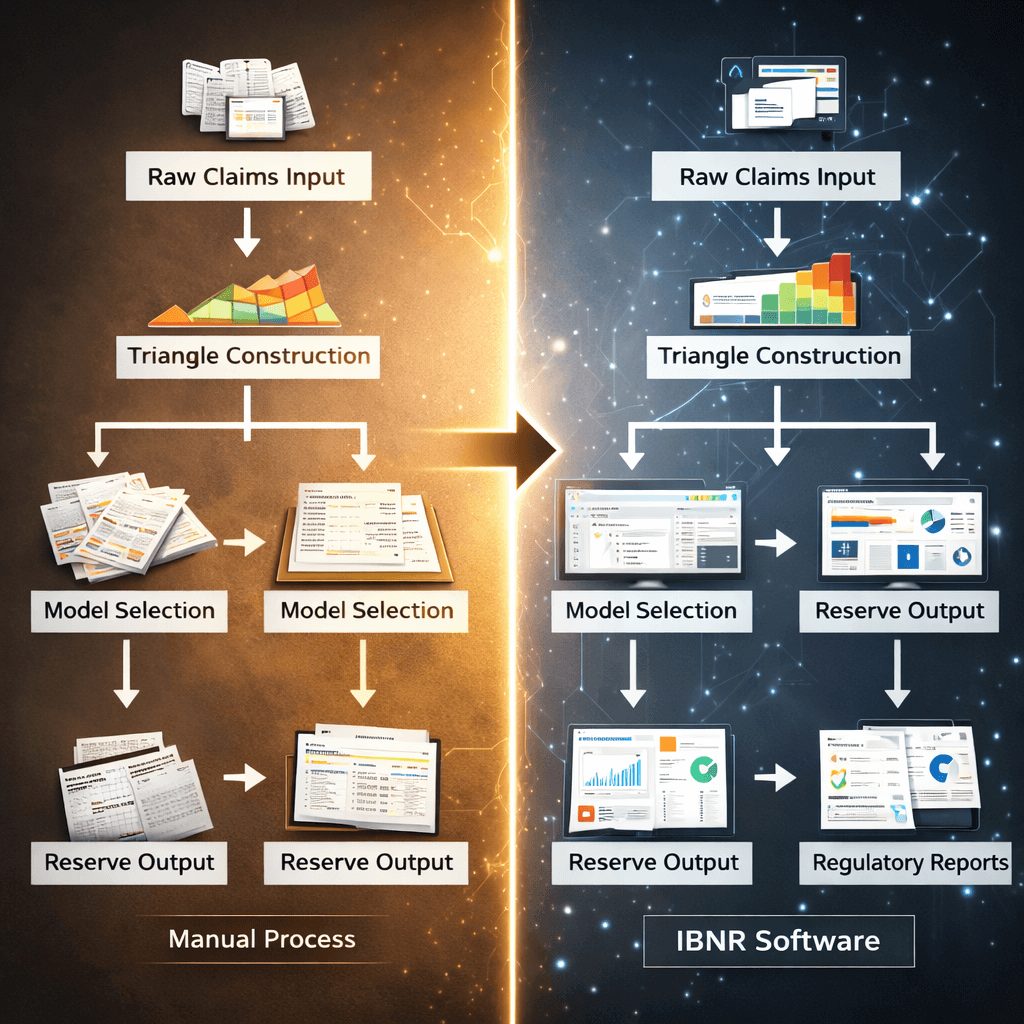

IBNR software is a purpose-built tool that automates this projection process. It replaces manual spreadsheet calculations with structured data pipelines, actuarial models, and built-in regulatory controls.

To put it simply, IBNR software does what Excel can’t: it handles large datasets at scale, runs multiple models in parallel, and flags anomalies in real time.

Key Features of End-to-End IBNR Software

Automated Claims Data Integration

Manual systems require actuaries to pull, clean, and organize claims data before any analysis begins. That takes time, and it introduces room for error.

Good IBNR software connects directly to your claims and policy systems. It ingests raw data, normalizes it, and feeds it into reserving models automatically. From there, your team focuses on interpreting results, not preparing inputs.

Real-Time Reserving and Reporting

Batch processing works for monthly closes. But market conditions shift, and your reserve estimates should reflect that quickly.

Modern IBNR platforms offer real-time or near-real-time dashboards. Actuaries can view updated triangles, development patterns, and reserve movements without waiting for a scheduled run.

Actuarial Modeling and Forecasting Tools

The core of any IBNR tool is its modeling engine. Look for support for Chain Ladder, Bornhuetter-Ferguson, Cape Cod, and stochastic methods like bootstrapping.

What’s interesting is that leading platforms now combine traditional methods with machine learning layers. This lets you keep the actuarial rigor your regulators expect while improving accuracy on volatile lines.

How IBNR Software Improves Reserving Accuracy

Claims Lag and Development Tracking

Claim lag, the time between an incident and when it’s reported, varies widely across lines of business. Property claims often settle fast. Liability claims can drag for years.

IBNR software tracks lag patterns automatically across historical periods. It builds lag distributions by line of business, so your development assumptions stay grounded in your own data, not industry averages.

Loss Development Triangle Methods

Loss development triangles sit at the heart of non-life reserving. They show how paid and incurred losses evolve across accident years and development periods.

Software platforms build and update these triangles automatically. They also let you run sensitivity tests across multiple triangle configurations, a process that can take days in Excel but minutes in a dedicated ibnr solution.

Frequency and Severity Modeling

Separating claim frequency from claim severity gives actuaries a cleaner view of where reserve risk is coming from. A spike in severity on auto liability looks very different from a spike in claim counts.

End-to-end IBNR platforms run frequency-severity splits as a standard output. You get a more detailed picture of your liability without any manual segmentation work.

IBNR Software Architecture and Data Flow

Core Data Inputs for Reserving Models

Accurate IBNR estimates start with clean, complete data. The key inputs include paid losses, incurred losses, claim counts, earned premiums, and exposure data by accident year.

Software platforms include built-in data quality checks. They flag missing values, outliers, and inconsistencies before the data reaches the model. That’s a step most manual workflows skip entirely.

Integration with Policy and Claims Systems

A standalone reserving tool only gets you so far. The real value comes when IBNR software connects to your core systems, including your policy administration platform, claims management system, and general ledger.

API-first architectures make this possible without expensive custom development. You configure the connections once, and the data flows automatically each period.

Batch vs Real-Time Processing

Most non-life insurers still run monthly reserve cycles. Batch processing handles this well, pulling a full data snapshot at month-end and running all models in a single scheduled job.

Real-time processing is better suited for high-volume lines like auto or workers’ compensation, where claim activity is continuous. The right architecture depends on your line mix and how often your reserves need to move.

Regulatory Compliance and Reporting Requirements

Solvency and Capital Adequacy Considerations

Non-life insurers operating under Solvency II must calculate best estimate liabilities and risk margins with documented, auditable methods. IFRS 17 adds contractual service margin requirements that affect how reserves are presented in financial statements. Learn more about IFRS 17 advisory support for these requirements.

Manual processes struggle here. They can produce the right numbers, but they can’t always prove how those numbers were reached. Software platforms maintain full audit trails by default.

Audit and Financial Reporting Standards

Regulators and auditors want to see method documentation, assumption justifications, and sensitivity analyses. That’s a lot to maintain in spreadsheets, and it often requires separate documentation files that can fall out of sync.

IBNR software stores all of this inside the platform. Assumptions, model selections, and override decisions are logged automatically, so your audit pack is ready when you need it.

Data Governance and Accuracy Controls

Data governance is a growing concern as non-life reserves grow in complexity. Software platforms include role-based access controls, input validation rules, and reconciliation checks between source data and model inputs.

Because of that, errors that once slipped through manual reviews get caught at the data intake stage, before they ever reach a model.

Advanced Analytics in Modern IBNR Software

Machine Learning in Reserving Models

Traditional actuarial methods use aggregate triangle data. Machine learning models can use individual claim records, policy characteristics, and even external data like weather events to improve prediction.

Research from Pinnacle Actuaries shows that ML approaches outperform baseline chain ladder methods on commercial auto liability when applied to granular policy-level data. That said, ML works best as a complement to traditional methods, not a replacement. Interpretability still matters to regulators.

Predictive Analytics for Claims Trends

Some IBNR platforms include predictive modules that identify emerging trends before they fully develop in the triangle data. You might spot a shift in severity patterns on general liability two or three quarters earlier than traditional methods would reveal it.

That’s actionable intelligence. It lets pricing and underwriting teams respond to reserve signals in real time, not after the fact.

Scenario Testing and Stress Analysis

Stress testing reserve estimates is increasingly expected by regulators and internal risk committees. What happens to your IBNR if reported claims come in 20% above development factors? What if tail risk materializes on a long-tail liability book?

IBNR software runs these scenarios quickly. You can define stress parameters, run multiple scenarios in parallel, and compare outputs side by side without rebuilding your model each time.

Common Challenges in IBNR Implementation

Data Quality and Historical Gaps

The biggest risk in moving from manual to software reserving isn’t the tool itself. It’s the data underneath it. Years of inconsistent coding, legacy system migrations, and manual adjustments can leave gaps that inflate uncertainty in your development factors.

Most implementations include a data remediation phase. Plan for it. A clean historical dataset is what makes the model reliable from day one.

System Integration Complexity

Connecting IBNR software to existing claims and policy systems takes time, especially in organizations running older core platforms. API compatibility, data mapping, and testing all need dedicated resources.

Still, the upfront integration work pays off quickly. Teams that previously spent two weeks on a reserve cycle report cutting that to two or three days after implementation.

Coordination Across Actuarial and Finance Teams

Reserve numbers don’t live in a vacuum. They feed directly into financial statements, regulatory filings, and pricing decisions. That means actuarial and finance teams need to agree on data sources, timing, and how adjustments are approved.

Software platforms help here by creating a single source of truth. When both teams pull from the same system, version control disputes and reconciliation meetings become far less frequent.

How to Choose the Best IBNR Software

Build vs Buy Decision Framework

Building a custom IBNR tool in-house is possible, but it’s rarely the right choice. The ongoing maintenance cost of a proprietary model, including model validation, regulatory updates, and staff turnover, often exceeds the cost of a commercial platform within three years.

Buying gives you a tested methodology, vendor support, and a product roadmap aligned with regulatory changes. The build option makes sense only if your reserving requirements are genuinely unique and no off-the-shelf solution can meet them.

Key Evaluation Criteria and Checklist

When assessing ibnr software comparison insurers use to make decisions, focus on these areas: actuarial model coverage, integration capabilities, audit trail quality, regulatory reporting alignment, user interface for actuarial staff, and total cost of ownership including implementation.

You’ll also want to check vendor experience specifically in non-life. A platform built primarily for life or health insurance may not handle property and casualty triangles with the same depth. Reviewing ifrs 17 software solutions can give you a useful reference point for what regulatory-grade tools look like in practice.

Scalability and Cloud Considerations

Scalability ibnr spreadsheets simply can’t match is a key advantage of cloud-based platforms. As your portfolio grows or you expand into new lines, a cloud-native tool scales without additional infrastructure investment.

Cloud deployment also simplifies version management and disaster recovery. Your data and models are backed up automatically, and your team can access the platform from any location.

[IMAGE PLACEHOLDER 4: Near end of article. Suggested type: Decision tree or checklist graphic. Visual intent: A visual checklist or decision tree that helps actuarial teams evaluate whether they’re ready to move from manual to software-based IBNR. Include criteria like data readiness, team capacity, regulatory requirements, and system integration complexity. Clean, professional design with brand-neutral colors.]

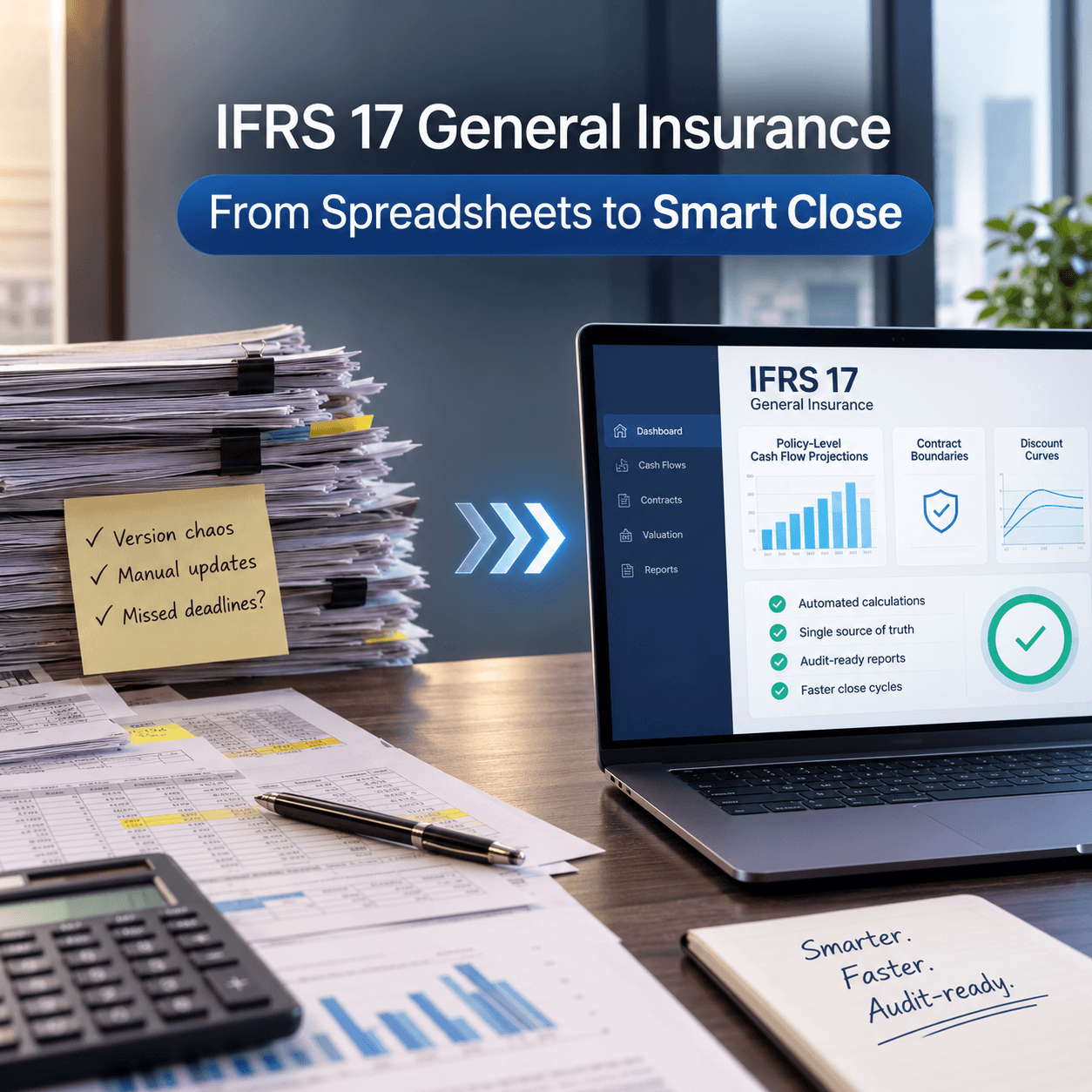

What Are the Benefits of End-to-End IBNR Solutions?

End-to-end platforms connect every step of the reserving process, from data ingestion through model output to regulatory reporting. That removes handoff points where errors typically enter.

The core benefits are faster close cycles, better audit readiness, more consistent reserve estimates, and lower operational risk. Teams also report that software platforms free up senior actuarial time from spreadsheet maintenance to actual analysis.

Global natural catastrophe insured losses exceeded $100 billion in 2024

(src). Events at that scale stress-test reserve adequacy across the entire non-life market. An end-to-end platform that can run catastrophe scenarios quickly isn’t a nice-to-have. It’s a core risk management tool.

How Does IBNR Software Support Financial Forecasting?

Reserve estimates don’t just fulfill a regulatory obligation. They directly affect your reported profitability, capital position, and pricing decisions.

Manual vs automated reserving IFRS non-life comparisons consistently show that automated platforms produce more stable reserve estimates quarter to quarter. That stability helps finance teams build more reliable forecasts and reduces the variance that can surprise investors and regulators alike.

IBNR software also supports forward-looking scenario analysis. You can model how your reserves would move under different claims development assumptions and show your board a range of outcomes rather than a single point estimate.

What Are the Best Practices for IBNR Modeling?

Start with your data. No model compensates for incomplete or inconsistent historical claims data. Before selecting a platform, audit your input quality and plan for any remediation work.

Run multiple methods in parallel. Chain Ladder is standard, but it shouldn’t be your only method. Bornhuetter-Ferguson adds stability on immature accident years. Stochastic methods quantify the range of outcomes. Using all three gives you a more complete picture.

Document every assumption. Your model selections, parameter choices, and manual overrides should be recorded in the system, not in a separate memo that might not be updated next quarter.

Review frequency matters too. Reserve estimates should be updated at least quarterly. Lines with high claim volatility, like casualty or professional liability, may warrant monthly reviews.

FAQs About IBNR Software

What is a typical IBNR reserve percentage?

There’s no universal answer. IBNR as a percentage of total reserves varies significantly by line of business and tail length. Short-tail lines like property may carry IBNR of 10 to 20 percent of total reserves. Long-tail lines like general liability or professional indemnity can carry IBNR above 50 percent. Your specific mix, development patterns, and claims reporting processes all affect the figure.

How often should IBNR models be updated?

Most non-life insurers update IBNR estimates at least quarterly. High-volatility lines or lines with rapid claims development benefit from monthly updates. Regulatory requirements under IFRS and Solvency II also influence the minimum frequency. Software platforms make frequent updates practical without a proportional increase in actuarial workload.

What data is required for accurate IBNR calculations?

Core inputs include paid losses by accident year and development period, incurred losses, claim counts, earned premiums, and exposure data. You’ll also need consistent historical data across multiple development periods to build reliable loss development factors. Software platforms include data validation steps that check completeness and flag anomalies before they reach the model.

What is the difference between IBNR and IBNP?

IBNR covers claims that have occurred but haven’t been reported to the insurer at all. IBNP, Incurred But Not Paid, covers claims that have been reported but not yet settled. IBNR is generally more uncertain because it requires estimating both the number of unreported claims and their eventual cost. Most reserving platforms calculate both separately and then combine them into a total outstanding claims estimate.

What’s the Right Next Step for Your Non-Life Reserving Process?

Moving from manual spreadsheets to dedicated IBNR software isn’t just a technology decision. It’s a risk management decision. The accuracy, speed, and regulatory readiness that software delivers are increasingly difficult to replicate manually as portfolios grow and reporting standards tighten.

Global non-life premium growth is forecast at 2.3% annually through 2026 (src), and casualty rates increased 4% globally in Q4 2025 (src). The market isn’t slowing down, and neither are regulatory expectations.

If your team is still managing reserves in spreadsheets, or if your current software doesn’t integrate well with your reporting requirements, it’s worth reviewing what a purpose-built ibnr software platform can change for you.

Prima Consulting works with non-life insurers worldwide on actuarial transformation, IFRS advisory, and reserving technology selection. Visit primaconsulting.org to connect with their team and find the right solution for your organization.