TL;DR

Choosing an IFRS 17 end-to-end non-life solution is one of the most consequential decisions your finance and actuarial teams will make. This guide breaks down every must-have feature, from calculation engines and CSM tracking to audit trails and data model integration. You’ll learn which vendor questions actually matter, what red flags to watch for at scale, and how to compare platforms against a clear non-life compliance checklist. If you’re at the decision stage, this is the reference you need before you sign anything.

IFRS 17 End-to-End Non-Life Vendor Criteria for Scale

You’re past the evaluation stage. You know IFRS 17 isn’t optional. Now you’re choosing a vendor to carry that weight, and the wrong pick will cost you more than just time. This guide lays out every must-have for a true IFRS 17 end-to-end non-life solution, from calculation engines to audit trails. It names real platforms, flags real risks, and gives you a clear path forward.

IFRS 17 End-to-End Non-Life Solution Overview

Non-life insurers face a different version of IFRS 17 than their life counterparts. Variable claim patterns, short-duration contracts, and high transaction volumes make the data and computation demands far heavier. That’s why selecting the right IFRS 17 end-to-end non-life solution isn’t just a technical decision, it’s a strategic one.

According to the Actuaries Institute of Australia, 60% of strategic IFRS 17 solutions among Australian and New Zealand insurers are vendor-based. The shift toward purpose-built platforms reflects just how complex in-house builds have become. At the same time, 47% of direct insurers still report significant manual intervention in IFRS 17 processes, which directly limits scalability and month-end close speed.

What defines a scalable IFRS 17 architecture?

A scalable architecture can handle policy volume growth without a rebuild. It separates calculation logic from data storage, supports parallel processing, and runs reconciliations without manual patching. The system’s performance must hold at peak volumes, not just in a demo environment.

Key capabilities of non-life IFRS 17 systems

Non-life systems must handle short-tail and long-tail contracts simultaneously. They need dynamic boundary assessments, rolling coverage unit calculations, and engines that process variable fulfillment cash flows across policy cohorts. Traceability from contract inception to run-off is non-negotiable.

How to Choose the Right IFRS 17 end-to-end non-life solution

Vendor selection starts long before a contract is signed. It starts with asking the right questions and knowing which answers are red flags.

Must-have features in IFRS 17 platforms

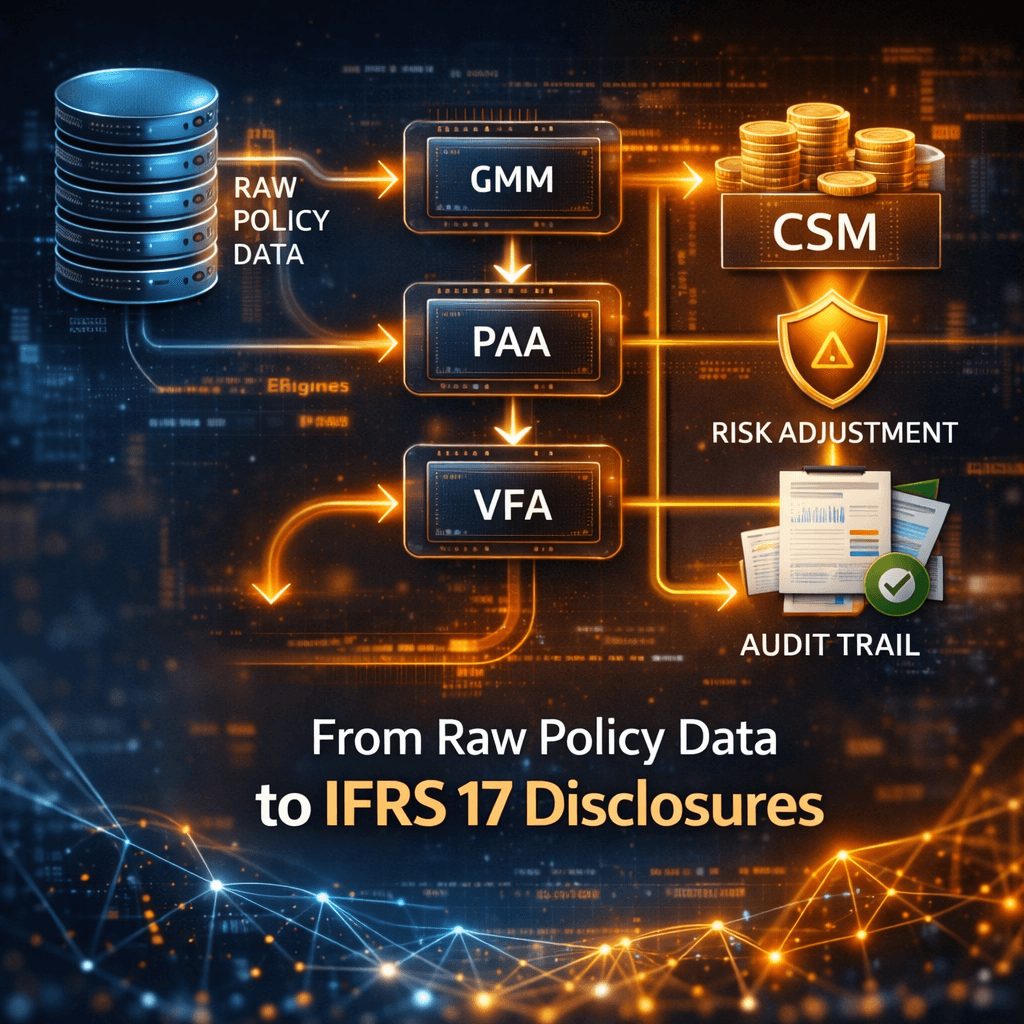

Any platform you shortlist must include a dedicated calculation engine for discounting, risk adjustment, and contractual service margin (CSM) tracking. It must support the General Measurement Model (GMM), Premium Allocation Approach (PAA), and Variable Fee Approach (VFA). If you’re still building your shortlist, reviewing available IFRS 17 software solutions before vendor demos will help you set the right benchmark. Intermediate results tables, full audit trails, and rules engines for contract recognition and separation are baseline requirements, not premium features.

Questions to ask before vendor selection

Start with volume. Ask vendors: “How many policies can your system process per month?” Then move to multi-entity: “Can your platform produce consolidated disclosures across subsidiaries in different jurisdictions?” Push on non-life traceability: “Can you show how your system traces general insurance variability from contract inception through run-off?” Any hesitation on these points is worth noting.

From there, ask about data validation rules, integration connectors for actuarial and finance tools, and how the system manages prior-period restatements. Vendors who answer vaguely on technical specifics are a risk.

Common mistakes in vendor evaluation

Teams often shortlist based on brand recognition alone. That’s a mistake. A well-known vendor may lack specific non-life traceability or struggle with high-volume PAA portfolios. Another common error is skipping proof-of-concept testing. Run your own data through the system before signing anything. Red flags include vague SLAs, generic demo data, and no client references from comparable non-life portfolios.

Core Functional Requirements for IFRS 17

Support for GMM, PAA, and VFA models

A platform must handle all three measurement models, not just PAA. Non-life portfolios often contain contracts that don’t qualify for the simplified approach. Your system needs to apply the correct model at the cohort level and flag exceptions automatically.

Handling high-volume non-life data

The Actuaries Institute of Australia found that 71% of reinsurers ranked data transformation and GIC tagging as a high challenge for scalability. This points directly to a gap in many vendor platforms: they can process data but can’t tag, transform, and reconcile it at the same time without manual steps.

Your vendor should offer automated data transformation pipelines that feed directly into the calculation layer. Manual intervention at this stage breaks auditability and slows close timelines.

CSM, risk adjustment, and reporting accuracy

CSM tracking must be granular enough to support cohort-level disclosure. Risk adjustment calculations need to align with your actuarial team’s probability of sufficiency inputs. For non-life portfolios, reserve estimates depend heavily on how your platform handles incurred but not reported claims, so understanding your IBNR software options before finalizing vendor selection is worth the extra step. Reporting outputs must be auditable, meaning every line in the disclosure must trace back to a specific input, calculation step, and data source.

Data, Integration, and System Scalability

Data governance and audit-ready workflows

Audit readiness isn’t just about storing data. It’s about being able to reproduce any prior-period result on demand. Your platform must log every calculation run, every parameter change, and every adjustment made by any user. This is the foundation of non-life compliance.

According to the same Actuaries Institute study, 30% of participants used prior-month roll-forward simplifications to manage scalability and timeline pressure. While that may pass an initial audit, it creates long-term disclosure risk. An audit-ready platform removes the need for such shortcuts.

Integration with finance, risk, and actuarial tools

Your IFRS 17 system shouldn’t operate in isolation. It must connect with your actuarial models, general ledger, and risk management platform. Look for pre-built connectors to tools like Prophet, Moses, or MoSes Lite, plus open APIs for custom integrations. The data flow between actuarial inputs and IFRS calculations must be automated, not managed through exports and uploads.

Cloud vs. on-premise scalability considerations

Cloud-based IFRS 17 platforms offer faster scaling, lower infrastructure overhead, and easier version upgrades. On-premise solutions give you more control over data residency, which matters in regulated markets with strict data sovereignty rules. A hybrid deployment, where calculations run in the cloud and sensitive data stays on-premise, is worth asking about during vendor demos.

Automation, Performance, and Analytics

Automating IFRS 17 calculations at scale

Full automation means the system runs from data ingestion to disclosure output without manual handoffs. That includes automated cohort grouping, contract boundary checks, and PAA eligibility tests. The best platforms run these checks in parallel across the full portfolio.

Real-time reporting and dashboards

Decision-makers need visibility before month-end close, not after. Real-time dashboards showing CSM roll-forward, loss component tracking, and cash flow variance give your finance and actuarial teams the ability to catch errors earlier. Ask vendors to show you live dashboards using realistic non-life data volumes.

Advanced analytics and forecasting capabilities

Some platforms now include scenario modeling and stress testing against different yield curve assumptions or claims development patterns. This isn’t just a nice feature. For CFOs preparing board presentations, the ability to model IFRS 17 impacts under different scenarios is a practical planning tool.

Governance, Compliance, and Controls

Ensuring regulatory compliance and audit trails

Your platform must produce disclosure-ready outputs that align with IFRS 17 paragraphs 78 to 100 for the statement of financial position and paragraph 101 onward for the statement of profit or loss. Every figure must trace back to its source without manual reconstruction.

Model validation and internal controls

The system should support independent model validation runs, where a second team or external auditor can rerun the same calculations and get the same results. Version-controlled parameters and locked reporting periods prevent after-the-fact edits.

Documentation and transparency standards

All assumption changes, discount rate updates, and risk adjustment revisions must be logged with timestamps and user IDs. This isn’t optional for external audit purposes. It’s also the basis of internal controls under IFRS 17 paragraph 117.

IFRS 17 and IAS 19 Valuation Synergies

Aligning actuarial models across standards

If you’re running both IFRS 17 and IAS 19 valuations, the actuarial inputs often overlap. Discount rates, mortality tables, and liability duration assumptions can frequently be shared across both processes. A platform that supports both standards within a single environment reduces duplication and improves consistency across disclosures.

Shared data and reporting efficiencies

When IFRS 17 and IAS 19 share a common data layer, your team runs one extract instead of two. That cuts close timelines and reduces the risk of inconsistencies between the two sets of disclosures, which external auditors actively look for.

Reducing duplication in valuation processes

Many insurers run parallel actuarial workstreams for IFRS 17 and employee benefits. A shared platform with separate reporting modules eliminates redundant data mapping and parallel reconciliations. That translates directly into fewer person-hours per close cycle.

Implementation and Deployment Strategy

Step-by-step rollout for scalable adoption

Start with a pilot portfolio, ideally one product line with moderate complexity. Run it through the full end-to-end workflow: data ingestion, calculation, disclosure, audit trail. Once that’s validated, extend to the full portfolio in waves. This reduces risk and gives your team time to build platform familiarity.

Timelines, costs, and resource planning

Realistic IFRS 17 implementation timelines for mid-size non-life insurers range from 12 to 24 months, depending on data quality and legacy system complexity. Budget for data migration, parallel run testing, and staff training. Some vendors include implementation in a bundled subscription; others charge separately. Ask for a full total cost of ownership breakdown, not just licensing fees.

Managing change and stakeholder alignment

Finance, actuarial, IT, and internal audit teams all have stakes in the IFRS 17 platform. Get them aligned on requirements before vendor demos. Misalignment at this stage leads to late-stage scope changes that delay go-live and inflate costs.

Build vs. Buy: What’s Best for Scale?

Pros and cons of in-house development

Building in-house gives you full control over the data model and calculation logic. That said, the maintenance burden grows every time the standard is updated or your product portfolio changes. Most insurers who built internally now spend significant resources just keeping the system current.

Benefits of vendor-based IFRS 17 solutions

Vendor platforms come pre-built with IFRS 17 logic, tested against the standard, and updated when interpretations change. For non-life insurers with complex portfolios, this removes a substantial compliance risk. You also get access to a client community and support team who’ve seen your problems before.

Hybrid approaches for flexibility

Some insurers keep specific calculation modules in-house, like bespoke risk adjustment models, while using a vendor platform for everything else. This works when your in-house component has a clear interface with the vendor system and doesn’t introduce reconciliation gaps.

Vendor Comparison Checklist for 2026

Evaluation criteria for scalability and performance

Use these criteria when comparing vendors on a scored basis:

Non-life calculation engine coverage (GMM, PAA, VFA): Does the system handle all three without workarounds?

Policy volume capacity: What’s the largest non-life portfolio the vendor currently processes monthly?

Audit trail completeness: Can every disclosure line be traced back to its source in three clicks or fewer?

Multi-entity and multi-currency support: Does the platform support consolidated group reporting across jurisdictions?

Integration depth: How many actuarial and finance tools does it connect to natively?

Intermediate results tables: Can you access pre-aggregation calculation outputs for review and validation?

Pricing models and total cost of ownership

IFRS 17 platform pricing typically follows one of three models: per-user licensing, portfolio-volume tiers, or annual subscription with a base and overage structure. Ask vendors for a three-year total cost of ownership including implementation, training, support, and upgrade fees. Some vendors in the GCC and broader MENA region offer localized pricing that accounts for regulatory reporting calendars.

Support, updates, and long-term viability

Check the vendor’s update cadence. IFRS 17 interpretations continue to evolve, and your platform needs to keep pace. Ask about their IASB monitoring process, how quickly regulatory updates get pushed to production, and what your contractual SLA is for critical calculation fixes.

FAQs: IFRS 17 Vendor Selection

What is the best IFRS 17 solution for non-life insurers?

The best solution handles all three measurement models natively, supports high-volume non-life data without performance degradation, and produces fully auditable disclosure outputs. Platforms with dedicated non-life modules, including intermediate results tables and rules engines for contract recognition, consistently outperform general-purpose accounting systems adapted for IFRS 17.

How do you ensure scalability in IFRS 17 systems?

Scalability depends on three things: parallel processing architecture, automated data transformation pipelines, and cloud-ready deployment. Run a proof-of-concept with your actual portfolio data at peak volumes before signing. Ask the vendor specifically about their largest non-life client by policy count and request a performance benchmark.

What are the biggest vendor risks to avoid?

Watch for vendors who rely on manual steps between data ingestion and final output. That’s a sign the calculation engine isn’t fully integrated. Also flag vendors who can’t demonstrate non-life specific traceability, who give vague answers on multi-entity consolidation, or who have no documented process for handling IASB standard updates.

Can one platform support IFRS 17 and IAS 19 valuation?

Yes, and it’s worth asking vendors about this during evaluation. Platforms that support both standards within a shared data environment reduce duplication in actuarial inputs, simplify audit trails, and cut close timelines. Prima Consulting’s advisory team works with insurers who run both standards and can help you structure the requirements before you go to market.

What to Do Before You Sign

You’ve got the checklist. You know the red flags. And you know what a real IFRS 17 end-to-end non-life solution looks like under the hood. The next step is matching that criteria to a vendor who can actually deliver it in your environment.

IFRSTech provides purpose-built IFRS 17 technology for non-life insurers who need scale, traceability, and full audit readiness. If you’re still comparing options or need an independent view of your shortlist, Prima Consulting’s advisory team at primaconsulting.org can run vendor assessments grounded in actuarial and regulatory expertise. Book a call today and bring your vendor criteria with you.