TL;DR

Enterprise banks need more than a feature list when evaluating IFRS 9 ECL software. This checklist gives your procurement team a structured, defensible framework across eight evaluation areas, from functional requirements and PoC design to commercial terms and exit strategy. You’ll learn which vendor red flags signal regulatory risk, why EIR calculation and ecl audit defense capabilities are non-negotiable, and how to score vendors objectively before committing. If your bank is at the final selection stage, this is where to start.

IFRS 9 ECL Software Vendor Selection Checklist for Enterprise Banks

You’re about to commit your bank to a multi-year platform decision. The IFRS 9 ECL software you select will affect audit outcomes, regulatory reporting cycles, and quarterly close timelines for years to come.

The global IFRS 9 Expected Credit Loss modeling platforms market reached USD 2.85 billion in 2024, per DataIntelo. That scale tells you this market is saturated, which means more vendors, more claims, and more risk of choosing wrong.

This checklist gives decision-stage finance and risk teams a structured framework. It covers functional requirements, vendor red flags, PoC design, and contract terms. Use it to compare vendors side by side and make a defensible choice.

IFRS 9 ECL Software Vendor Selection Criteria

Define ECL Modeling and Reporting Requirements

Start by documenting what your bank needs to produce, not what vendors say they can offer. List your portfolio types, reporting currencies, staging logic, and disclosure obligations under IFRS 9.

Your requirements document becomes the basis for every vendor conversation. Without it, demos run on vendor terms, not yours.

Align with IFRS 9 Impairment Framework

The platform must support the three-stage impairment model explicitly. Check that it handles 12-month ECL for Stage 1 and lifetime ECL for Stages 2 and 3 without workarounds.

Ask vendors directly how they calculate Effective Interest Rate across multi-period forecasts. Vague answers here are a red flag, not a sales nuance.

Set Measurable Technical and Risk KPIs

Define KPIs before demos begin. These should include calculation run times, audit trail completeness, EIR accuracy tolerances, and IFRS 9 regulatory reporting output formats.

Vendors who resist custom KPIs during procurement often resist them during implementation too. That pattern compounds into audit risk.

How to Build a Defensible Evaluation Framework

Start with Outcomes, Not Features

Your bank needs to produce compliant disclosures, pass internal and external audits, and close the quarter faster. Start your evaluation by asking how each vendor gets you there, not which features they list.

Feature-led demos tend to favor vendors with polished UX over vendors with stronger compliance architecture.

Identify Regulatory Non-Negotiables

Certain capabilities are not optional for enterprise ECL platforms. Immutable audit trails, full drill-down from portfolio ECL to facility-level cash flows, and traceable staging decisions are baseline requirements.

A 2025 UNEP FI survey found that 36% of banks are incorporating climate risk into IFRS 9 and CECL estimates, per UNEP FI. Your platform needs to support macroeconomic overlays, not just historical PD curves.

Create Weighted Scoring and Comparison Matrix

Assign numerical weights to criteria categories: compliance architecture, integration depth, implementation speed, audit readiness, and support responsiveness.

Weighted scoring removes bias from demos and gives your procurement committee a documented basis for every decision.

Assign Governance and Decision Owners

ECL platform decisions typically involve Finance, Risk, IT, Compliance, and Internal Audit. Each team has distinct concerns and veto points.

Assign a named owner for each evaluation criterion. Without clear ownership, vendor selection stalls or defaults to whoever spoke last in the room.

Core Functional Requirements for ECL Platforms

PD, LGD, and EAD Modeling Capabilities

The platform must support transparent PD, LGD, and EAD calculation at facility level. You need to see every assumption and every intermediate result, not just the final provision number.

Vendors using black-box aggregation create audit exposure. Regulators and external auditors expect traceability to source data.

Scenario Analysis and Macroeconomic Overlays

IFRS 9 requires forward-looking information. Your platform should support base, optimistic, and pessimistic macroeconomic scenarios with probability-weighted ECL outputs.

Check that the scenario framework handles GDP, unemployment, interest rate, and property price inputs. Single-factor sensitivity models are not sufficient for most regulators.

Data Integration and Automation Controls

Batch file processing creates data latency and version control gaps. API-native integration with your core banking system eliminates overnight delays and manual upload errors.

Check for hidden audit risks in IFRS 9 spreadsheets before assuming your current data flows are compatible with a new platform.

Audit Trails and Regulatory Reporting Outputs

Every parameter change, staging override, and model update must be logged with timestamps, user IDs, and change rationale. This is non-negotiable for ecl audit defense.

The platform should generate IFRS 7 disclosure templates automatically, including ECL movement reconciliations and credit risk concentration tables.

Technical and IT Due Diligence Checklist

System Architecture and Scalability

Ask vendors how calculation time changes as your loan book grows. Platforms that process slowly at current scale create capacity risk during peak periods.

Multi-entity support is a separate requirement for banking groups. Confirm the platform handles multiple legal entities, currencies, and reporting perimeters without manual aggregation.

Cloud vs On-Premise Deployment Options

Some regulators impose data residency requirements. Some banks have group-level IT policies that restrict cloud deployment. Get this answer confirmed in writing, not just in a demo.

The build vs buy IFRS 9 software TCO analysis for your specific deployment model should inform your total cost estimate before you commit.

Security, Access Controls, and Compliance

Role-based access controls should restrict who can modify models, override parameters, or view sensitive credit data. Multi-factor authentication and immutable audit logs are baseline expectations.

Ask for SOC 2 Type II certification documentation and review it. Many vendors claim security compliance without third-party validation.

Integration with Core Banking Systems

Confirm direct API connectivity to your core banking system, general ledger, and data warehouse. Manual CSV exports between systems create reconciliation gaps and increase closing cycle time.

Platforms built on file-based data exchange were designed before modern banking API standards. They tend to accumulate technical debt that your IT team inherits.

Proof of Concept and Vendor Demonstrations

Designing an Effective ECL PoC

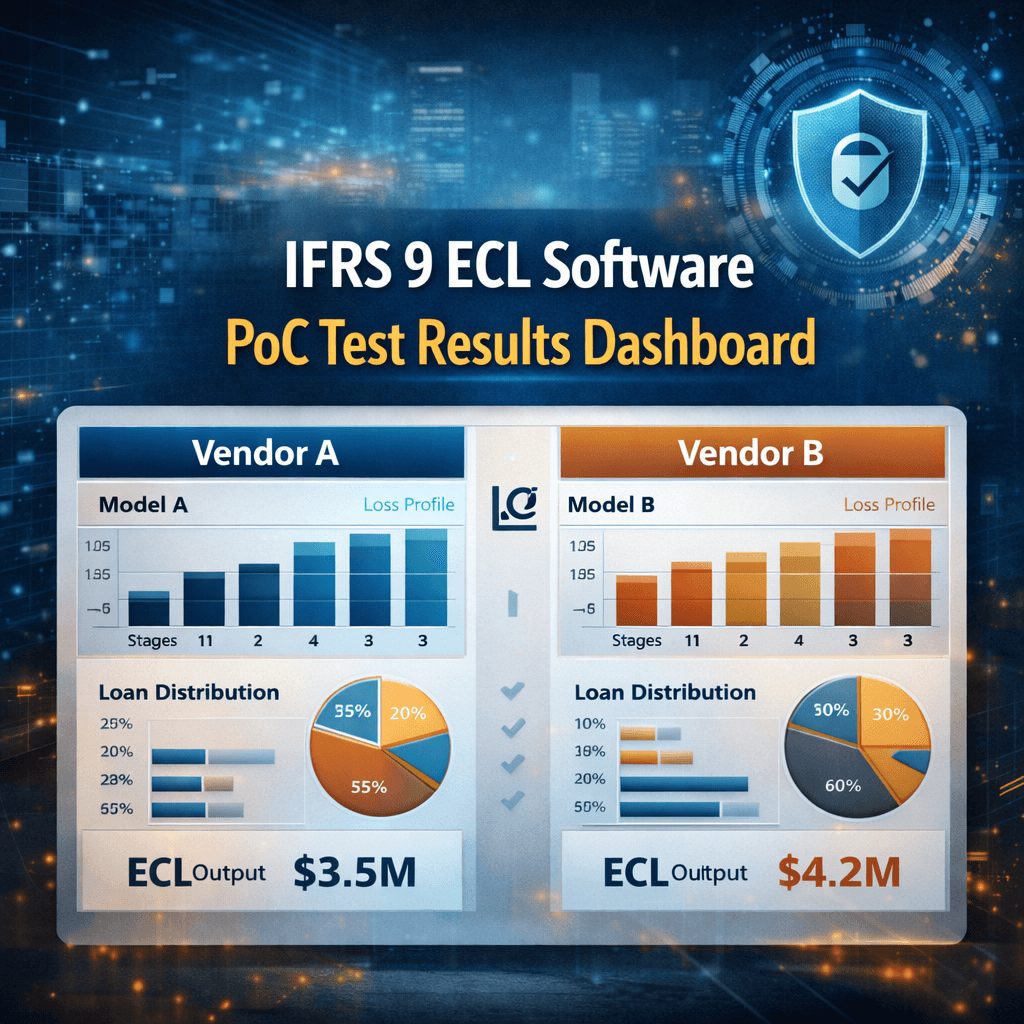

Run your PoC on real data, not vendor-supplied sample files. Provide a representative slice of your actual loan book, including edge cases like restructured facilities, purchased credit-impaired assets, and revolving commitments.

Define pass-fail criteria in advance. A PoC without agreed success criteria defaults to a second demo with your data.

Validating Model Accuracy and Performance

Compare PoC ECL outputs to your current calculations. Material differences need explanations, not reassurances. Ask vendors to walk through their methodology at facility level.

Test calculation run time against your full portfolio volume, not a subset. Performance issues discovered post-implementation are expensive to resolve.

Testing Reporting and Disclosure Outputs

Export the IFRS 7 disclosure package from the PoC environment and review it against your current reporting templates. Gaps identified here predict gaps during your first live quarter.

Your internal audit team should review PoC outputs before selection is finalized. Their sign-off on the audit trail quality reduces post-implementation friction.

Commercial, Risk, and Contract Considerations

Total Cost of Ownership Analysis

License fees are the starting point, not the full picture. Add implementation costs, internal resource time, data migration effort, ongoing support fees, and annual model update costs.

A platform priced low at entry often carries high customization and support costs once you’re inside. Review the IFRS 9 compliance process architecture implications before comparing sticker prices.

Implementation Timeline and Resource Plan

Ask vendors for a realistic implementation timeline based on your specific configuration needs, not a best-case scenario. Implementations that run longer than planned create regulatory exposure if they coincide with reporting dates.

Standard implementations for purpose-built ECL platforms typically complete in 6 to 12 weeks. Legacy multi-module suites often require 6 to 12 months. The gap in timeline is also a gap in cost.

Ongoing Support and Model Updates

IFRS 9 guidance evolves. Your vendor needs to update models and templates when regulatory interpretations change. Confirm that regulatory updates are included in your support contract, not billed separately.

Ask for the vendor’s documented response time for critical issues. Four hours or less for system-down events is a reasonable baseline for enterprise IFRS 9 software.

Exit Strategy and Data Portability

Document how you get your data out if you switch vendors. Proprietary data formats that require vendor assistance to export create dependency risk.

Standard export formats and open API access to your own calculation results are contractual rights worth negotiating before you sign.

Common Pitfalls in ECL Software Selection

Overlooking Data Quality Constraints

Many ECL implementations fail not because the software is wrong, but because source data quality is insufficient. Gaps in facility-level data, missing collateral valuations, and inconsistent staging history all create downstream modeling errors.

Run a data quality assessment before vendor selection, not after contract signing. Your IFRS 9 impairment spreadsheet risk profile should inform your integration design.

Ignoring Change Management Needs

Finance and risk teams replacing manual ECL spreadsheets often underestimate the retraining required. New platforms change how people interact with data, not just where they find it.

Budget for user training as a line item, not a free add-on. Platforms that promise training without a structured plan tend to deliver documentation, not capability.

Selecting Tools Without Regulatory Alignment

Generic risk software is not the same as IFRS 9-specific ECL software. ERM platforms built for broad risk management may not support EIR calculation, SICR detection, or IFRS 7 disclosure generation natively.

Vendor red flags ifrs ecl include: no native audit trail, EIR calculated outside the platform, and disclosure templates that require manual editing after export. These are not minor gaps. They create direct audit exposure.

Why Rust IFRS 9 Software Stands Out for Enterprise ECL

For enterprise banks and financial institutions evaluating scalable multi-entity ECL vendors, Rust IFRS 9 Software delivers a purpose-built ECL engine with API-native integration and full calculation transparency.

Rust connects directly to Temenos, Flexcube, Finacle, SAP, and Oracle through REST APIs, eliminating batch file exchanges. Every staging decision, PD curve, and ECL output is drill-down-auditable to facility level.

Implementation completes in 6 to 8 weeks through prebuilt staging rules, PD term structure templates, and IFRS 7 disclosure generators. A regional bank with USD 8 billion in assets reduced its IFRS 9 close cycle from 12 days to 4 days after deploying Rust.

For enterprise ECL software criteria banks need to meet, Rust provides SOC 2 Type II security certification, multi-entity support, cloud and on-premise deployment options, and immutable audit trail logging that satisfies both internal audit and external regulators.

[Schedule a personalized demo at IFRSTech.com to see Rust handle your specific ECL requirements.]

FAQs on Enterprise ECL Vendor Selection

What Makes IFRS 9 ECL Software Compliant?

Compliant IFRS 9 ECL software supports three-stage impairment classification, 12-month and lifetime ECL calculations, EIR-based discounting, forward-looking macroeconomic overlays, IFRS 7 disclosure generation, and complete audit trails. The platform must trace every provision amount back to source facility data without manual intervention.

How Long Does ECL System Implementation Take?

Purpose-built ECL platforms typically deploy in 6 to 12 weeks with prebuilt templates and API integration. Multi-module enterprise suites often require 6 to 12 months. Your implementation timeline depends on data migration complexity, integration scope, and configuration requirements. Confirm the timeline in writing before signing any contract.

What Criteria Matter Most for Banks?

Enterprise ECL software criteria banks prioritize most include audit trail completeness, EIR calculation accuracy, API integration with core banking systems, multi-entity support, scenario analysis capabilities, and implementation speed. Regulatory defensibility of outputs matters more than feature breadth for most compliance teams.

How Do You Compare Multiple ECL Vendors Objectively?

Build a weighted scoring matrix before any demos. Assign weights to compliance architecture, integration depth, audit readiness, implementation timeline, total cost of ownership, and support responsiveness. Run a structured PoC on your own data and score each vendor against pre-agreed pass-fail criteria. Document every decision for governance purposes.

Ready to Evaluate IFRS 9 ECL Software with Expert Guidance?

Choosing the right ECL platform is one of the highest-stakes decisions your finance and risk team will make. The criteria in this checklist give you a structured starting point, but implementation success also depends on regulatory interpretation, model governance, and change management.

Prima Consulting’s IFRS 9 advisory services combine technical ECL expertise with regulatory experience across banking and financial services markets worldwide.

To see a platform purpose-built for enterprise ECL requirements, schedule a demo of Rust IFRS 9 Software at IFRSTech.com. Your first call is a no-obligation consultation.