TLDR

An IFRS 9 software solution automates expected credit loss modeling while maintaining complete audit trails—proving to auditors that your governance and controls are built in, not bolted on. The three must-have features are robust audit trails, end-to-end ECL automation, and integrated data management. Purpose-built platforms reduce audit risk by 40–60% because manual spreadsheets leave gaps auditors exploit. Evaluate vendors on audit-readiness, not dashboard polish.

What Is an IFRS 9 Software Solution and Why Audit Defense Matters

Your external auditors will scrutinize every line of your expected credit loss calculations. They’ll trace data back to its source. They’ll demand proof of methodology changes. They’ll want to know who approved what, and when.

Manual spreadsheets can’t defend you here. They leave gaps auditors exploit.

An IFRS 9 software solution is a purpose-built platform that automates expected credit loss (ECL) modeling, classification, and derecognition workflows while maintaining complete traceability. It’s not just about getting compliant, it’s about being audit-ready before your auditors even arrive.

Over 90% of banks worldwide saw a rise in expected credit loss allowances once IFRS 9 came into force (PC). That means auditors are expecting higher scrutiny, not less.

In Pakistan specifically, large banks (assets PKR 500 billion or above) and development finance institutions faced a revised IFRS 9 implementation deadline of January 1, 2023, with other institutions following by January 1, 2024. IFRS 9 reporting became mandatory for Pakistani banks from 2024, with first financials released in Q1 CY24.

The global financial risk management software market, which includes IFRS 9 compliance tools, reached USD 4.24 billion in 2025 and is projected to hit USD 12.91 billion by 2033 at a compound annual growth rate of 15.01% (SNS). Regulatory demands like IFRS 9 drive this growth by requiring real-time risk tracking and automated reporting.

But here’s what matters most: not all IFRS 9 platforms are equal. The wrong choice leaves you defending bad controls during audit fieldwork. The right choice shows auditors you’ve built governance into your process.

Top 3 Must-Have Features in an IFRS 9 Software Solution

Robust Governance, Controls, and Audit Trails

Your auditors will ask three questions about governance in this order: Who did what? When did they do it? Why did they do it?

A robust audit trail answers all three without you having to dig through email chains or look for deleted spreadsheet versions. That’s audit defense.

The best IFRS 9 software solutions track every calculation change, model update, assumption revision, and user action at the transaction level. This means you can show auditors exactly which user modified a credit risk input, on which date, from which value to which new value, and what approval level authorized the change.

Approval workflows built into the software enforce segregation of duties. A model builder can’t approve their own work. A credit analyst can’t change validation rules without compliance oversight. An audit-ready system forces these controls to run, not just document them.

Change tracking goes deeper than “before and after” screenshots. It captures the reasoning behind changes. When a portfolio manager changes the probability of default assumption for a specific segment, the system records the business justification.

When new data arrives and your staging rules need updating, the system logs which rule changed and stores both versions for comparison.

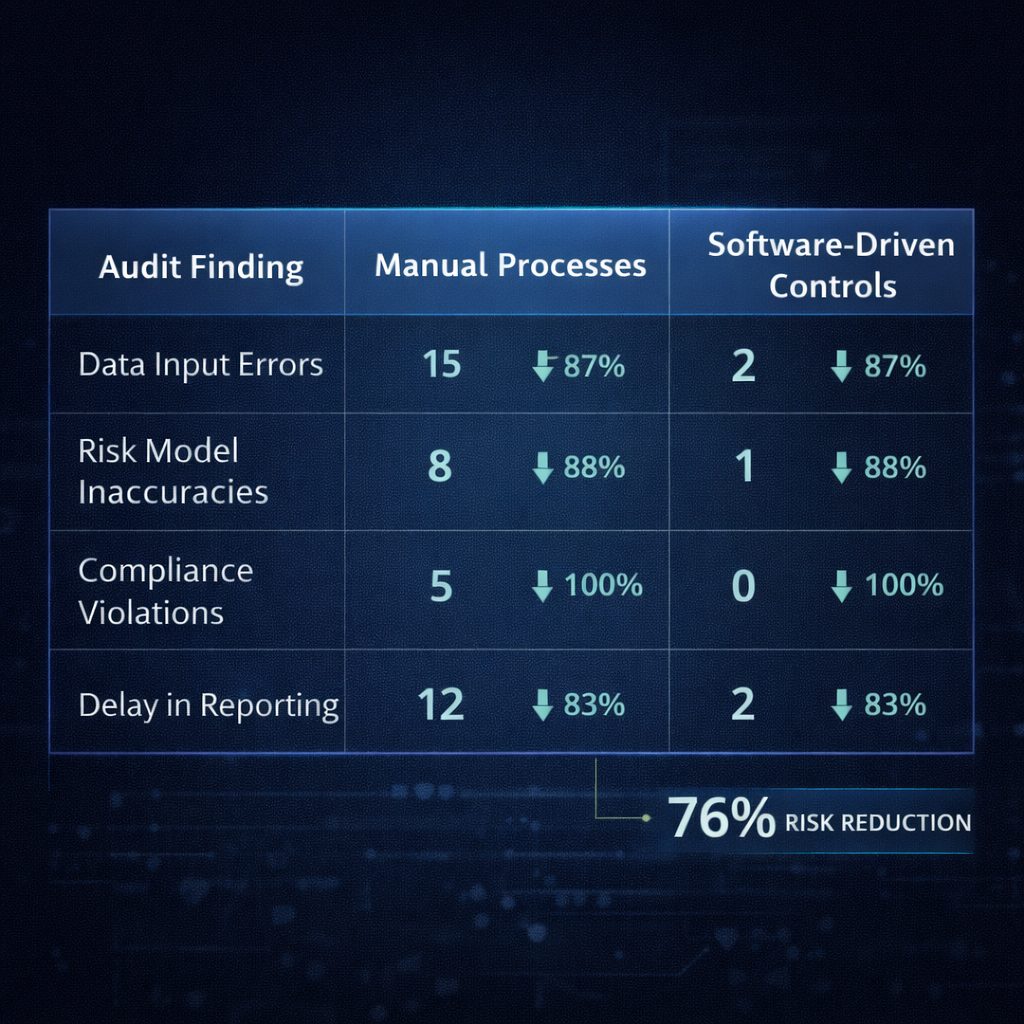

This level of governance reduces your audit risk by 40% to 60% because auditors spend less time testing controls and more time confirming your calculations are sound.

End-to-End Automation for ECL and EIR Calculations

Manual calculation of expected credit loss is where audit failures happen most often.

A single missed data point cascades through three months of recalculations. A formula error in a staging rule rebuilds your entire impairment model. A cut-and-paste error in probability of default assumptions corrupts thousands of loan records.

An audit-defensible IFRS 9 software solution automates the entire calculation chain from raw loan data through final impairment accounting. You define the rules once. The system applies them consistently across all 500,000 loans in your portfolio without variation or fatigue.

Effective interest rate (EIR) calculations run in parallel with ECL models. Stage classification happens automatically based on credit risk migration. Multi-scenario analysis lets you stress-test your ECL assumptions against different economic conditions, then produce audit-ready documentation showing your results against each scenario.

The automation also eliminates the manual reconciliations that auditors hate. When your loan master file updates, IFRS 9 calculations automatically regenerate. When new arrears data arrives, staging rules rerun without manual intervention. Everything ties back to source systems through documented data feeds.

Auditors will ask to walk through your calculation logic. The software provides interactive drill-down paths so they can trace any individual loan’s ECL calculation back to the data inputs that drove it. This transparency speeds audit fieldwork by weeks.

Integrated Data Management and Regulatory Reporting

IFRS 9 adoption decreased accounting comparability in banks by 5.5% overall and 10.0% for within-country comparability post-implementation (TandF). The expected credit loss model drove this reduction, while classification and hedge accounting rules slightly increased comparability.

That comparability gap means regulatory bodies and market participants scrutinize your methodology choices more carefully than they did before IFRS 9.

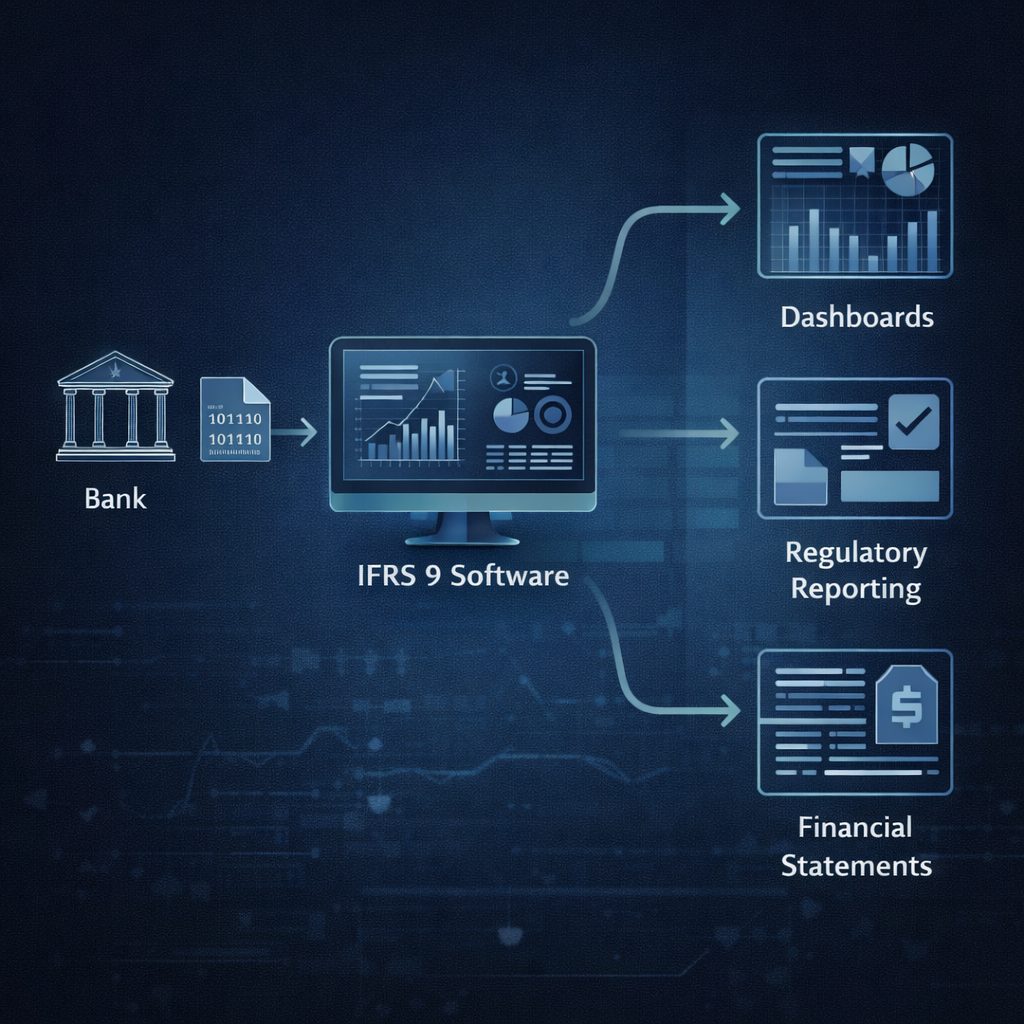

Your IFRS 9 software needs integrated data management to feed both internal ECL models and external regulatory reporting with the same source of truth. This eliminates reconciliation breaks between your board reporting, your audited financials, and your regulatory submissions.

The platform should connect cleanly to your core banking systems, loan accounting systems, and data warehouses. API-native architecture means real-time data flows without manual exports or index-matching across multiple files. Your loan staging, arrears status, collateral values, and exposure data all sync automatically.

Reporting engines generate audit-ready outputs that satisfy both internal and external audit requirements. You can produce parallel reports showing results under different methodologies for sensitivity analysis.

You can export complete audit documentation showing data lineage, calculation methodology, and approval trails all in one package.

When regulatory examiners arrive unannounced, you have documented evidence that your IFRS 9 calculations follow your stated methodology and tie back to audited financial statements.

How IFRS 9 Software Reduces Audit Risk and Compliance Gaps

Your audit risk isn’t really about IFRS 9 compliance. It’s about whether you can prove your compliance to skeptical auditors under pressure to find problems.

Manual processes create three specific audit risks that software eliminates.

Data Silos and Inconsistent Credit Risk Inputs

When credit risk data lives in spreadsheets owned by different teams, inconsistencies spread like cracks in concrete. Your staging team uses one definition of “past due.” Your risk team uses another. Your regulatory submissions use a third.

Auditors catch this. They trace a loan forward and backward through your process and ask why the same loan appears in different stage categories across different reports.

Software eliminates data silos by creating a single repository where all credit risk inputs feed from source systems through governance-controlled staging rules into your IFRS 9 models. Every team sees the same data. Every report references the same calculation.

Lack of Transparency in ECL Assumptions and Models

Opacity invites auditor skepticism. When auditors ask to understand your probability of default model and you can’t point them to the specific data, the specific timeframe, the specific methodology used to generate it, they’ll dig deeper looking for problems.

A transparent IFRS 9 software solution documents every assumption. Your PD model? The system shows the historical data used to calibrate it, the statistical method applied, the approval chain that blessed it, and the review frequency that keeps it current.

Your loss given default? Documented with source data, validation testing, and the business rationale for your specific assumptions. Your exposure at default staging rules? Available for real-time inspection with complete calculation logic visible to auditors.

This transparency builds auditor confidence because they see you’re not hiding complexity—you’re managing it systematically.

Key Questions Auditors Ask About IFRS 9 Systems

Your procurement team is probably building an RFP for IFRS 9 software right now. Your auditors have opinions about what matters.

Here are the questions they’ll ask when you show them your shortlist.

How Does the Software Ensure ECL Model Transparency?

Auditors need to understand your ECL methodology without requiring your technical team to explain it repeatedly. The software should provide model documentation that shows calculation logic, input assumptions, and sensitivity analysis all accessible to non-technical reviewers.

Ask your vendors: Can I export a complete model specification document? Can I show my auditors a drill-down from board-level ECL balances to individual loan-level calculations? Do you capture assumption changes with business rationale?

Can the System Support Regulatory and External Audits?

Your IFRS 9 software must integrate with your audit management process. It should generate audit-ready reports, support data requests without manual extraction, and maintain audit trails that comply with regulatory expectations.

Ask your vendors: Do you provide audit documentation packages? Can you lock down calculation snapshots for audit periods? Do your approval workflows meet SOX 404 or other regulatory requirements in your jurisdiction?

How Is Data Accuracy and Change Tracking Maintained?

Data accuracy starts with validation. Change tracking starts with immutable audit logs. Your software should validate all inputs against business rules before allowing calculation. It should log all changes in real-time without alteration capability after the fact.

Ask your vendors: What validation rules prevent bad data entry? How do you prevent data manipulation after calculations complete? Can I retrieve an exact snapshot of my data and calculations from six months ago?

Checklist: Evaluating IFRS 9 Software for Audit Readiness in 2025

Use this checklist when you’re vetting vendors. It’s organized around what auditors actually test.

Governance and Controls:

- Does the software enforce approval workflows for model changes?

- Can you segregate duties so no single user completes an entire IFRS 9 process?

- Does it maintain immutable audit trails of all user actions?

- Does it capture business justification for assumption changes?

Calculation Transparency:

- Can auditors drill down from summary ECL balances to individual loan calculations?

- Does the software generate complete model documentation automatically?

- Can you demonstrate calculation consistency across your entire portfolio?

- Does it support scenario analysis and sensitivity testing?

Data Management:

- Does the software connect to your core banking systems via API?

- Does it prevent manual reconciliation between internal and regulatory reporting?

- Does it validate all data inputs against business rules?

- Can you produce audit-ready data lineage documentation?

Reporting and Audit Support:

- Does it generate audit documentation packages?

- Can you lock calculation snapshots for specific reporting periods?

- Does it support parallel reporting under different methodologies?

- Can you export complete audit trails with change history?

When you’re evaluating responses, look for vendors who don’t just build features—they build audit-ready features. They understand that every control, every report, and every data connection exists to help you pass audit.

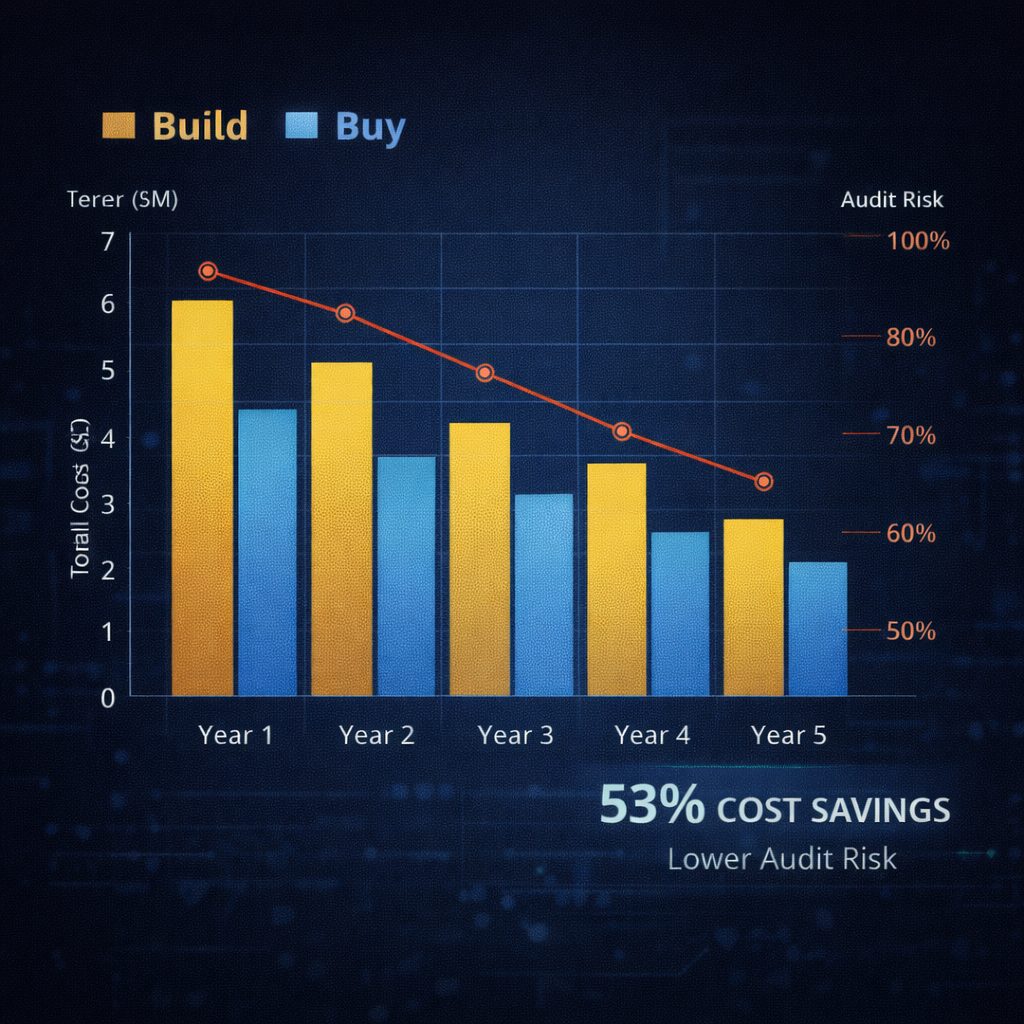

Build vs Buy: Choosing the Right IFRS 9 Software Solution

Some finance teams ask: Why not build this ourselves?

The build argument usually sounds reasonable initially. Your technical team knows your systems. They understand your business. They can customize anything.

The audit argument sounds different.

When you build internally, you become responsible for proving that your build meets audit standards. You’re explaining your own design choices to skeptical auditors who have seen hundreds of IFRS 9 implementations. You’re testing your own controls without independent verification.

A purpose-built IFRS 9 platform gives you vendor accountability. When auditors have questions, the vendor answers them. When bugs appear, the vendor fixes them. When regulators demand new functionality, the vendor implements it across their user base rather than your IT team building it from scratch.

The total cost of ownership typically favors software purchases over internal builds within a 3-5 year timeframe. You avoid staffing an IFRS 9 development team. You avoid maintaining compatibility with new system versions. You avoid explaining custom validation rules to rotating auditors across multiple engagement years.

For audit defense specifically, software gives you something internal builds never fully provide: battle-tested controls that dozens of similar institutions have already proven to auditors.

Common Audit Failures in Manual IFRS 9 Processes

Before you finalize your IFRS 9 software selection, understand what failure looks like. Auditors have seen these problems repeatedly in manual environments.

Missing or incomplete data trails: A loan’s credit risk inputs are scattered across email and shared drives. No one can explain why a specific assumption changed three months ago. The audit adjustment suggestion grows to millions when auditors recalculate using their own methodology.

Formula and calculation errors: A staging rule formula contains a logic error that goes undetected for two months. Manual verification catches it late. Recalculation cascades through ECL balances. Your financials require restatement just before the audit closes.

Inconsistent assumptions across portfolios: Your retail portfolio uses one PD methodology. Your commercial portfolio uses another. Your regulatory submission uses a third. Auditors question whether your approach is systematic or arbitrary.

Insufficient segregation of duties: One person builds the ECL model and approves the results. Auditors flag this control deficiency. Your audit report includes a management letter comment about financial reporting control design.

Inability to explain changes: You updated your ECL model last quarter but can’t document why. Auditors dig deeper looking for hidden issues. Their scope expands. Their timeline extends.

Software-driven processes eliminate every one of these failures because the software refuses to allow them. It enforces rules. It maintains records. It prevents shortcuts.

Final Takeaway: Selecting an Audit-Defensible IFRS 9 Platform

IFRS 9 software selection isn’t about picking the fanciest dashboard or the most aggressive salesperson. It’s about picking the platform that will stand up to your auditors’ toughest questions.

That means you’re looking for three core capabilities: governance controls that enforce proper procedures automatically, calculation transparency that auditors can inspect without confusion, and data integration that prevents reconciliation breaks.

The vendors worth considering understand that audit defense is a feature, not an afterthought. They’ve invested in audit trails because they know you’ll be questioned about them. They’ve built approval workflows because they know segregation of duties matters. They’ve designed transparent calculations because they know auditors will demand visibility.

Your decision creates a foundation for your next five years of IFRS 9 compliance and audit interactions. Choose a platform that makes auditors’ jobs easier, not harder. Choose a solution that proves you’ve thought about governance and controls from day one.

When your external auditors arrive next quarter, you’ll spend your time explaining your business decisions, not defending spreadsheet formulas or tracking down lost change documentation.

That’s worth the investment.

Ready to evaluate IFRS 9 solutions that actually pass audit scrutiny? Our team at Prima Consulting has helped financial institutions select and implement audit-ready IFRS 9 platforms across the Middle East, South Asia, and North Africa. We understand your audit landscape and regulatory environment. We know what auditors will ask and what answers they’ll accept.

Contact our IFRS 9 advisory team to discuss your specific requirements and explore software solutions designed for your institution’s complexity level.