TL;DR

IFRS 17 software platforms solve critical data challenges that delay insurance compliance. IFRS 17 data requirements demand contract-level tracking across actuarial, finance, and policy systems with millions of granular data points. Legacy spreadsheet processes can’t handle the volume or complexity, creating reconciliation gaps and audit trail failures. Purpose-built IFRS 17 software automates data flows, eliminates manual errors, and connects disparate sources into unified repositories. Automated platforms handle GMM, PAA, and VFA calculations while preserving complete audit trails and governance controls. Read on to discover how proper data architecture and automation ensure successful IFRS 17 implementation.

IFRS 17 Data Requirements: Why IFRS 17 Software Matters

You’re staring at spreadsheets that never reconcile. Your actuarial team uses one model while finance relies on another. Claims data sits in a different system entirely.

That’s the reality for most insurers facing IFRS 17 data requirements. The standard demands contract-level detail that your legacy systems simply can’t provide. IFRS 17 software exists to bridge these gaps, but understanding your data challenges comes first.

What data does IFRS 17 require from insurers?

IFRS 17 shifts insurance reporting from aggregate portfolios to individual contract tracking. You’ll need detailed records for every policy’s cash flows, premiums, claims, and adjustments.

The standard requires three measurement models based on contract characteristics. Each model carries distinct data demands that stretch existing infrastructure.

Contract-level vs portfolio-level data requirements

Under IFRS 4, you tracked liabilities at portfolio level. IFRS 17 changes that completely.

Now you’re tracking individual contracts within cohorts. Each contract needs its own cash flow projections, premium allocations, and coverage period details.

This means storing millions of data points instead of thousands. Your database architecture must handle 100 times more granular information than before.

The shift affects every downstream process. Reconciliations take longer, reporting cycles strain infrastructure, and audit trails become exponentially complex.

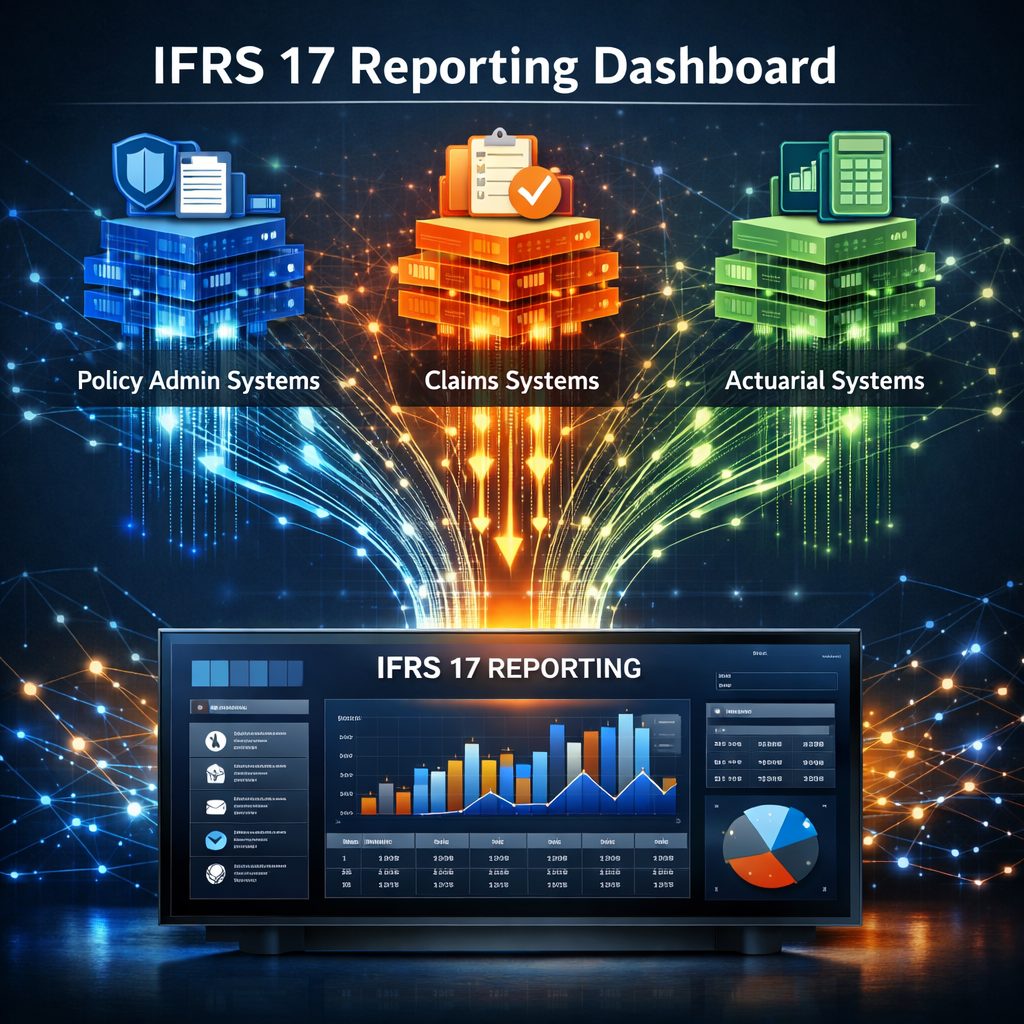

Actuarial, finance, and policy data alignment

Your actuarial models calculate reserves using assumptions about policyholder behavior. Finance needs those same contracts valued in general ledger terms.

Policy administration systems track premiums received and coverage details. Claims systems hold loss histories and settlement patterns.

IFRS 17 demands all four sources speak the same language. Yet most insurers find their systems use different contract identifiers, date formats, and classification schemes.

Data from actuarial spreadsheets won’t match finance records. Premium amounts in policy systems differ from what accounting teams report.

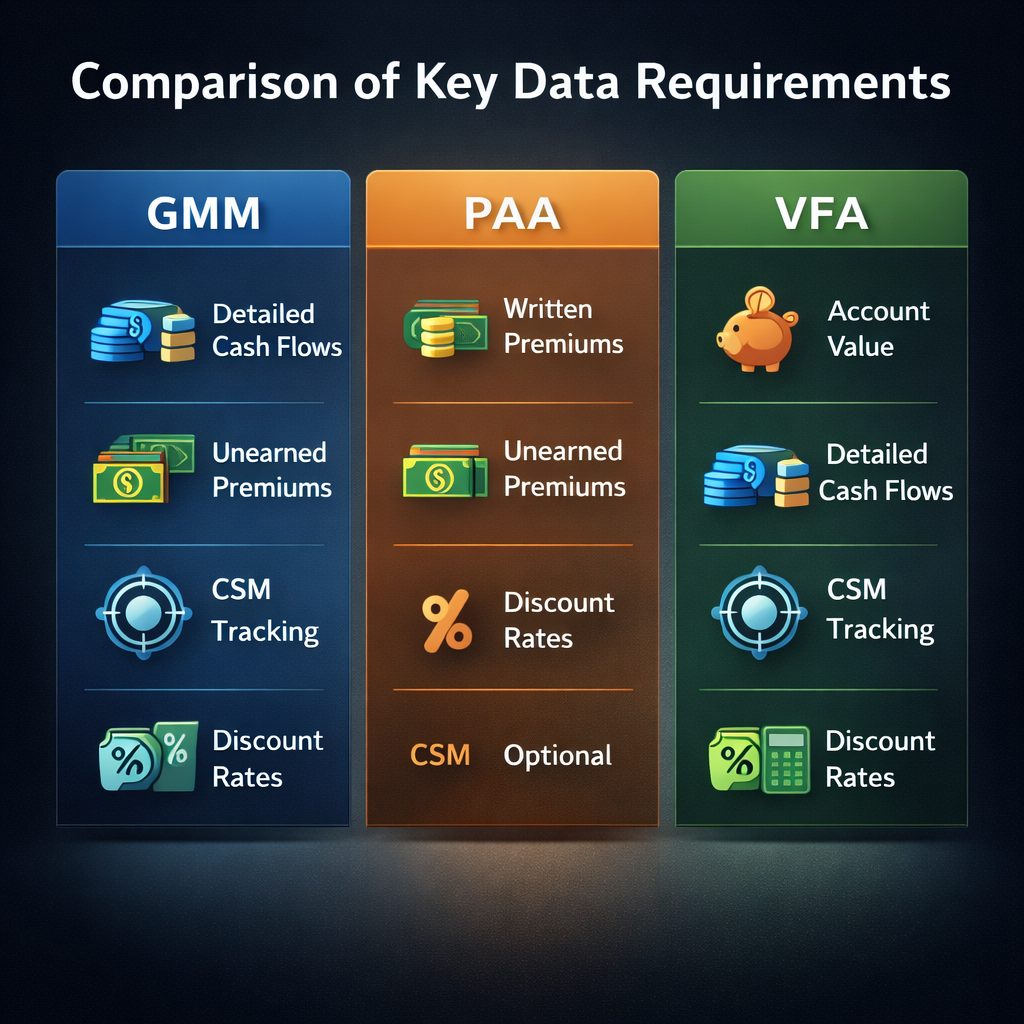

Data granularity required for GMM, PAA, and VFA

The General Measurement Model (GMM) requires tracking the Contractual Service Margin (CSM) for every contract group. You’ll need historical cash flows, current estimates, and assumption changes documented separately.

Premium Allocation Approach (PAA) appears simpler but still demands proof. Roughly 90% of non-life insurance liabilities were valued using PAA in recent implementations.

Even with PAA, you’re running parallel GMM calculations to demonstrate materiality thresholds. That means maintaining two complete data sets for comparison purposes.

Variable Fee Approach (VFA) adds another layer. You’re tracking policyholder shares in underlying items, requiring real-time investment data linked to specific contracts.

Why IFRS 17 data requirements delay implementation

You’re not alone if IFRS 17 rollout took longer than planned. Data issues account for most implementation delays across the insurance industry.

Legacy systems weren’t built for this level of detail. What worked for decades under IFRS 4 now creates bottlenecks.

Historical data challenges in IFRS 17

IFRS 17 requires transition data going back to contract inception. For long-duration policies, that means retrieving records from 20 or 30 years ago.

Many insurers archived older data in formats no longer accessible. Tape backups, discontinued software, and merged systems all create gaps.

You might find premium information but lack corresponding cash flow details. Claims exist without clear linkage to original policy terms.

62% of New Zealand insurers repo

rted no onerous contracts in their first filings. That statistic masks the data quality struggles behind those clean results.

Reconstructing missing information takes months. You’re manually reviewing paper files or making reasonable approximations where exact data doesn’t exist.

Data governance and audit trail expectations

Regulators expect complete documentation of every assumption, adjustment, and calculation. Your audit trail must show who changed what data and when.

That level of tracking doesn’t exist in most spreadsheet-based processes. Finance teams share files via email with version control handled manually.

IFRS 17 demands automated controls. Changes to discount rates need approval workflows, assumption updates require documentation, and every CSM adjustment must trace to source.

Building governance frameworks means redesigning processes that worked for years. Teams resist changing familiar workflows even when compliance requires it.

How IFRS 17 software fixes data gaps

Technology solutions address what manual processes can’t handle. Purpose-built platforms connect disparate sources and automate reconciliation.

You’re replacing spreadsheets with centralized repositories. Data flows from source systems into unified structures designed for IFRS 17 calculations.

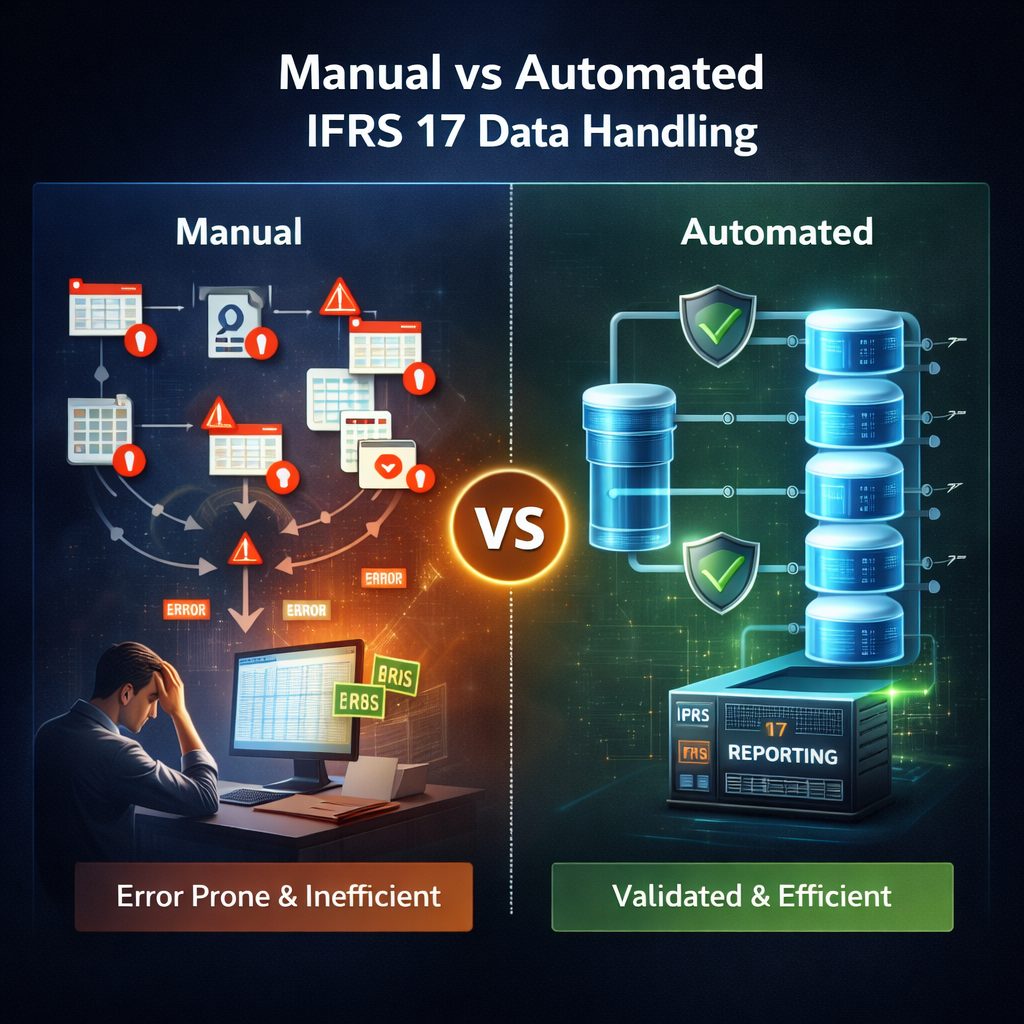

Automation vs manual data handling risks

Manual processes fail under IFRS 17’s volume demands. Copying data between systems introduces errors that compound through calculations.

One misplaced decimal in a discount rate affects thousands of contracts. Timing differences between when actuarial runs occur and when finance closes books create permanent reconciliation gaps.

Automated IFRS 17 software eliminates copy-paste errors. Data extracts from source systems on defined schedules with validation rules catching exceptions immediately.

You’ll still review results, but the software handles repetitive tasks. That frees your team to focus on judgment calls and exception handling.

86% of over 60 surveyed Asian P&C insurers applied PAA only during initial adoption. Automation made that choice viable by simplifying eligibility testing.

Key data challenges in IFRS 17 implementation

Every insurer faces similar obstacles regardless of size or market. Understanding common challenges helps you plan realistic timelines.

Data quality issues surface during implementation that weren’t apparent under old standards. What seemed acceptable for IFRS 4 fails IFRS 17’s scrutiny.

Common data quality issues under IFRS 17

Contract boundaries prove harder to define than expected. Your policy systems don’t clearly distinguish when coverage ends or when renewal options create new contracts.

Premium data exists at transaction level but lacks allocation to coverage periods. You know total premiums collected but can’t break them down by month or quarter.

Claims data shows settlement amounts without detailed cash flow timing. IFRS 17 needs payment patterns split by incurred date, not just paid date.

Reinsurance recoveries sit in separate systems with different contract identifiers. Matching ceded premiums to underlying policies requires manual mapping.

Discount rate applications vary by product line. Some teams use risk-free rates while others include illiquidity premiums without consistent methodology.

Examples of IFRS 17 data mapping issues

Product codes in policy administration don’t match general ledger account structures. Finance aggregates by business segment while operations track by product version.

Date fields store inception dates differently across systems. Some use policy effective date, others use accounting recognition date, creating timing mismatches.

Currency handling varies between actuarial models and accounting systems. Foreign exchange translations apply at different points in the calculation chain.

Contract modifications update policy systems but don’t trigger recalculation in actuarial models. Your CSM doesn’t reflect mid-term endorsements automatically.

What data models work best for IFRS 17 compliance?

Your data architecture determines whether reporting succeeds or fails. The right structure supports calculations while wrong design creates ongoing struggles.

Most insurers underestimate the modeling effort required. You’re not just storing data but creating relationships that enable complex calculations.

How insurers should structure IFRS 17 data architecture

Start with contract as your base entity. Every data element must link to specific contracts within defined groups.

Cash flow tables store expected and actual amounts by coverage period. Each row connects to contract IDs with timestamps for version control.

Assumption tables hold discount curves, mortality rates, and lapse expectations. Changes create new versions without overwriting historical values.

Calculation tables preserve every step from gross premiums through CSM adjustments to final liability amounts. Audit trails show complete calculation chains.

Reference tables map between different system identifiers. Product codes, account numbers, and organizational units all need translation layers.

The architecture must support temporal queries. You’re answering “what was the CSM for this contract group at quarter end” repeatedly throughout the year.

Checklist for IFRS 17 data readiness

Before implementation, verify these foundational elements exist:

- Complete contract inventory with unique identifiers across all systems

- Historical premium and claims data for transition calculations

- Cash flow projections at contract level with timing details

- Documented discount rate methodologies with rate curve sources

- Contract grouping logic that supports onerous testing

- Reinsurance linkages showing ceded portions by underlying contract

- Assumption change tracking with approval workflows

- Reconciliation between actuarial reserves and general ledger balances

Missing any item means your data isn’t ready. Implementation will stall when calculations can’t run or results don’t reconcile.

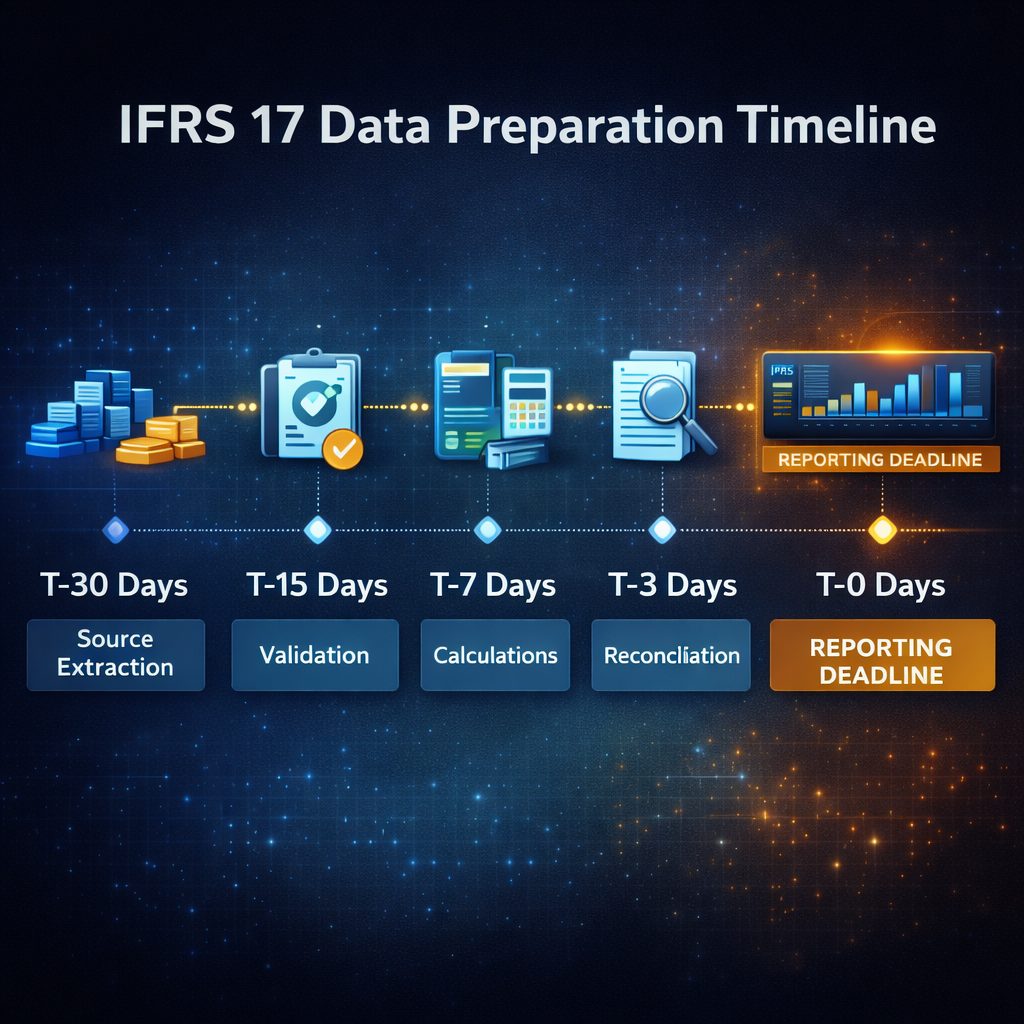

How to prepare data for IFRS 17 reporting

Preparation determines whether quarterly closes take days or weeks. You’re building processes that repeat under tight deadlines.

Start early and test repeatedly. Data issues that seem minor during planning become critical during first live reporting.

Extract source data with enough lead time for validation. You’ll find exceptions that need research before calculations begin.

Map contracts to cohorts using documented rules. Judgment calls need approval before processing starts, not during close.

Run calculations in stages with checkpoints between. Validate cash flows before computing CSM, verify CSM before releasing liabilities.

Compare results against prior periods and expectations. Material variances need explanation before external reporting occurs.

Document everything as you go. Questions will arise during audit that require retracing specific calculations months later.

Questions insurers ask before selecting IFRS 17 software

What source systems will the solution connect to directly versus requiring file uploads?

How does the platform handle contract grouping and cohort assignment?

Can it process both GMM and PAA simultaneously for materiality testing?

Does the solution store calculation history for audit trails?

What happens when you need to restate prior periods due to assumption changes?

How long does month-end close take with your contract volumes?

Can actuarial teams work in the system simultaneously with finance?

What validation rules run automatically before releasing results?

Does it support multiple discount curve scenarios for sensitivity analysis?

How are software updates handled during critical reporting periods?

Frequently Asked Questions

Existing actuarial systems calculate reserves but rarely integrate with general ledger processes. You’ll face reconciliation challenges even if actuarial calculations meet IFRS 17 standards. Most insurers need middleware or replacement solutions that connect actuarial outputs to accounting systems.

It depends on your transition approach. Full retrospective application requires data back to contract inception. Modified retrospective needs fewer years but still demands historical premiums and claims. Fair value approach minimizes historical requirements but affects opening balance sheet comparability.

Data remediation averages 12 to 18 months for mid-sized insurers. Large companies with multiple legacy systems often need 24 months. The timeline extends when historical data reconstruction is required or when multiple business units operate on different platforms.

Yes. Reinsurance held follows similar measurement principles to direct insurance. You’ll need contract-level data for ceded premiums, expected recoveries, and cash flow timing. The challenge intensifies when reinsurance terms don’t align cleanly with underlying direct contracts.

Most insurers update quarterly to align with reporting deadlines. Some run monthly calculations to smooth period-end workload. Real-time updates aren’t practical given the complexity involved. What matters more is maintaining current assumption libraries and contract inventories.

Getting your IFRS 17 data foundation right

IFRS 17 data requirements represent the biggest operational change most insurers face. You’re moving from aggregate tracking to contract-level detail across every system.

The standard demands integration between actuarial models, policy administration, claims processing, and general ledger. Legacy infrastructure wasn’t designed for this connectivity.

Data quality determines compliance success. Incomplete histories, mismatched identifiers, and manual processes all create risks that compound under tight reporting deadlines.

Purpose-built IFRS 17 software platforms solve what spreadsheets can’t. Automation handles volume and complexity while preserving audit trails and governance controls.

Your data architecture needs careful design before calculations begin. Contract grouping, assumption libraries, and reconciliation frameworks all require upfront planning.

Start preparation early and test thoroughly. Data gaps discovered during first live reporting cause delays and restatements that damage stakeholder confidence.

Prima Consulting helps insurers navigate IFRS 17 implementation from data assessment through ongoing reporting. Our team understands both the accounting standards and the technical infrastructure needed for compliance. Visit Prima Consulting to discuss your specific data challenges and implementation roadmap.