Selecting enterprise IFRS 9 ECL software determines whether your bank spends the next five years managing credit risk efficiently or fighting manual processes every quarter. Financial institutions evaluating solutions often focus on features without examining the structural requirements that separate functional software from enterprise-grade platforms. The difference shows up quickly during implementation, audit cycles, and regulatory reviews.

Enterprise IFRS 9 ECL software selection requires evaluating five critical dimensions: data integration scalability, regulatory compliance controls, model governance frameworks, total cost structures, and implementation timelines. Banks that skip this evaluation framework typically discover gaps after deployment when changing vendors becomes costly and disruptive.

What Is Enterprise IFRS 9 ECL Software Selection?

Enterprise IFRS 9 ECL software selection means identifying platforms that handle complex portfolios across multiple jurisdictions while maintaining audit trails and regulatory compliance. The process differs from standard software evaluation because IFRS 9 implementations directly affect balance sheets, capital ratios, and regulatory standing.

Software must calculate expected credit loss provisions using probability of default, loss given default, and exposure at default models. These calculations run continuously as loan portfolios change and economic forecasts shift. Enterprise platforms process thousands of facilities simultaneously while maintaining drill-down transparency to individual exposures.

The selection process evaluates whether software scales with portfolio growth, integrates with existing banking systems, adapts to regulatory changes, and provides complete model documentation. Banks need solutions that work today and accommodate expansion into new markets or product lines without requiring replacement.

Why Enterprises Need ECL Software for IFRS 9 Compliance

Manual spreadsheets break under enterprise portfolio volumes. A mid-size bank with 50,000 loans can’t reliably calculate staging classifications and ECL provisions using Excel formulas maintained by two analysts. Errors compound quickly when models span multiple sheets with external data links and complex macros.

In 2024, the IFRS 9 Expected Credit Loss Modeling Platforms market reached USD 2.85 billion globally, showing how banks worldwide recognized manual processes can’t meet current requirements. The market growth reflects institutions replacing spreadsheets with purpose-built platforms.

Regulators expect banks to explain ECL movements each quarter. When provisions increase by 15%, management must attribute changes to new business volumes, staging migrations, parameter updates, or economic scenario shifts. Manual systems can’t produce this attribution analysis within acceptable timeframes.

Audit requirements demand complete documentation from source data through final provisions. Auditors verify staging decisions, validate PD curves against historical performance, and test scenario probability weights. Software that hides calculations in black boxes creates friction during reviews and extends close cycles unnecessarily.

Build vs Buy: Enterprise IFRS 9 ECL Software Decisions

Banks face fundamental choices when addressing ECL calculation requirements. Building proprietary solutions offers complete control but requires sustained development resources and deep IFRS 9 expertise. Buying vendor platforms accelerates deployment yet introduces dependency on external support.

In-house development starts with a six to eighteen month timeline for basic functionality. Teams must code data integration layers, implement staging logic, build PD term structure engines, create LGD calculation modules, and develop reporting frameworks. Each component requires specialized knowledge that combines accounting standards, actuarial methods, and software engineering.

The ongoing maintenance burden grows as portfolios expand and regulations change. Internal teams handle bug fixes, performance optimization, and feature additions while supporting production operations. Staff turnover creates knowledge gaps that threaten system stability.

Vendor solutions reduce implementation timelines to three to six months through prebuilt templates and tested calculation engines. Providers handle regulatory updates and maintain documentation that supports audit requirements. Updates deploy through managed release cycles rather than internal development sprints.

That said, vendor platforms limit customization options compared to internal builds. Banks must adapt workflows to match software capabilities rather than designing perfect-fit solutions. Licensing fees recur annually while internal systems spread costs across longer periods.

The 5 Criteria to Evaluate Enterprise IFRS 9 ECL Software

Enterprise platforms must satisfy specific requirements that distinguish them from basic calculation tools. These five criteria form the evaluation framework that determines long-term viability.

How IFRS 9 Expected Credit Loss Models Work

Expected credit loss calculations apply forward-looking provisioning to financial instruments measured at amortized cost or fair value through other income. The framework replaces incurred loss models that recognized provisions only after credit events occurred.

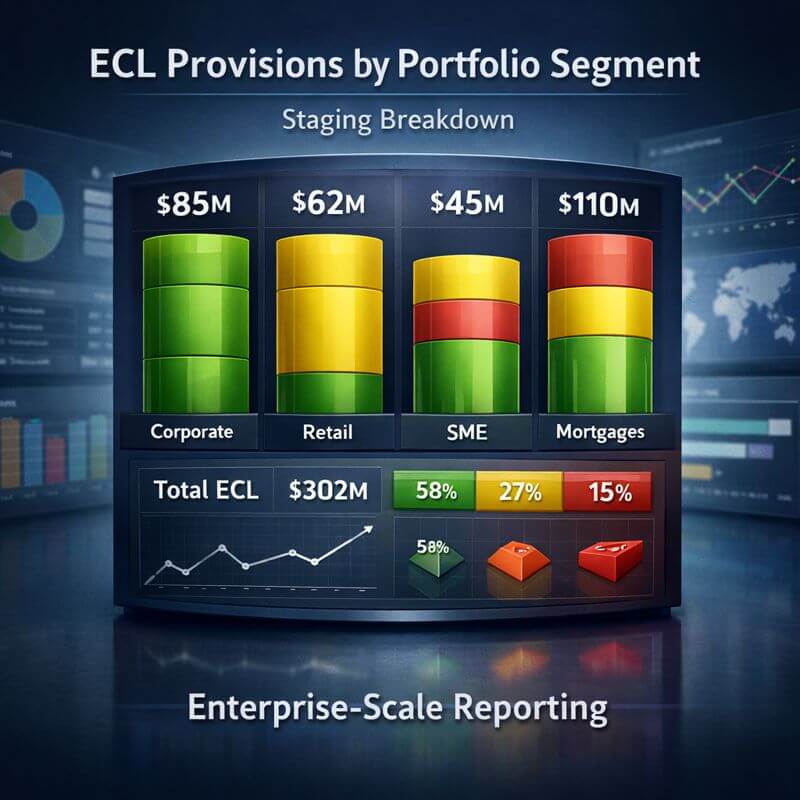

Banks classify exposures into three stages based on credit quality changes since initial recognition. Stage 1 assets show no significant increase in credit risk and carry twelve-month ECL provisions. Stage 2 exposures experienced meaningful credit deterioration and require lifetime ECL coverage. Stage 3 loans exhibit objective impairment evidence and use lifetime ECL with interest calculated on net carrying amounts.

The ECL formula combines three components at each future period. Probability of default estimates the likelihood an obligor fails to meet contractual obligations. Loss given default projects the economic loss percentage if default occurs. Exposure at default calculates the outstanding balance when default happens, accounting for scheduled repayments and commitment drawdowns.

Most institutions apply three to five macroeconomic scenarios when incorporating forward-looking information into ECL calculations. Base scenarios reflect most likely economic paths while optimistic and pessimistic cases capture uncertainty ranges. Probability weights generate expected values across scenarios.

PD, LGD, and EAD Modeling Explained

Probability of default curves show default likelihood across future time periods. Banks build PD term structures using historical default experience calibrated to current portfolio characteristics. Through-the-cycle PD estimates reflect long-run average default rates while point-in-time adjustments incorporate current economic conditions.

Loss given default estimation requires analyzing recovery experience by collateral type, seniority class, and obligor characteristics. Secured exposures show lower LGD due to collateral liquidation proceeds. Unsecured loans experience higher losses absent recovery sources. Banks apply haircuts to collateral values based on realization experience and market volatility.

Exposure at default modeling accounts for balance changes between reporting dates and default events. Amortizing loans show declining EAD as scheduled payments reduce principal. Revolving facilities require credit conversion factors that estimate commitment drawdowns before default. Banks calibrate factors using historical utilization patterns during stressed periods.

What Makes ECL Software “Enterprise-Grade”?

Enterprise platforms handle portfolio volumes exceeding 100,000 facilities while maintaining calculation speed and drill-down transparency. Systems process nightly batch runs within acceptable timeframes and support real-time queries during business hours.

Multi-entity consolidation capabilities aggregate ECL across subsidiaries while maintaining separate calculations by legal entity. Banks operating in multiple jurisdictions apply local regulatory requirements alongside group reporting standards. Software must track entity-specific parameters and produce both individual and consolidated disclosures.

Role-based access controls limit who modifies model assumptions, approves parameter changes, or views sensitive portfolio information. Audit trails capture every action with timestamps and user identifiers. Workflow automation routes model updates through approval chains that match governance policies.

Data Integration and Scalability for Enterprise ECL Models

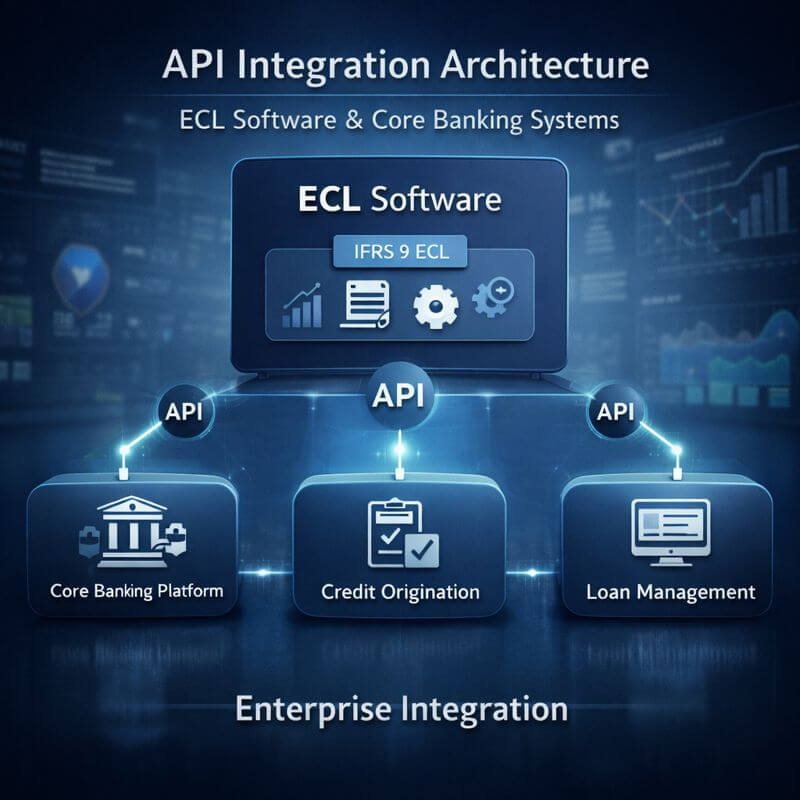

Core banking systems hold the loan-level data that feeds ECL calculations. Integration methods determine whether your bank manually exports files each month or receives automated real-time updates through APIs.

File-based integration requires scheduled extracts from source systems, manual quality checks, and upload processes that delay calculations. Batch workflows break when file formats change or new data fields appear. Staff spend hours troubleshooting integration issues rather than analyzing results.

API-native platforms connect directly to core banking systems through REST interfaces. Data synchronization happens automatically on defined schedules or triggered by specific events. Bidirectional integration posts calculated provisions back to general ledgers without manual journal entry creation.

North America commanded over 38% of the global IFRS 9 Expected Credit Loss Modeling Platforms market share in 2024, partly because regional institutions prioritized modern integration architectures that reduced operational risk.

Scalability testing should confirm platforms handle your current portfolio plus 200% growth without performance degradation. Calculate whether batch processing completes within acceptable windows as loan volumes increase. Test whether query response times remain acceptable when drilling down through large exposure populations.

Regulatory Compliance and Audit-Ready Controls

Regulators require banks to explain methodology choices, validate model performance, and document assumption changes. Software must generate the evidence packages that satisfy these requirements without extensive manual compilation.

Complete audit trails show who changed PD curves, when LGD parameters updated, and why management overlays applied. Average management overlays for Dutch banks decreased to 8% from 11% between 2023 and 2024, demonstrating how oversight of assumption changes affects reported provisions materially.

Software should produce methodology documentation automatically as configurations change. Technical specification documents describe staging logic, PD term structure construction methods, LGD estimation approaches, and scenario framework designs. Version control tracks documentation evolution as models refine over time.

IFRS 7 disclosure requirements mandate detailed reconciliations showing ECL movements between periods. Attribution analysis breaks changes into components driven by new originations, repayments, staging migrations, parameter updates, and economic scenario revisions. Disclosure templates populate automatically from calculation engines rather than requiring manual table construction.

How to Validate and Audit IFRS 9 ECL Models

Model validation compares predicted outcomes against realized experience. Back-testing engines track whether Stage 2 exposures default at rates consistent with calculated PD curves. Validation reports highlight where models underpredict or overpredict losses by portfolio segment.

Challenger models provide independent ECL estimates using alternative methodologies. Banks compare primary calculation results against challenger outputs to identify potential model weaknesses. Material differences trigger investigation into assumption reasonableness and methodology appropriateness.

External auditors require read-only system access to independently verify calculations. Platforms must support auditor queries without granting modification permissions. Export capabilities let auditors extract supporting detail for any provision amount without staff assistance.

Security, Data Privacy, and Access Controls

Customer financial data requires protection through encryption, access restrictions, and activity monitoring. Enterprise platforms apply encryption to data at rest and in transit using industry-standard algorithms. Database encryption prevents unauthorized access even if physical storage compromises occur.

Multi-factor authentication adds security layers beyond username and password combinations. Time-based tokens or biometric verification reduce credential theft risks. Session timeouts limit exposure from unattended workstations.

Data residency requirements in some jurisdictions mandate that customer information stays within national borders. Cloud deployments must run in regional data centers while on-premise installations keep data fully internal. Banks operating across multiple countries need solutions that accommodate varying regulatory expectations around data sovereignty.

Model Governance, Validation, and Transparency

Enterprise platforms provide built-in governance frameworks that track assumption changes and route updates through approval workflows. Parameter modifications require documentation explaining business justification and expected impacts. Senior risk officers review and approve changes before implementation.

Version control systems maintain complete histories of model configurations. Banks can reconstruct calculations from any prior reporting period by loading historical parameter sets. This capability supports regulatory requests for methodology explanations and enables impact analysis when refining approaches.

Sensitivity analysis tools show how provision levels respond to assumption changes. Banks test ECL sensitivity to unemployment rate shifts, GDP forecast revisions, or property value declines. Results inform scenario probability weight selections and support management overlay decisions when models appear misaligned with emerging risks.

Transparency requirements mean drilling from portfolio-level provisions to facility-specific calculations. Users click through from total ECL to segment breakdowns to individual exposure details. Every intermediate calculation step remains visible rather than hidden audit risks in IFRS 9 spreadsheets.

The average coverage ratio for amortized loans in European banking dropped from 1.40% in 2022 to 1.36% in 2023, showing material impacts from assumption refinements. Transparent platforms help banks explain these movements to stakeholders clearly.

Total Cost of Ownership for Enterprise ECL Platforms

Initial licensing fees represent only part of total software costs over five-year periods. Implementation services, annual maintenance, user training, infrastructure, and ongoing support combine to determine real economic impacts.

Perpetual licenses require large upfront payments but lower ongoing costs. Banks own software indefinitely and pay annual maintenance fees typically ranging from 15% to 20% of license values. This model suits institutions with stable long-term requirements and capital budget availability.

Subscription pricing spreads costs across contract terms through monthly or annual fees. Initial outlays decrease while ongoing expenses increase. Cloud-hosted subscriptions include infrastructure costs within subscription fees. On-premise subscriptions require separate hardware and administration budgets.

What Ongoing Costs Should Enterprises Expect?

Annual maintenance covers software updates, bug fixes, and technical support access. Fees typically range from 15% to 20% of initial license costs for perpetual models. Subscription pricing bundles maintenance into recurring payments without separate line items.

User training requires budget allocation for both initial onboarding and ongoing education as staff turn over. Training costs vary based on user counts, session formats, and customization needs. Plan for refresher training annually to maintain proficiency as software evolves.

Infrastructure costs include hardware for on-premise deployments or cloud service fees for hosted solutions. On-premise installations need servers sized for production workloads plus development and test environments. Cloud deployments shift infrastructure expenses from capital to operating budgets through monthly service charges.

Integration development connects ECL platforms to core banking systems and general ledgers. API-native solutions reduce integration costs compared to custom coding file transfer processes. Budget for initial integration plus ongoing maintenance as source systems upgrade.

Can ECL Software Adapt to Regulatory Changes?

Regulatory expectations around IFRS 9 continue evolving as supervisors issue updated guidance and interpretation changes. Software vendors should maintain regulatory monitoring teams that track these developments and incorporate requirements into product releases.

Release notes for each software version should detail regulatory updates addressed. Banks review these notes to understand which guidance changes the vendor handled versus which require internal policy decisions. Clear communication prevents surprises during audit reviews.

Configuration flexibility lets banks adapt to regulatory shifts without vendor involvement. When supervisors issue new staging guidance, administrators should modify SICR triggers through user interfaces rather than requesting custom code changes. This flexibility reduces dependency on vendor development cycles.

Implementation Speed and Ongoing Support

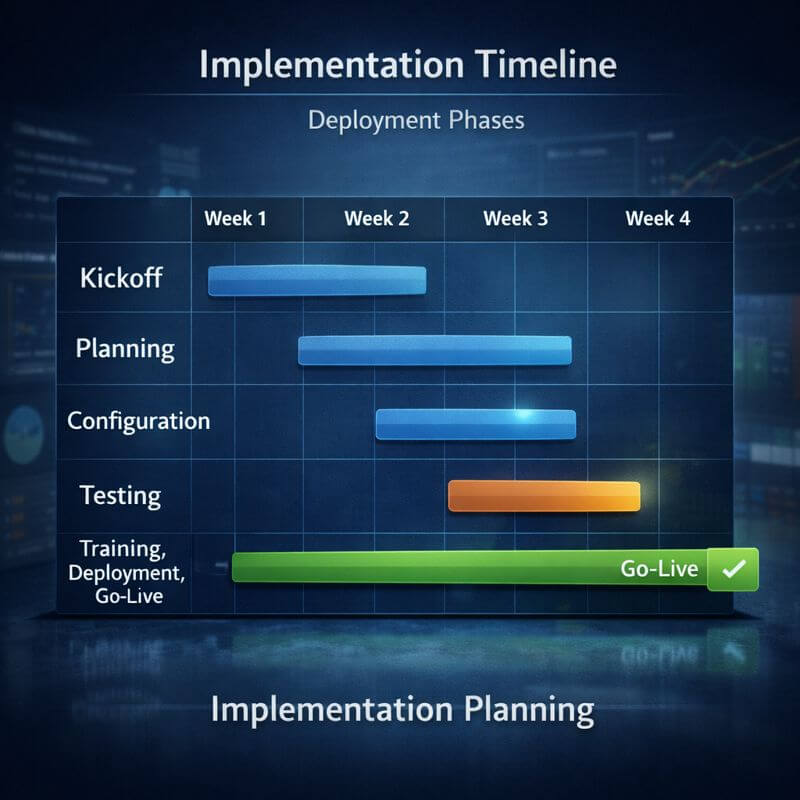

Standard implementations complete in six to twelve weeks when banks provide data access promptly and dedicate resources to configuration decisions. Complex portfolios or extensive customization extend timelines proportionally.

Prebuilt templates accelerate deployment by providing tested staging rules, standard PD term structures, and disclosure report formats. Banks customize templates to match specific requirements rather than building configurations from scratch. This approach cuts implementation time significantly compared to build vs buy IFRS 9 software TCO blank-slate deployments.

How Long Does It Take to Deploy ECL Software?

Simple implementations with standardized loan portfolios complete in eight to ten weeks. Timeline includes data integration setup, staging rule configuration, PD and LGD parameter population, user training, and parallel run validation. Banks with clean core system data and clear methodology documentation move faster.

Complex implementations requiring multiple entity consolidation, Islamic finance product support, or extensive workflow customization extend to twelve to sixteen weeks. Additional time accommodates extra configuration requirements and broader user training needs across multiple business units.

Parallel run periods validate that new software calculations match expectations before go-live. Banks run both legacy processes and new platforms simultaneously for one to two reporting cycles. Teams reconcile differences and refine configurations until results align acceptably.

When a Hybrid IFRS 9 Software Model Makes Sense

Some banks prefer hybrid approaches that combine vendor core platforms with internal custom modules for specialized requirements. Standard loan products run through vendor engines while unique instruments process through internal calculations. Results consolidate at the reporting layer.

Hybrid models work when banks have significant IT development capability and face requirements vendor platforms can’t accommodate. The approach requires maintaining integration between internal and external components plus version compatibility as vendors release updates.

Regional Regulatory Requirements (KSA, UAE, Pakistan, EU)

Different jurisdictions impose specific IFRS 9 implementation requirements beyond base standards. Software must accommodate these variations when banks operate across multiple regulatory regimes.

Saudi Arabian Monetary Authority provides detailed guidance on SICR indicators that Saudi banks must consider. Software serving KSA institutions should include these specific triggers in staging rule libraries. Local disclosure templates align with SAMA expectations rather than requiring manual reformatting.

Central Bank of UAE issues circulars clarifying IFRS 9 application in Emirati contexts. Platforms operating in UAE markets incorporate these requirements into standard configurations. Dubai International Financial Centre follows somewhat different rules than mainland UAE, requiring software that handles both frameworks.

State Bank of Pakistan publishes instructions on ECL calculation approaches for Pakistani banks. Software vendors targeting Pakistan build SBP-specific guidance into products rather than forcing banks to interpret instructions independently.

European Banking Authority technical standards affect all EU institutions. Software must generate FINREP and COREP reporting templates that match EBA specifications. The net ECL charges in European banking decreased 3% year-on-year in 2023, partly reflecting refined model calibrations across the region.

Frequently Asked Questions

How do enterprises validate IFRS 9 ECL models effectively?

Model validation compares predicted losses against actual default and recovery experience over time. Banks track whether Stage 2 migration rates, default frequencies, and recovery percentages align with model assumptions. Validation reports highlight segments where models consistently overestimate or underestimate risk. Independent risk functions perform validations quarterly or annually depending on portfolio complexity and regulatory expectations.

What data quality issues affect enterprise ECL calculations most?

Missing customer identifiers prevent exposure aggregation across products. Incomplete collateral records cause LGD calculation failures for secured loans. Inconsistent product classifications create staging rule application errors. Historical data gaps limit PD curve calibration accuracy. Banks should audit data quality before implementation and establish governance processes that maintain standards ongoing.

How do Islamic banking products affect IFRS 9 software selection?

Islamic finance structures like Murabaha, Ijarah, and Musharakah require modified cash flow generation logic. Profit rates replace interest rates in discount calculations. Ownership transfer timing affects exposure classification. Software must accommodate these differences while maintaining audit trails and regulatory compliance. Vendors serving Islamic markets include purpose-built modules rather than forcing institutions into conventional banking frameworks.

Can IFRS 9 ECL software handle purchased credit-impaired assets properly?

Purchased credit-impaired assets require lifetime ECL from initial recognition rather than staging classifications. Software calculates credit-adjusted effective interest rates and tracks changes in lifetime expected losses. These exposures report separately in disclosures. Enterprise platforms should include specific modules for PCI asset accounting that integrate with standard portfolio calculations.

What makes staging rule engines “enterprise-grade”?

Enterprise staging engines handle complex contagion logic that applies risk indicators across related exposures automatically. They support cooling-off periods that prevent premature stage reversals after temporary cures. They accommodate portfolio-specific SICR triggers beyond standard payment status and credit rating changes. Configuration interfaces let risk managers modify rules without coding while maintaining complete audit trails of logic changes.

How do forward-looking scenarios incorporate macroeconomic forecasts?

Banks obtain base, optimistic, and pessimistic economic forecasts from internal economics teams or external providers. These scenarios include GDP growth, unemployment rates, interest rates, property prices, and industry-specific variables. Software applies these factors to adjust PD curves and LGD estimates. Probability weights combine scenario results into expected values. Sensitivity tools show provision changes under alternative scenario designs or weight allocations.

What audit trail capabilities do regulators expect?

Complete audit trails capture who modified parameters, when changes occurred, what values changed, and why modifications happened. Trails cover staging rule updates, PD curve adjustments, LGD parameter changes, scenario weight revisions, and management overlay applications. Records remain immutable and accessible for regulatory reviews. Workflow logs show approval processes for material assumption changes.

How does ECL software handle multi-currency portfolios?

Multi-currency support calculates provisions in each loan’s denomination currency then consolidates to reporting currency using period-end exchange rates. Software maintains both individual currency and consolidated reporting views. Translation adjustments appear separately in ECL movement reconciliations. Banks operating globally require platforms that handle dozens of currencies simultaneously without performance impacts.

What differentiates vendor red flags during IFRS 9 software evaluation?

Red flags include vendors unable to provide customer references from similar institutions. Watch for demonstrations using only sample data rather than showing actual portfolio processing. Avoid vendors that cannot explain model transparency or provide unclear documentation. Question vendors pushing extensive customization rather than configuring standard functionality. Platforms requiring six-month-plus implementations for standard portfolios signal potential issues.

How do enterprises manage ongoing model governance after implementation?

Model governance committees meet quarterly to review calculation performance, approve parameter changes, and assess methodology appropriateness. Members include risk management, finance, internal audit, and business line representatives. Software-generated governance reports show model performance metrics, assumption changes since prior periods, and validation results. Formal documentation requirements apply to all material methodology updates.

Request an Enterprise IFRS 9 ECL Software Demo

Seeing software in action reveals capabilities that specification sheets can’t convey. Demonstrations should use your actual portfolio data rather than vendor sample files. This approach tests whether platforms handle your specific exposure types, staging scenarios, and reporting requirements.

Request demonstrations that show complete workflows from data integration through final disclosure generation. Watch how staging decisions apply, how PD curves build, and how attribution analysis decomposes provision changes. Ask presenters to drill down from portfolio totals to individual facility calculations.

Bring technical staff, risk managers, and finance team members to demonstrations. Different perspectives identify requirements that single-function viewers miss. Technical staff evaluate integration approaches while risk managers assess model governance features and finance teams check reporting flexibility.

Prepare specific scenarios that reflect your institution’s challenges. Ask vendors to show how software handles unusual exposure types, complex staging situations, or specific audit requirements you face. Generic demonstrations miss these critical details.

Visit IFRSTech IFRS 9 Compliance Software to schedule detailed platform demonstrations that address your specific requirements and evaluation criteria.

Get a Custom ECL Software Cost & ROI Analysis

Total cost of ownership calculations should compare all alternatives across five-year planning horizons. Include initial licensing or subscription fees, implementation services, training, infrastructure, annual maintenance, and support costs in analyses.

ROI calculations measure efficiency gains from automating manual processes, reduced audit findings, faster close cycles, and improved analytical capabilities. Banks replacing spreadsheet processes typically recover software investments within eighteen to twenty-four months through staff time savings alone.

Risk reduction benefits include fewer calculation errors, complete audit trails, and improved regulatory standing. While difficult to quantify precisely, these benefits matter materially when regulators identify control weaknesses or auditors issue findings.

Scalability value grows as portfolios expand. Software that accommodates growth without additional licensing costs or performance degradation delivers increasing returns over time. Calculate whether platforms support your projected growth without requiring replacement.

Talk to an IFRS 9 ECL Implementation Expert

Implementation planning determines whether projects finish on time and on budget or extend indefinitely while costs accumulate. Experts with multiple deployment experiences anticipate common challenges and structure projects to avoid known pitfalls.

Ask potential vendors about implementation team qualifications. How many IFRS 9 deployments have team members completed? Do they include banking professionals who understand portfolio dynamics alongside technical experts? Can they provide references from similar institutions?

Clarify exactly what implementation packages include. Does pricing cover data integration development, configuration services, user training, and go-live support? What falls outside scope and requires separate engagement? Understanding boundaries prevents budget surprises mid-project.

Request detailed project plans showing task sequences, resource requirements, and decision points. Plans should identify where bank staff input proves critical versus where vendors work independently. Clear plans set realistic expectations and enable effective progress tracking.

Schedule Your IFRS 9 Readiness Assessment

Readiness assessments evaluate whether your bank has the data quality, resource availability, and organizational alignment needed for successful implementation. Assessments identify gaps requiring attention before formal projects begin.

Data quality checks verify that core systems contain the fields required for ECL calculations. Missing customer identifiers, incomplete collateral records, or inconsistent product classifications create implementation obstacles. Address these issues proactively rather than discovering them during configuration.

Resource availability matters because implementations require sustained attention from business and technical staff. Identify who will make methodology decisions, configure staging rules, validate results, and train end users. Confirm these people have capacity during implementation periods.

Organizational readiness means stakeholders understand project goals and support implementation approaches. Secure executive sponsorship early to resolve cross-functional disagreements quickly. Implementation success requires coordinated effort across risk, finance, IT, and treasury functions.

Contact IFRSTech today to begin your enterprise IFRS 9 ECL software evaluation and implementation planning process.