TL;DR

Your IFRS 17 compliance solutions may be producing outputs, but regulators want more than numbers. They want audit trails, traceable data, and documented controls. Manual processes can’t deliver that reliably. This article covers why spreadsheet-based ifrs 17 solutions fail regulatory reviews, where data validation and grouping challenges create compliance risk, and what audit-ready looks like heading into 2026. Read on to see where your current setup stands.

Why Regulators Are Flagging Manual IFRS 17 Compliance Solutions

You’ve completed your IFRS 17 implementation. The reports are running, and disclosures are out. So why are regulators still asking questions?

The answer often comes back to how IFRS 17 compliance solutions were built. Across the insurance industry, manual processes, fragmented data, and weak validation controls are drawing increasing scrutiny from auditors and regulators.

This article breaks down what’s going wrong, where the risks are, and what stronger IFRS 17 compliance solutions actually look like.

Why Regulators Question Manual IFRS 17 Compliance Solutions

Manual approaches to IFRS 17 were often adopted out of necessity. Tight implementation timelines and legacy infrastructure left many insurers relying on spreadsheets, offline models, and patchwork reconciliation workflows.

That’s a problem regulators are now paying close attention to. The core issue isn’t effort. It’s reproducibility, traceability, and error tolerance.

Regulators want audit-ready reporting. They want to trace every liability figure back to its source data. Manual IFRS 17 compliance solutions, by design, make that difficult. Data moves between systems with no automated lineage. Calculations happen outside controlled environments. Reconciliation depends on individual judgment.

What’s interesting is that many insurers believe they’ve achieved compliance. But compliance is not just about producing the right output. It’s about proving it, defending it, and replicating it across periods without error.

What Are IFRS 17 Compliance Solutions?

IFRS 17 compliance solutions are the tools, systems, and processes insurers use to meet the reporting requirements of IFRS 17.

At their most basic, they handle three things: data collection and validation, actuarial calculations including GMM, PAA, and VFA measurement, and financial disclosure and period-close reporting.

In practice, the quality of IFRS 17 solutions for insurance varies widely. Some insurers built integrated platforms with end-to-end automation. Others cobbled together spreadsheets, scripts, and legacy models. It’s the latter group that’s facing the most regulatory heat right now.

A 2025 study published by the Casualty Actuarial Society found that among Asian general insurers, 63% of respondents still planned to use Excel for onerous testing or loss component calculations under IFRS 17. That level of spreadsheet dependency is exactly what regulators are flagging.

Key Risks of Manual IFRS 17 Processes

Manual IFRS 17 processes carry risks that go well beyond basic calculation errors. They create systemic vulnerabilities in how financial data is managed, controlled, and reported.

Data Accuracy and Audit Trail Gaps

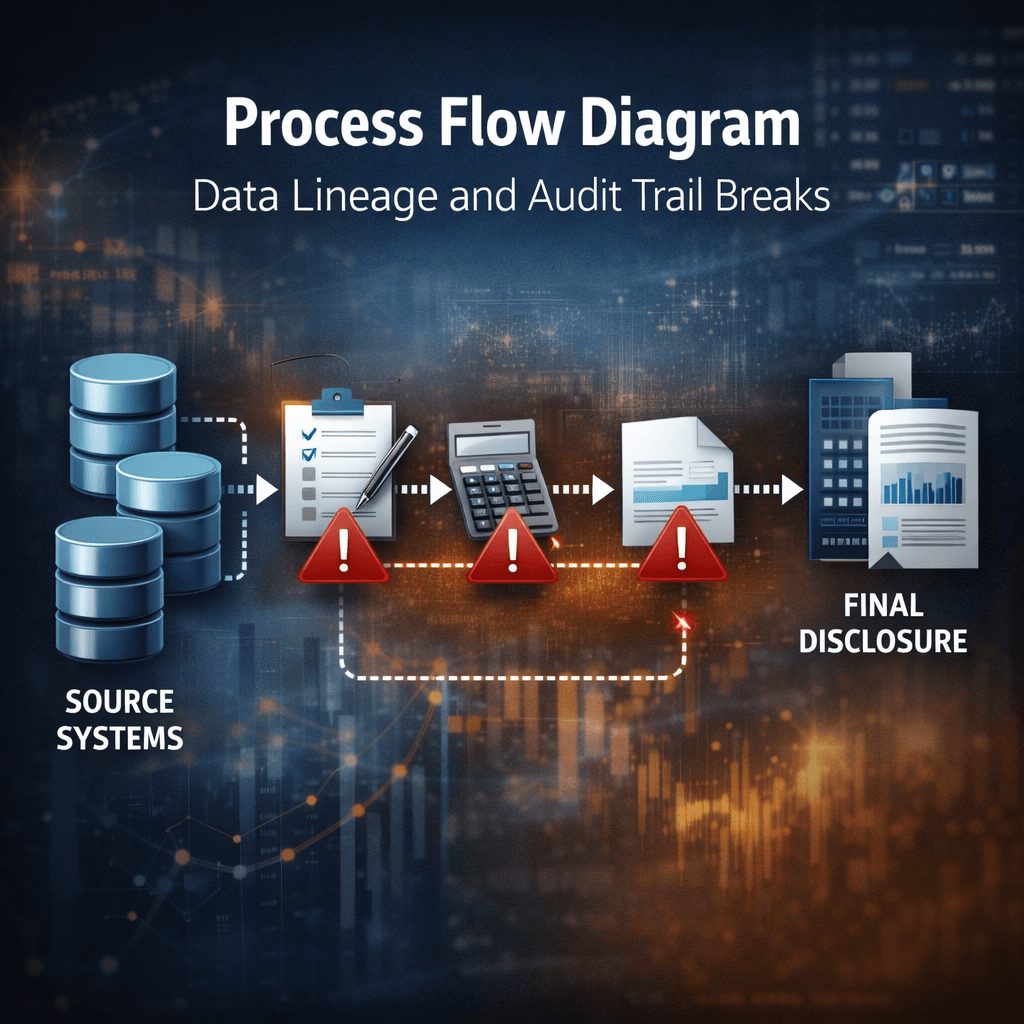

IFRS 17 requires contract-level data granularity. Every premium, claim, and liability needs to be traceable to its source. Manual data pipelines break that chain.

Data gets transferred manually between systems. Formats change. Mapping rules aren’t documented. By the time a figure appears in a disclosure, the path it traveled is often impossible to reconstruct. Auditors ask for audit trails. Manual systems can’t produce them cleanly.

Model Governance and Control Weaknesses

IFRS 17 compliance solutions must include model governance. That means version control, validation sign-offs, change logs, and documented assumptions.

Manual environments rarely have this. Models get updated without change records. Assumptions shift between periods without documentation. When regulators request evidence of model governance, the response is often incomplete.

This is where ifrs 17 solutions for insurance start to fail the audit standard, not the technical standard.

Spreadsheet Dependency and Version Risk

Spreadsheets are the most common form of manual IFRS 17 compliance tool. They’re also the riskiest.

A single formula error in a core calculation spreadsheet can cascade across all related outputs. Version risk is constant. Different teams may be working from different file versions without realizing it. There’s no single source of truth.

For IFRS 17 general insurance solutions in particular, where short-duration contracts and PAA simplifications are common, spreadsheet dependency is widespread. So is the regulatory exposure that comes with it.

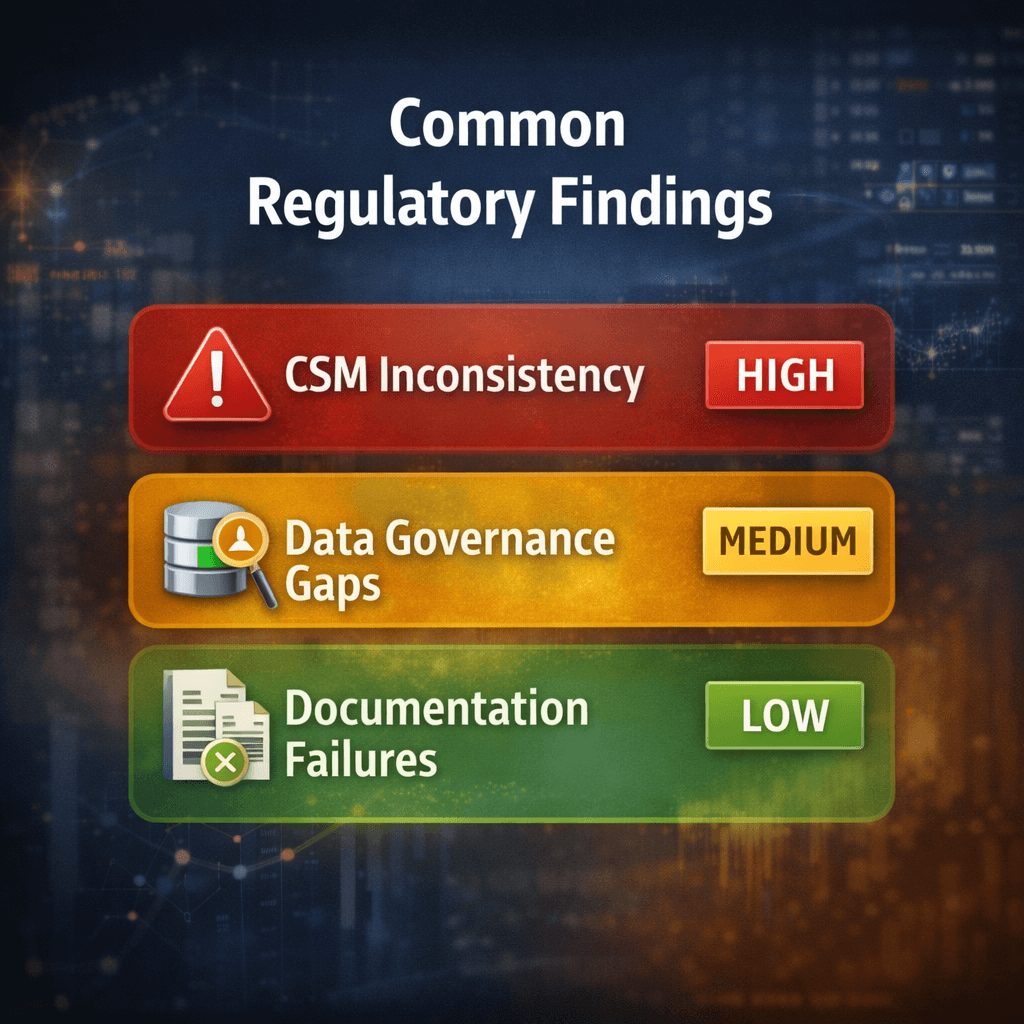

Common Regulatory Findings in IFRS 17 Reviews

Regulatory reviews of IFRS 17 reporting are surfacing recurring problems. These aren’t edge cases. They reflect structural weaknesses in how manual IFRS 17 compliance solutions were designed.

Inconsistent CSM Calculations

The Contractual Service Margin is one of the most scrutinized elements of IFRS 17. It requires consistent grouping of contracts, reliable future cash flow estimates, and defensible risk adjustment inputs.

In manual environments, CSM calculations often vary between periods in ways that can’t be explained by genuine economic change. Grouping logic shifts. Risk adjustment methodologies aren’t applied consistently. That’s a red flag for any regulator or external auditor.

The IFRS 17 end-to-end non-life solution problem is especially visible here. Non-life insurers applying PAA don’t have the same CSM complexity, but they face similar issues with onerous contract testing and loss component tracking when those processes are manual.

Weak Data Governance Frameworks

Data governance under IFRS 17 isn’t optional. Regulators expect insurers to document where data comes from, how it’s validated, and who approved it.

Manual ifrs17 solutions often have informal governance at best. Data owners aren’t clearly defined. Validation policies exist on paper but aren’t enforced in practice. Input controls are missing or inconsistent across business units.

For ifrs 17 solutions that span multiple legal entities or geographies, this becomes even more problematic. Governance gaps multiply across jurisdictions.

Inadequate Documentation and Controls

Regulators also look at documentation quality. Can the insurer explain its methodology choices? Is there a written record of how grouping criteria were set? Are assumption changes documented with sign-off?

Manual IFRS 17 compliance solutions almost always struggle here. Documentation is an afterthought, not a built-in output. The result is a compliance narrative that can’t hold up under detailed review.

How to Strengthen IFRS 17 Compliance Solutions

The path to stronger IFRS 17 compliance isn’t about overhauling everything at once. It starts with identifying where manual processes introduce the most regulatory risk.

Automating Data Integration and Validation

Data validation is the first place to improve. Automated validation rules catch format errors, missing values, and out-of-range inputs before they reach calculation engines.

This is especially critical for ifrs 17 data management systems, where inputs come from multiple source systems including policy admin, claims, and actuarial platforms. Automated integration removes the human handoff risk that creates audit trail gaps.

Stronger IFRS 17 compliance solutions build validation into the data pipeline itself, not as a manual review step at the end. From there, every figure that enters the calculation layer has a documented origin.

Strengthening Actuarial-Finance Alignment

One of the most persistent challenges in IFRS 17 is the disconnect between actuarial and finance teams. Actuarial models produce outputs that finance teams then manually reformat, reconcile, and load into disclosure templates.

That handoff creates risk. Numbers change in transit. Reconciliation fails. Sign-offs happen without full visibility of the underlying data.

Stronger ifrs 17 insurance reporting tools build actuarial-finance alignment into the workflow. A single data model feeds both the valuation engine and the reporting layer, with no manual reformatting in between.

Building Robust Internal Controls

Internal controls under IFRS 17 need to be formalized, not informal. That means documented control objectives, assigned ownership, regular testing, and evidence of sign-off at each stage.

For IFRS 17 compliance solutions to stand up to regulatory review, controls need to be embedded in the process, not bolted on at period end. That includes maker-checker workflows for key calculations, automated reconciliation between source data and outputs, and documented exception handling.

Manual vs Automated IFRS 17 Compliance Solutions

The choice between manual and automated IFRS 17 compliance solutions isn’t just a technology decision. It’s a risk management decision.

Cost, Risk, and Scalability Comparison

Manual solutions appear cheaper in the short term. The real costs show up later: in extended close cycles, in staff hours spent on reconciliation, and in regulatory remediation when findings emerge.

Automated ifrs17 solutions reduce those costs by design. They also scale more cleanly as contract volumes grow or as regulatory requirements change. A manual solution that works for a mid-size insurer today may collapse under the weight of expanded disclosure requirements in 2026 and beyond.

Think about it this way: the cost of a regulatory finding, including remediation, restatement risk, and reputational impact, almost always exceeds the cost of building a more robust solution from the start.

Long-Term Reporting and Disclosure Impact

IFRS 17 disclosures are getting more detailed, not less. Regulators and investors are asking for more granular breakdowns of liability movements, risk adjustment changes, and CSM roll-forwards.

Manual IFRS 17 compliance solutions aren’t designed for this. They produce point-in-time outputs rather than continuous, traceable reporting. As disclosure expectations increase, the gap between manual and automated solutions will only widen.

Stronger ifrs 17 data management systems make this transition manageable. They store period data in structured formats, enable comparison across periods, and generate disclosures directly from validated source data.

2026 Checklist for Audit-Ready IFRS 17 Compliance

If you’re reviewing your IFRS 17 compliance solutions ahead of the next reporting cycle, here’s what audit-ready looks like in practice.

Governance and Control Framework

You need documented data ownership across all source systems. Validation policies must be written, not assumed. Model governance records should include version histories, assumption change logs, and sign-off evidence. Internal control testing results must be retained for audit review.

Technology and System Readiness

Source-to-disclosure data lineage must be traceable without manual reconstruction. Calculation engines must be version-controlled and deployed consistently across entities. Automated reconciliation should flag discrepancies before period close, not after.

Regulatory Reporting and Disclosure Controls

Disclosure outputs must tie back to validated source data. CSM roll-forward schedules must reconcile to actuarial outputs. Exception handling procedures must be documented and applied consistently. PAA onerous contract tests and loss component tracking must leave auditable records.

For insurers using IFRS 17 solutions across non-life and life portfolios, the checklist should be entity-specific. Grouping criteria, measurement model choices, and disclosure formats may differ, but the underlying control standards don’t.

People Also Ask: IFRS 17 Compliance Solutions

What are the most common IFRS 17 compliance failures?

The most common failures involve inconsistent CSM calculations, poor data governance, and the lack of audit trails in manual processes. Grouping errors and undocumented assumption changes are also frequently cited in regulatory reviews.

Why do manual IFRS 17 processes lead to regulatory scrutiny?

Manual processes can’t produce the audit trails, version control, and data lineage that regulators expect. They also introduce version risk, reconciliation errors, and governance gaps that automated systems are designed to prevent.

What is the difference between PAA and GMM in IFRS 17?

The Premium Allocation Approach is a simplified model for short-duration contracts, commonly used in non-life insurance. The General Measurement Model applies to most other contracts and requires full cash flow projections and a CSM. The Variable Fee Approach is used for participating contracts where returns are linked to underlying items.

How do grouping errors affect IFRS 17 compliance?

Grouping errors cause contracts to be classified incorrectly, which distorts CSM calculations, onerous contract identification, and liability measurement. Regulators look for grouping consistency across periods and between entities.

What should IFRS 17 compliance solutions include by 2026?

By 2026, IFRS 17 compliance solutions should include automated data validation, documented model governance, traceable audit trails, integrated actuarial-finance workflows, and disclosure outputs that tie directly to validated source data.

What Manual IFRS 17 Gaps Mean for Your Compliance Position

Manual IFRS 17 compliance solutions were built for a deadline, not for the long term. The regulatory landscape is catching up fast.

Data validation issues, grouping inconsistencies, and weak governance frameworks are no longer tolerated as growing pains. They’re being treated as structural compliance failures.

Insurers that address these gaps now, before the next reporting cycle, are the ones that will move through regulatory reviews without disruption. Those that don’t face mounting remediation costs and reputational exposure.

If your IFRS 17 compliance solutions rely on manual processes, the time to act is now. Prima Consulting works with insurers to assess and strengthen IFRS 17 compliance frameworks, from data governance to disclosure controls. Reach out to start a conversation about where your current setup stands.