IBNR Software Solutions: Risks of Estimating Without One

How insurers relying on manual IBNR processes expose their reserves, audits, and IFRS 17 compliance to risks that no spreadsheet formula can patch.

✓ Written by IFRS TECH’s advisory team · ✓ Serving GCC, Europe & APAC · ✓ Actuaries + CPAs + CFAs

TL;DR

IBNR software solutions exist for a reason: manual estimation fails at scale, fails under audit, and fails IFRS 17 reserving requirements. This article covers why estimation risks multiply without the right tools, how data and version control issues compound over time, and what insurers operating on spreadsheets are actually putting at risk. If your team hasn’t moved to a purpose-built ibnr software process, the cost of that delay is already accumulating.

What this article covers:

- Why manual IBNR reserving breaks under IFRS 17 disclosure demands

- How audit and regulatory risks grow when estimation processes aren’t defensible

- What scaling looks like without specialized ibnr software solutions

In 2024, US insurers added USD 16 billion to prior-year liability loss estimates during reserve reviews. That number isn’t a market anomaly. It’s what happens when estimation processes can’t keep up with claims complexity, portfolio growth, and regulatory demands.

Most reserve failures don’t start with bad actuaries. They start with bad tools. Or worse, with no tools designed for the job at all.

IFRS TECH works with insurers across GCC, Europe, and APAC who are navigating this problem right now. The pattern is consistent: the longer a team relies on manual processes, the more embedded the risk becomes, and the more expensive the correction.

What IBNR Estimation Without Specialized Tools Actually Costs

Most teams underestimate this. They see the spreadsheet as free. What they don’t see is what’s accumulating beneath it.

Adverse prior-year development across all US liability lines hit $7.8 billion in 2024, more than double the $3.7 billion reported the year before. For casualty lines specifically, adverse development reached $15.8 billion, the highest level on record. Milliman’s analysis points directly to actuarial assumptions that didn’t keep pace with actual claims experience.

That gap between assumption and reality widens faster when estimation tools can’t process granular data, run multiple methods simultaneously, or flag inconsistencies automatically. Spreadsheets can’t do any of those things reliably at scale. The manual process doesn’t warn you when your loss development factors are drifting. It just records what you put in.

Here’s a question worth sitting with: how would your current team know if your IBNR estimate was materially off by the time the next audit cycle started?

Quick Estimation Risk Check

Ask your actuarial team these four questions:

- Can you reproduce last quarter’s IBNR estimate exactly, step by step, from a documented trail?

- Does your current tool flag when a development factor falls outside historical bounds?

- Is your process compliant with IFRS 17 disclosure requirements without a manual translation step?

- If your lead actuary left tomorrow, could the next person re-run the same model without starting over?

If any answer is “no,” the process has embedded risk.

Why Manual IBNR Reserving Fails Under IFRS 17

IFRS 17 didn’t just change reporting. It changed what “defensible” means.

Under the old regime, a reserve number with a licensed actuary’s signature was largely good enough. IFRS 17 requires insurers to disclose the assumptions behind their estimates, explain movements in reserves period to period, and demonstrate that their liability for incurred claims reflects current expectations, not historical conventions. That’s a fundamentally different standard. A spreadsheet built for chain ladder calculations doesn’t answer those questions. It stores the output. It doesn’t build the case.

Teams working with ibnr solution with ifrs 17 reserving built in find this process far cleaner. The methodology is documented inside the tool. The inputs are version-controlled. Disclosure outputs are built for regulators, not translated for them after the fact.

Data Entry Is Not an Actuarial Method

This one matters more than it sounds. Manual IBNR processes require someone to move data from claims systems into estimation models. That step introduces human error at the exact point where precision is most critical.

A single transposition in a run-off triangle can move a reserve estimate by millions, depending on portfolio size. There’s no automated check. The model processes whatever it receives. And in a quarterly cycle, that error may not surface until the following period’s development review, by which time financial statements have already been reported.

Purpose-built actuarial saas providers for ibnr compliance connect directly to source data. The manual transfer step disappears. So does the error rate it carries.

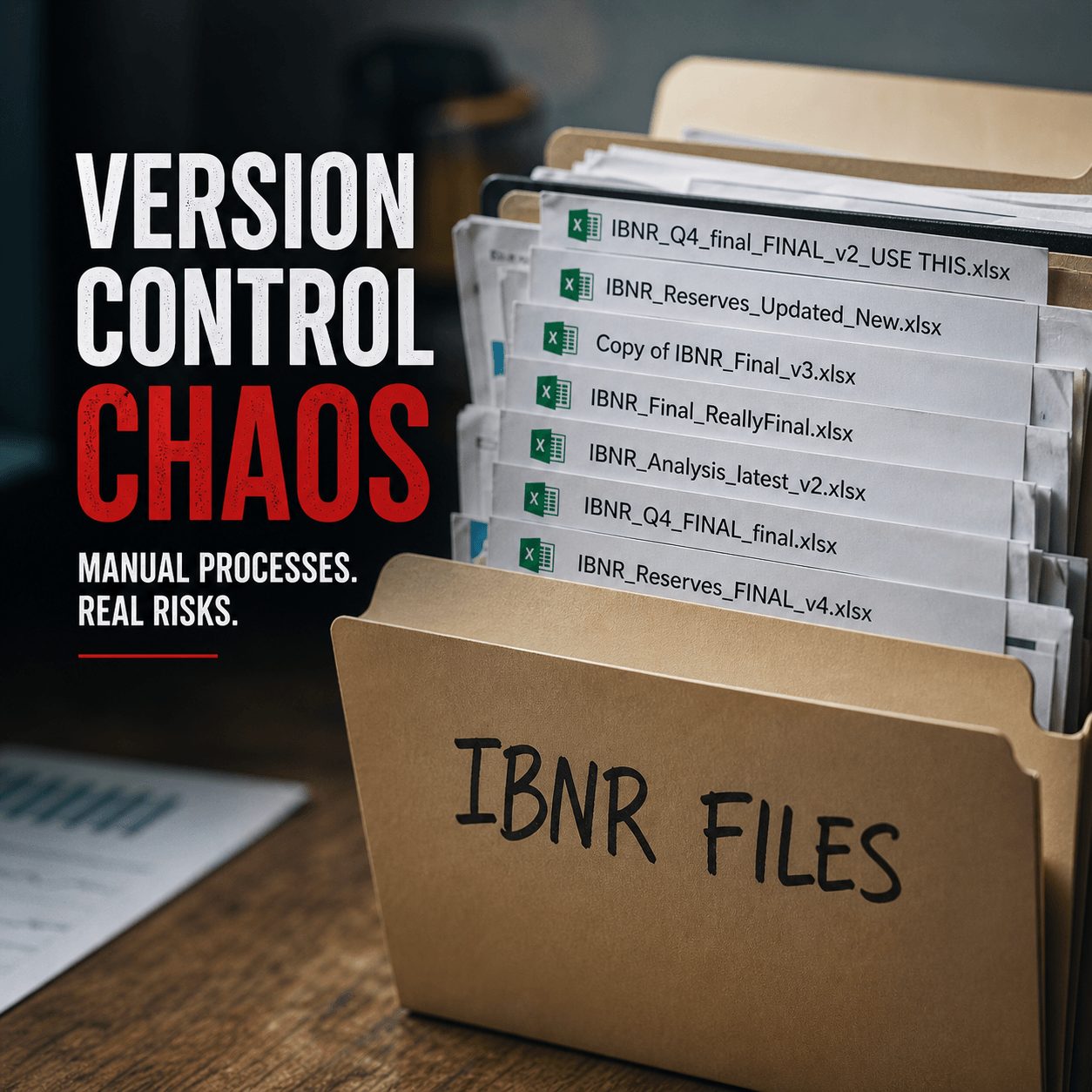

Version Control Is the Risk No One Talks About

Ask a team running manual IBNR processes which version of the model produced last quarter’s reserve. Nine times out of ten, there’s hesitation. There’s a folder with three versions of a file named something like “IBNR_Q4_final_v3_REVISED_USE THIS ONE.” Nobody wants to admit what’s actually in it.

That’s not a process failure. It’s what manual version control looks like in practice.

When auditors or regulators ask to trace a reserve number back to its source, that folder is your evidence. It’s not enough.

If your team is reviewing ifrs 17 actuarial tools in insurance, version control and audit trail capability should be the first filter. Not interface design. Not price. Those come after.

The Audit Risk Hiding in Your Spreadsheets

Reserve adequacy audits are getting harder. That’s not an opinion. Over the decade from 2015 to 2024, total adverse development in commercial liability lines accumulated to USD 62 billion globally. Regulators are paying attention. Audit standards are tightening in response.

The question isn’t whether your estimates will be challenged. It’s whether your process can withstand that challenge when it comes.

Regulators Can’t Audit a Spreadsheet Trail

IFRS 17 requires disclosure of estimation uncertainty. In plain terms: you need to show not just what your reserve is, but why it’s defensible, what assumptions drove it, and what the sensitivity looks like if those assumptions shift. A spreadsheet model can’t produce that documentation automatically. A team producing it manually is spending actuarial time on compliance formatting instead of analysis.

The ifrs 17 non life solutions that serve this market correctly build regulatory output as part of the core workflow, not as an add-on. That distinction matters when your regulator asks for documentation with a 72-hour deadline.

What Happens When the Auditor Asks “How Did You Get Here?”

There’s a specific kind of uncomfortable silence that happens in audit meetings when a reserve number can’t be traced to a documented, reproducible process. The actuary who built the model is the only person who knows how it works. That person may have left the company. Or they may be on leave. Or the original file may have been overwritten.

This is not hypothetical. It’s a common failure point in manual IBNR processes.

Purpose-built ibnr software solutions log every assumption, every method selection, every input change. The audit trail exists by default, not because someone thought to create it.

Is your IBNR process ready for a disclosure audit?

IFRS TECH’s actuarial team runs a 5-question IBNR Readiness Assessment for insurers evaluating their current reserving workflow against IFRS 17 requirements.

Scaling Breaks Manual IBNR Processes

Small portfolios forgive manual processes. A team of two actuaries running 15 lines of business through a shared spreadsheet can manage. Until they can’t.

Growth changes the math. More lines of business mean more triangles, more lag patterns, more judgment calls, and more opportunities for inconsistency. The manual process doesn’t scale linearly, it breaks at a threshold, usually at the worst possible time: mid-year close, a portfolio acquisition, or a regulatory filing deadline.

When Portfolio Volume Outgrows Your Tools

The threshold varies. But one thing is consistent across every insurer that hits it: they knew the manual process was under strain before it actually failed. They just didn’t address it in time.

That pattern exists because switching to specialized ibnr software solutions feels expensive and disruptive when the current process is still technically working. Then it stops working, and the cost of the switch plus the cost of the failure lands at once.

AM Best estimated an $18.8 billion deficiency in net loss and LAE reserves across the US market as of 2024, driven in part by processes that couldn’t keep pace with claims complexity. That’s the industry-wide version of what happens at the portfolio level when tools don’t match the workload.

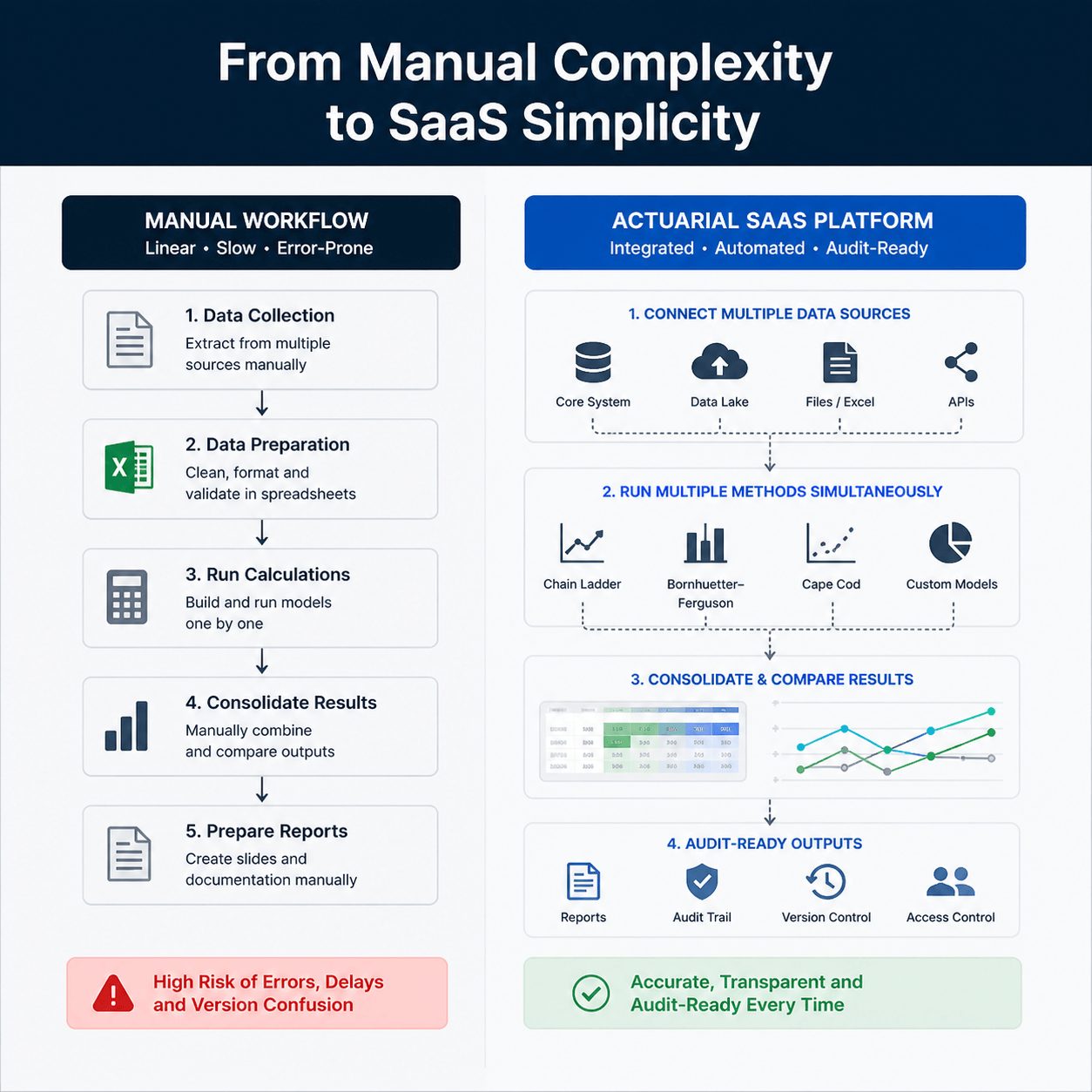

How Actuarial SaaS Providers Solve the Scaling Problem

Dedicated actuarial saas platforms don’t just automate the calculation. They standardize the process so it can run across multiple lines, multiple geographies, and multiple time periods without requiring proportional increases in actuarial headcount.

Arius, one of the longer-standing actuarial reserving platforms, estimates that its users process reserves up to four times faster than with spreadsheets. That speed isn’t the point. The reliability is. Speed is just the signal that the process is actually working as designed.

IFRS TECH has supported insurance clients across Saudi Arabia, the UAE, and Europe in transitioning from manual reserving to compliant IBNR workflows. The consistent finding: audit preparation time drops, and reserve volatility narrows within two reporting cycles. See ifrs 17 vendors for scalable compliance for specifics.

The Compliance Gap Between Basic and Specialized IBNR Solutions

Not every tool called an “IBNR solution” actually is one.

There’s a category of general financial modeling tools that can produce reserve estimates if you configure them correctly. Many insurers use them. They work up to a point. But they weren’t built for the specific demands of actuarial reserving under IFRS 17, and that gap shows up in four places: method flexibility, disclosure generation, integration with claims systems, and stochastic modeling support.

IFRS 17 Reserving Demands More Than Chain Ladder

Chain ladder is a starting point. It’s not an answer. IFRS 17 expects insurers to consider multiple estimation methods and to explain why the selected approach reflects current claims experience. A tool that only runs chain ladder doesn’t give you that flexibility. You get one lens, and regulators are asking for several.

The ifrs 17 software solutions that support IBNR properly run Bornhuetter-Ferguson, Cape Cod, and frequency-severity methods alongside chain ladder, with comparative outputs that make the actuarial judgment transparent rather than opaque.

Why a Generic Tool Is Not an IBNR Solution

Generic financial tools treat IBNR as a number. Specialized ibnr software solutions treat IBNR as a process. That’s the whole difference.

A process includes documentation of assumptions. It includes sensitivity testing. It includes period-over-period comparison with explanation of movements. A number produced by a general-purpose spreadsheet has none of that built in. You have to build it yourself, every quarter, from scratch.

Teams doing this manually are spending roughly 40-60% of their reserve cycle time on process management rather than actuarial analysis. That estimate comes directly from client engagements, not from a study, and I’d welcome pushback on it from teams that have measured it differently. But the direction is consistent.

Look at it this way: if your actuaries are spending more time formatting outputs than evaluating assumptions, the tool is failing you.

Transition Risks: Moving From Manual to Automated IBNR Tools

This section is where most guides stop short. They explain the risks of staying manual but say almost nothing useful about the risks of switching.

Transitions are hard. Data migration from manual processes often uncovers inconsistencies that were previously invisible. Historical triangles built in spreadsheets may not transfer cleanly into structured databases. Actuarial judgment embedded in cell formulas doesn’t document itself.

The right approach to transition is parallel running. Keep the manual process operational while the new system is validated over at least two full reserve cycles. Don’t kill the spreadsheet until the new tool has matched outputs on live data. That sounds slow. It’s slower to recover from a transition failure during a regulatory filing period.

The ifrs 17 end to end non life solution framework IFRS TECH uses for implementation builds parallel running into the project plan by default. It adds eight to twelve weeks to the timeline. It also prevents the category of failures that come from switching too fast.

One more thing about transition: the staff who built the manual process often feel threatened by the change. That’s a people problem, not a technology problem, and it matters more than the vendor selection in many cases. Address it directly.

What You Now Know

- Manual IBNR estimation processes create measurable audit, compliance, and scaling risks that compound over time. The $16 billion in reserve additions across the US market in 2024 reflects, in part, what happens when actuarial assumptions can’t be updated fast enough with the tools available.

- IFRS 17 reserving requirements aren’t compatible with spreadsheet-based processes. Disclosure obligations, assumption documentation, and period-over-period movement analysis require purpose-built ibnr software solutions, not general financial modeling tools configured for the task.

- Transition from manual to automated IBNR tools carries its own risks and should include parallel running over at least two reserve cycles. The cost of a poorly managed switch is comparable to the cost of staying manual too long.

The industry’s reserve adequacy problems aren’t going away. Other liability-occurrence lines showed $10.3 billion of adverse development in 2024 alone. Social inflation, litigation trends, and claims complexity are outpacing the backward-looking methods that most manual processes rely on.

Specialized ibnr software solutions don’t guarantee accurate reserves. Nothing does. But they close the gap between your estimation process and the standards that regulators, auditors, and IFRS 17 now require. That gap is where the risk lives.

Your next reserve cycle is the right time to close it.

Teams that have already reviewed their options will find that the ifrs 17 software vendor shortlist process surfaces both the capability differences between tools and the implementation questions that matter most. Start there, not with a demo request.

See how IFRS TECH’s IBNR advisory team handles estimation risk, disclosure compliance, and IFRS 17 reserving for non-life insurers.

We’ve supported insurers from initial gap analysis through to first compliant reporting period, across GCC, Europe, and APAC markets.

Frequently Asked Questions

What are the main risks of IBNR estimation without specialized software?

The primary risks are data entry errors in manual triangle construction, lack of version control on model assumptions, inability to produce IFRS 17-compliant disclosure outputs, and audit trails that can’t withstand regulatory scrutiny. These risks compound as portfolio volume grows and reserve cycle frequency increases.

How does IFRS 17 change IBNR reserving requirements for insurers?

IFRS 17 requires insurers to disclose the assumptions behind their liability for incurred claims, explain period-over-period reserve movements, and demonstrate that estimates reflect current expectations. Manual ibnr solutions typically produce a number but not the documented process IFRS 17 demands, creating compliance gaps that surface during audit.

When should an insurer consider switching to actuarial SaaS for IBNR compliance?

Before portfolio growth strains the current process, ideally. In practice, the right trigger is when reserve cycle preparation time exceeds 30% actuarial capacity, when a regulatory filing has required material manual restatement, or when IFRS 17 disclosure requirements can’t be met without significant rework after the estimation step.

What are the common data risks in manual IBNR reserving?

Manual data transfer from claims systems to run-off triangles is the highest-risk step. Single transposition errors can shift reserve estimates materially. Without automated data validation, there’s no systematic check between source data and the triangle used for estimation. IFRS 17 non-life solutions that connect directly to source systems eliminate this step.

What should insurers look for when evaluating IBNR software solutions?

Audit trail capability, support for multiple estimation methods beyond chain ladder, native IFRS 17 disclosure outputs, direct integration with claims data systems, and a documented implementation path for parallel running during transition. Price should be the last filter, not the first.