TL;DR

Manual ECL modeling risks in spreadsheets undermine your IFRS financial reporting solution and create audit failures that regulators catch during examinations. This guide exposes how banks expose themselves through formula errors, version control failures, and inconsistent probability of default assumptions when lacking a robust IFRS financial reporting solution. Learn why spreadsheet-based IFRS 9 compliance creates systemic control weaknesses, what regulators examine in ECL models, and why enterprise IFRS financial reporting solution reduce risk while improving decision-making. Discover how modern IFRS financial reporting solution enforce consistent methodology and generate automatic audit trails that eliminate spreadsheet-based risks entirely.

IFRS Financial Reporting Solution: Manual ECL Modeling Risks in Spreadsheets and Hidden Audit Failures in IFRS 9 Compliance

Banks face mounting regulatory pressure around expected credit loss calculations. Manual spreadsheet processes create audit failures that regulators catch during inspections. The problem isn’t just about accuracy. It’s about proving your methodology works consistently across thousands of loan portfolios without a robust IFRS financial reporting solution.

Financial institutions worldwide rely on Excel for IFRS 9 compliance. That reliance creates systemic risks that don’t show up until audit season. Formula errors, version control gaps, and inconsistent probability of default assumptions slip through review cycles. Then regulators flag them during examinations.

A comprehensive IFRS financial reporting solution addresses these vulnerabilities by automating calculations, maintaining audit trails, and ensuring consistent application of ECL methodologies across all portfolios.

Why Spreadsheets Fail as an IFRS Financial Reporting Solution

Spreadsheets weren’t designed for probability-weighted ECL calculations across multiple economic scenarios. Banks use them anyway because they seem flexible and familiar. The reality is different. Complex PD multipliers, LGD adjustments, and exposure at default calculations create formula chains that break under manual updates.

As of December 31, 2023, 57% of IFAC member jurisdictions have fully adopted IFRS. That means 79 jurisdictions rely on standards that demand sophisticated impairment modeling. Spreadsheets can’t keep pace with that sophistication at scale.

Banks operate under intense scrutiny. Regulators examine ECL models for transparency and reproducibility. Spreadsheets obscure both. You can’t trace back through six months of manual adjustments to understand why Stage 2 provisions increased. Version control becomes impossible when finance teams share files through email attachments.

Key Risks in Manual IFRS 9 ECL Models

Formula Errors and Broken Links

Copied formulas create silent failures. You adjust a PD table in one worksheet. The LGD calculation two tabs over still references the old range. Nobody notices until the quarter closes and provisions don’t reconcile.

VLOOKUP functions fail when reference tables shift. INDIRECT formulas break when worksheets get renamed. These aren’t theoretical problems. They happen in production ECL models at major financial institutions. Auditors find them during post-implementation reviews.

Version Control and Audit Trail Gaps

Finance teams work in shared drive folders. Someone updates the macro scenarios. Another analyst recalibrates the PD curves. A third person refreshes the EAD inputs. Which version contains the approved assumptions?

Email chains become the audit trail. That doesn’t work when regulators ask about specific staging decisions six months later. You need to prove the model worked correctly at month end. Spreadsheet file properties don’t capture that level of detail.

Manual logs and change documentation help. They still depend on human discipline during month-end close cycles. One missed entry breaks the audit trail. Regulators view that as a control failure.

Inconsistent PD, LGD, and EAD Assumptions

PD calibration requires careful attention to macroeconomic forecasts. Banks typically run three scenarios with different probability weights. Each scenario needs consistent PD curves across all portfolios. Spreadsheet models apply those curves through manual links and references.

One portfolio uses a stale PD table. Another references the updated assumptions. The weighted average ECL calculation combines inconsistent inputs. The provision looks reasonable at the total level. It falls apart under detailed audit review.

LGD adjustments face similar problems. Forward-looking overlays should apply consistently to like exposures. Manual application creates variation that auditors interpret as methodological weakness. That triggers deeper examination of your entire ECL framework.

Weak Scenario Weighting and Overlays

IFRS 9 requires probability-weighted provisions across multiple economic scenarios. Banks typically model base, upside, and downside outcomes. Each scenario gets a probability weight that reflects management’s view of economic conditions.

Spreadsheet models track scenario weights in parameter tables. Someone updates the weights for the current quarter. The calculation formulas still reference last quarter’s assumptions. Weighted ECL provisions use the wrong probabilities for three months.

Qualitative overlays add another layer of complexity. Management adjustments for emerging risks need clear documentation and consistent application. Spreadsheet models hide those adjustments in hardcoded cells that don’t link to supporting documentation.

How Spreadsheet Errors Impact Financial Statements

Misstated Loan Loss Provisions

ECL provisions flow directly to the income statement. A 10 percent error in PD assumptions can shift provisions by millions. Spreadsheet formula failures create exactly those kinds of errors.

Banks provision for expected losses over the life of the loan. Stage 1 uses 12-month ECL. Stages 2 and 3 require lifetime calculations. Manual staging decisions multiplied across thousands of loans create exposure to systematic errors.

One broken formula affects an entire portfolio segment. Corporate loans get Stage 1 treatment when they should migrate to Stage 2. The provision understates expected losses by material amounts. Auditors catch it during year-end fieldwork.

Profit Volatility and Capital Pressure

Unexpected provision increases hit earnings immediately. Management explains the impact to boards and investors. Regulators question whether risk management processes work effectively.

Capital ratios depend on stable, predictable credit loss estimates. Sharp provision swings suggest underlying model weaknesses. Banks operating near regulatory minimums face immediate pressure to strengthen capital positions.

That pressure comes from preventable spreadsheet errors. Better model governance would catch the problems before quarter-end. Manual processes make that governance nearly impossible to maintain.

Regulatory and Audit Findings

Regulators examine ECL models through formal inspections. They sample loan files and test provision calculations. Material errors trigger enforcement actions and remediation requirements.

Public auditors face their own requirements around model validation. They can’t rely on client-built spreadsheets without extensive testing. That testing takes time and increases audit fees. Persistent model issues can lead to qualified opinions.

Governance and Control Challenges

Significant Increase in Credit Risk (SICR) Issues

IFRS 9 requires banks to identify significant increases in credit risk. That determination drives staging decisions. Stage 1 loans use 12-month ECL. Stage 2 requires lifetime provisions.

Spreadsheet models typically use quantitative thresholds for SICR assessment. PD increases above a certain level trigger Stage 2 classification. Manual application of those thresholds introduces inconsistency across portfolios.

Qualitative indicators add complexity. Payment delays, covenant breaches, and credit rating downgrades all signal increased risk. Finance teams apply judgment to assess significance. Spreadsheet models don’t capture that judgment in auditable ways.

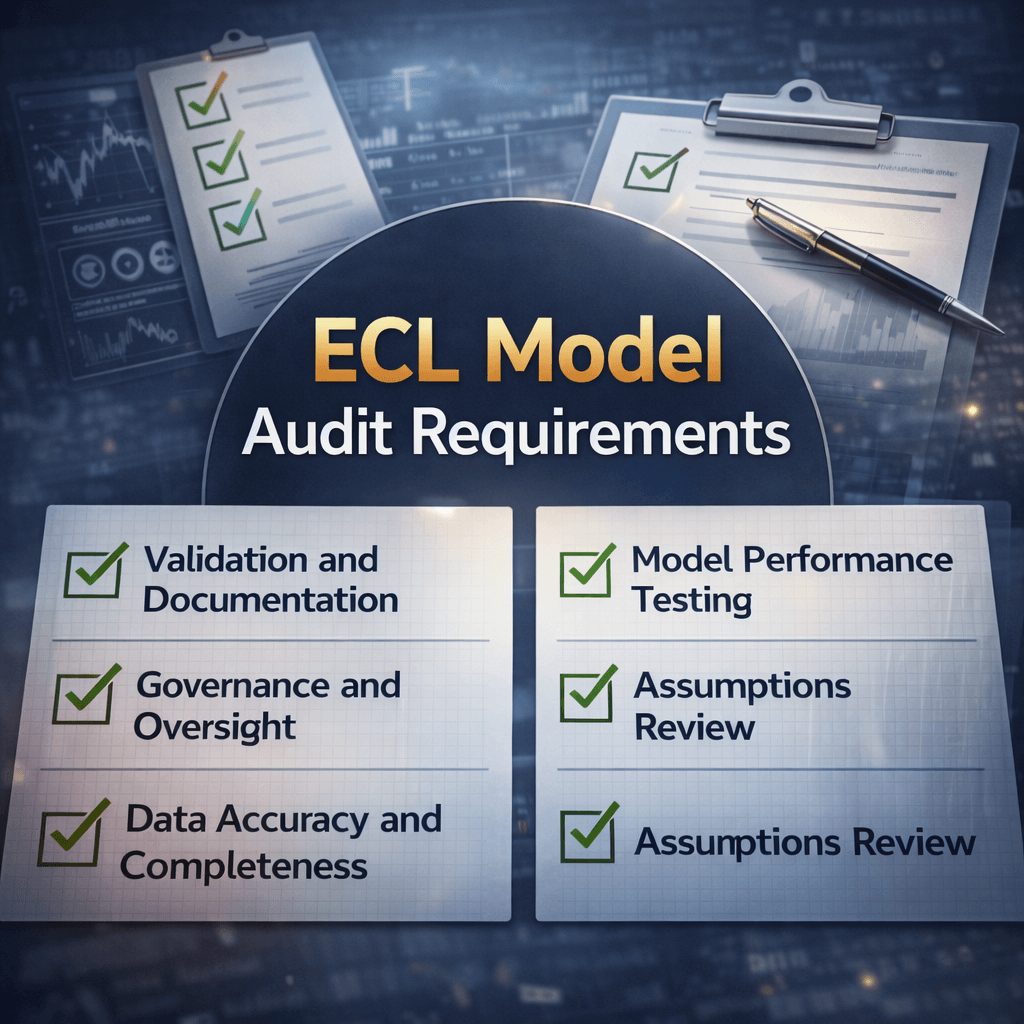

Model Validation and Documentation Gaps

Model validation requires independent review of assumptions, formulas, and calculations. Spreadsheet models resist effective validation. Reviewers can’t easily trace complex formula chains across dozens of worksheets.

Documentation standards for ECL models are strict. Banks need to explain data sources, calibration approaches, and override rationale. Spreadsheet models embed that information in comments, notes, and supporting files. That fragmentation makes comprehensive documentation difficult.

IFRS 9 software solutions provide integrated documentation capabilities that address these challenges.

Third-party validators struggle with spreadsheet-based ECL models. They request source data, calculation logic, and scenario assumptions. Banks respond with file packages that take days to assemble. The validation process becomes a documentation exercise instead of a technical review.

Data Quality and Integration Failures

ECL calculations need current loan data, macroeconomic forecasts, and historical loss experience. Those data sources live in different systems. Spreadsheet models pull information through manual exports and data dumps.

Export timing matters. Month-end loan balances should match the ECL calculation date. Manual processes create timing mismatches when exports run on different schedules. The provision calculation uses stale data without anyone realizing it.

Data transformation introduces additional errors. Raw system exports need cleaning, formatting, and reconciliation. Spreadsheet macros and formulas handle those tasks. Quality checks depend on manual reviews that might not catch every issue.

What Auditors Look for in ECL Models

External auditors examine ECL models for accuracy, completeness, and compliance. They test whether provisions reflect management’s best estimate of expected losses. Spreadsheet models make that testing difficult.

Auditors request model documentation, assumption support, and calculation details. Banks provide spreadsheet files with highlighted cells and annotation notes. That doesn’t meet audit standards for model transparency and control.

Formula logic needs independent verification. Auditors trace calculations from source data through final provisions. Complex spreadsheet formulas with nested functions and circular references resist audit testing. Verification takes extensive time and sampling.

Scenario analysis requires special attention. Auditors test whether probability weights and macroeconomic assumptions align with approved frameworks. Spreadsheet models store those parameters in various locations. Gathering complete documentation becomes a project unto itself.

Spreadsheet vs Automated IFRS Financial Reporting Solution

Purpose-built systems offer clear advantages over spreadsheet approaches. Automated platforms maintain audit trails by design. Every assumption change, staging decision, and provision calculation gets logged with timestamps and user identifiers.

IFRS 9 ECL software eliminates manual version control issues through centralized model management.

System-based solutions integrate directly with core banking platforms. Data pulls happen automatically on scheduled cycles. Timing mismatches and stale data problems disappear. The ECL calculation always uses current loan information.

Formula logic becomes standardized and testable. Development teams build calculation engines with version control and testing protocols. Changes go through formal release processes. That creates confidence that calculations work correctly across all portfolios.

When to Replace Manual ECL Models

Banks should evaluate their ECL model approach when regulatory findings accumulate. Multiple audit comments about documentation or control weaknesses signal systemic problems. Manual processes can’t address those problems through incremental improvements.

Growth in loan portfolios strains spreadsheet capacity. Models that worked for 10,000 loans break down at 50,000. Calculation times increase. Formula complexity makes maintenance impossible. That’s the signal to consider purpose-built solutions.

Regulatory change creates another inflection point. As of December 31, 2023, 40% of IFAC member jurisdictions have partially adopted IFRS. Those jurisdictions will move toward full adoption. Banks operating there need scalable ECL solutions.

Best Practices to Reduce ECL Model Risk

Strong governance starts with documented procedures. Banks should maintain written policies for assumption setting, model override, and scenario selection. Those policies guide finance teams during monthly provision cycles.

Independent model validation provides critical assurance. Validation teams should review calculation logic, test key assumptions, and verify data quality. That validation needs to happen annually at minimum. Material model changes trigger immediate review.

Understanding IFRS 9 requirements helps organizations build stronger validation frameworks.

Change control procedures prevent unauthorized modifications. ECL models should operate in restricted environments with access logging. Version control tracks all changes with approval documentation. Month-end calculations use formally released model versions.

Regular testing identifies calculation errors before quarter close. Finance teams should reconcile provisions across multiple dimensions. Compare current period to prior period. Test scenario sensitivity. Validate staging decisions for major exposures.

Frequently Asked Questions

What are the biggest risks in Excel-based ECL models?

Formula errors create the most immediate risk. Broken links, incorrect references, and copy-paste mistakes generate wrong provisions. Those errors often go undetected until audit review.

Version control presents ongoing challenges. Multiple analysts working in shared files create conflicts and overwrites. The approved model version becomes unclear.

Documentation gaps undermine audit defense. Spreadsheet models lack built-in trails for assumption changes and override rationale. That makes regulatory examination difficult.

Can spreadsheets meet IFRS 9 compliance requirements?

Spreadsheets can technically perform ECL calculations. The question is whether they support sustainable compliance at scale. Small portfolios with simple structures might work in spreadsheet environments.

Large banks with diverse loan books face serious limitations. Manual processes can’t maintain the control rigor that regulators expect. Audit trails, version management, and documentation standards require system-level capabilities.

Partial compliance isn’t acceptable. Regulators evaluate the entire ECL framework holistically. Weaknesses in governance, validation, or documentation offset calculation accuracy.

How do banks strengthen ECL model governance?

Written policies establish baseline standards. Documentation requirements, validation frequency, and change approval processes need formal definition. Those policies guide daily operations and audit responses.

Independent validation provides external perspective. Validation teams should include technical specialists who understand ECL methodology. Their reviews catch issues that internal teams might miss.

Technology investment reduces manual risk. Purpose-built platforms offer control capabilities that spreadsheets lack. Banks should evaluate those solutions when governance weaknesses persist despite process improvements.

Moving Toward Automated IFRS Financial Reporting Solution

Manual ECL modeling exposes banks to preventable audit failures and regulatory findings. Spreadsheet limitations around version control, formula accuracy, and documentation create systemic weaknesses. Those weaknesses show up during external audits and regulatory inspections.

Strong governance reduces but doesn’t eliminate spreadsheet risks. Banks operating at scale need purpose-built solutions that maintain audit trails and automate complex calculations. The transition from manual to automated IFRS financial reporting solution requires planning and investment. It also provides immediate improvements in control quality and audit efficiency.

Prima Consulting helps financial institutions strengthen their IFRS 9 compliance frameworks through tailored IFRS financial reporting solution. Our team brings deep expertise in ECL methodology, model validation, and regulatory requirements. Contact us to discuss how we can support your credit loss modeling initiatives.