TL;DR

Finding and classifying lease contracts scattered across your organization is the biggest barrier to successful IFRS 16 software compliance. Most finance teams discover this painful truth when they realize lease agreements hide in procurement systems, real estate files, vendor portals, and spreadsheets nobody knew existed. This article walks you through identifying where lease data actually lives, the classification challenges you’ll face with embedded leases and renewal options, and how to prevent common data extraction mistakes. Learn why incomplete lease inventories and spreadsheet errors derail most implementations. Start building a systematic approach to locate, classify, and manage your complete lease population before your audit begins.

IFRS 16 Transition Headaches: Data Extraction and Classification for IFRS 16 Software Solutions

Finding and classifying every lease contract across your organization is the biggest barrier to successful IFRS 16 compliance.

Most finance teams discover this painful truth six months into their transition when they realize lease agreements hide in procurement systems, real estate files, vendor portals, and spreadsheets nobody knew existed.

The work of extracting lease data and determining which contracts qualify for exemptions isn’t just tedious. It’s where most IFRS 16 projects falter, miss deadlines, and discover critical compliance gaps during the audit phase.

This article walks you through the exact challenges your team will face, where lease data actually lives, how to identify embedded leases, and why IFRS 16 software solutions change the entire equation.

Why IFRS 16 Transitions Fail Without the Right Data

The IFRS 16 standard requires organizations to recognize nearly all leases as right-of-use assets and lease liabilities on the balance sheet. This fundamental change means every lease contract your company holds needs identification, extraction, classification, and calculation. The process sounds straightforward until you start looking.

Here’s what actually happens: You create a centralized lease team. You send emails asking departments to submit lease agreements. The responses trickle in with some complete, some partial, and many lost entirely. Finance finds leases in vendor payment records that procurement never documented.

Real estate discovers vehicle leases buried in fleet management systems. Marketing uncovers equipment leases signed years ago by people who’ve since left the company.

One mid-market manufacturing firm discovered they were managing 340 lease agreements. Their initial inventory showed 210 contracts. The gap of 130 missing leases only emerged after they systematically searched procurement files, accounting records, and vendor agreements. Those missing contracts represented millions in unrecognized liabilities.

In 2024, over 50% of Chartered Accountants reported a mcc moderate to very significant impact from adopting IFRS 16. That impact directly correlates with data extraction challenges. When companies lack complete lease populations, impact assessments fail. Comparative reporting becomes unreliable.

Audit findings multiply. Many finance teams have found that using IFRS 16 software helps them address these data extraction problems faster and more reliably than traditional spreadsheet approaches.

What Lease Data Is Required Under IFRS 16?

Before your team can classify and calculate anything, you need specific information from each lease contract. Missing even one field creates problems downstream. Understanding your data requirements is crucial whether you manage information manually or select IFRS 16 software solutions to assist you.

Identifying Complete and Accurate Lease Populations

The first step involves determining your complete lease population. This means every contract where your organization controls the right to use an identified asset for a period in exchange for consideration. That definition casts a wide net.

You need property leases covering real estate locations: office buildings, warehouses, retail spaces, parking facilities. You need equipment leases for machinery, computers, vehicles, furniture. You need embedded leases within service contracts like the transportation component embedded in a waste collection service agreement.

Your lease population must include sale-leaseback arrangements, subleases where your company acts as lessor, and leases you haven’t previously recognized because they fell below materiality thresholds under the old IAS 17 standard. To properly understand how these categories interact, you may want to review IFRS 16 Lease Accounting Basics on Prima Consulting’s site.

Key Data Fields for IFRS 16 Compliance

Each lease contract requires extraction of critical information. The lease commencement date establishes when your company obtains the right to use the asset. The lease term determines the calculation period. When you’re uncertain whether renewal options are reasonably certain to be exercised, the lease term shrinks considerably, affecting both the right-of-use asset and lease liability calculations.

Your team needs all lease payments: base rent, contingent payments, amounts paid directly to third parties, and variable payments linked to indices or rates. You need the interest rate implicit in the lease when it’s readily determinable. When it’s not, you need your incremental borrowing rate—the rate you’d pay to borrow funds over a similar term for a similar amount.

Additional critical fields include initial direct costs like commissions paid to brokers, estimated restoration costs when the lease requires asset restoration, and any purchase options, termination options, or other contract terms affecting lease classification.

Organizations managing hundreds of leases typically find that specialized IFRS 16 software solutions for managing these data fields prevent errors that spreadsheets frequently introduce.

Where Lease Data Hides Inside Organizations

Finance teams consistently underestimate how scattered lease information becomes across the enterprise. Knowing where to look determines whether you find 80 percent or 20 percent of your actual lease portfolio. This is why IFRS 16 software with systematic data discovery capabilities helps organizations locate leases they might otherwise miss.

Contracts, ERP Systems, and Spreadsheets

Your enterprise resource planning system holds lease data, but often not in a dedicated lease module. Accounting records show rental expense but may lack lease term details. Spreadsheets maintained by individual departments contain historical lease information in inconsistent formats with varying completeness.

Procurement systems record vendor agreements and purchase orders. Many equipment leases begin as purchase orders or vendor contracts that finance teams never categorized as leases. Marketing and operations maintain their own vendor files with signed agreements that accounting departments never received.

Real estate teams typically manage property leases in standalone systems. Those databases contain rich lease data but operate independently from accounting records. If real estate and finance don’t coordinate during IFRS 16 implementation, property lease data gets duplicated, contradicts accounting records, or gets overlooked entirely. This fragmentation is exactly what IFRS 16 software helps resolve by consolidating data from multiple sources.

Procurement, Real Estate, and Asset Systems

Your procurement department knows about leases structured as service agreements. A maintenance contract for HVAC systems might include the right to use the equipment for five years. That’s an embedded lease requiring separate accounting treatment.

The real estate department tracks all property leases. They understand lease terms better than anyone because they negotiate renewals and handle modifications. Their systems contain complete payment schedules, escalation clauses, and renewal options that accounting has never seen.

Your fixed asset systems hold information about capitalized lease payments. These systems show what’s already been capitalized but may contain different lease term assumptions than the actual contracts specify. Vendor portals where you access lease documentation online often contain the most current contract information, yet many organizations don’t know these portals exist.

Email archives hold signed lease agreements. Someone’s inbox contains PDF files of every contract ever executed. Finding that person, accessing those files, and extracting contract information from casual email storage requires persistence most organizations underestimate.

Lease Identification and Classification Challenges

Once you’ve physically located lease contracts, you face analytical challenges that spreadsheets can’t reliably solve. Understanding these challenges upfront prevents errors later. Many organizations turn to IFRS 16 software when managing classifications across diverse asset types and contract structures.

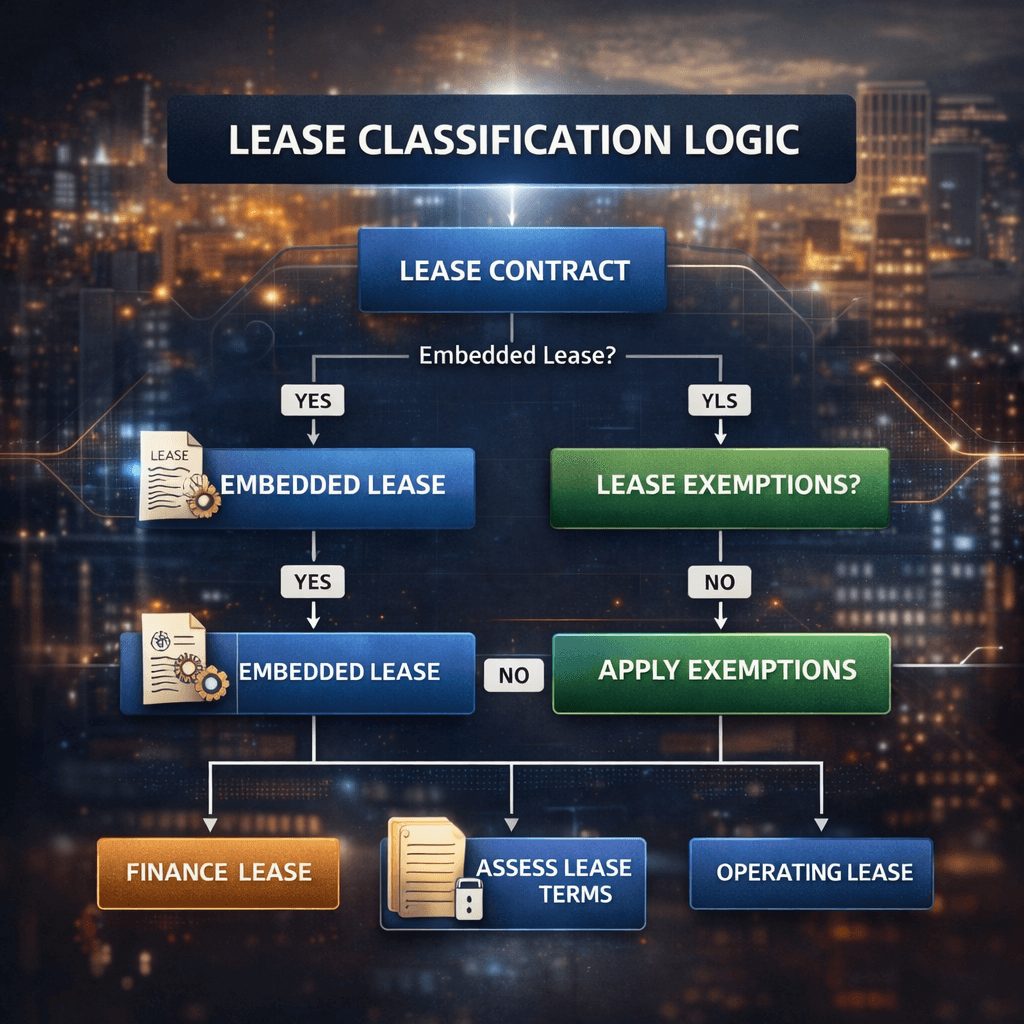

Identifying Embedded Leases

Embedded leases exist within larger service contracts. Your organization signs a facility management agreement covering building maintenance, cleaning, grounds keeping, and security. The contract includes the right to use the building for the term. That’s an embedded lease requiring separate accounting treatment.

These embedded leases are easy to miss because they’re literally embedded inside contracts that have nothing to do with leases. A waste collection service agreement includes the right to have waste collected from a specific facility on a set schedule. That collection service contains a lease component: the right to use the collection vehicle and disposal facilities.

The tricky part involves determining where the lease component ends and the non-lease service component begins. The IFRS 16 standard requires separation when lease and non-lease components are separately identified in the contract and you can measure the standalone price of each component.

Most organizations lack the systems and processes to systematically identify embedded leases. They find some after auditors point them out. They miss others entirely because nobody conducted a systematic search across service contracts.

Separating Lease and Non-Lease Components

When you identify an embedded lease, you must separate the lease payments from service payments. That’s straightforward when contracts separately price lease and non-lease components. Many contracts don’t. You face judgment calls about allocating a single blended payment between the lease component and the service component.

A facility management agreement specifies $10,000 monthly. That payment covers all building management services including HVAC maintenance, building security, grounds keeping, cleaning, and the right to occupy the space. IFRS 16 requires you to determine how much of that $10,000 relates to your lease right versus facility services.

You might reasonably conclude that 60 percent relates to the space lease and 40 percent to services. Different people might reasonably reach different conclusions. That judgment directly affects your right-of-use asset and lease liability calculations.

Determining Lease Term and Renewal Options

The lease term includes the non-cancellable period plus any renewal periods you’re reasonably certain to exercise. That word “reasonably” creates classification uncertainty throughout your lease portfolio.

Your company signs a five-year equipment lease with two one-year renewal options. Are you reasonably certain to exercise those options? The question requires analyzing your historical renewal patterns, the nature of the equipment, the cost of replacement, and the operational importance of maintaining equipment access.

Many organizations struggle with this judgment. Some automatically assume all options will be exercised. Others automatically exclude all options. Neither approach matches the IFRS 16 requirement to assess genuine business circumstances. IFRS 16 software can help model different renewal scenarios to support your judgments.

Variable lease payments create similar classification challenges. Your lease requires $5,000 monthly base rent plus additional rent equal to 3 percent of building sales exceeding $2 million annually. Do you include that contingent payment in your initial lease liability measurement?

The standard requires excluding contingent payments from the lease liability and instead recognizing them as expenses when the contingency occurs. That’s straightforward conceptually but requires systems to track conditional payments separately from base payments.

For guidance on managing complex modifications after initial recognition, consider reviewing IFRS 16 lease modification accounting resources.

Common IFRS 16 Data Extraction Mistakes

Most organizations repeat the same errors when implementing IFRS 16. Understanding these mistakes helps you avoid them. These are exactly the kinds of errors that IFRS 16 software was designed to prevent through automation and validation controls.

Incomplete Lease Inventories

The biggest error involves incomplete lease identification. Organizations complete IFRS 16 implementation believing they’ve found all leases. Six months later, auditors identify lease agreements they missed. Comparative reporting becomes unreliable. Restatements become necessary.

This happens because organizations don’t systematically search all potential lease sources. They rely on voluntary submissions from departments, missing leases in vendor portals, email archives, and systems they didn’t know existed. They underestimate how scattered lease information becomes across enterprises.

Preventing this requires documenting every location where lease agreements could exist. That means checking procurement systems, reviewing vendor agreements, searching email archives, accessing real estate management systems, examining asset registries, and interviewing department heads about historical lease obligations.

Inconsistent Assumptions Across Entities

Multi-entity organizations face judgment consistency challenges. Your U.S. subsidiary assumes all renewal options will be exercised. Your European subsidiary excludes most renewal options. Your Asia-Pacific region uses a middle-ground approach.

That inconsistency creates audit risk and comparability problems. IFRS 16 requires consistent application of judgments across the organization. When different entities reach different conclusions about lease terms, renewal options, or embedded lease identification, financial statements lack the transparency the standard demands.

Preventing this requires documenting lease judgment policies before implementation. Your organization should determine standard approaches to lease term assessment, renewal option evaluation, and embedded lease identification. Individual entities apply those standards consistently unless specific circumstances genuinely warrant different conclusions.

Over-Reliance on Manual Spreadsheets

Many organizations build extensive spreadsheets to track lease calculations. Individual contributors maintain spreadsheets, make formula errors, manually update calculations, and create version control nightmares. Someone forgets to update the master spreadsheet when a lease modifies. Another person makes a formula error that nobody catches until audit.

Spreadsheets aren’t inherently bad. They’re essential for smaller portfolios. But as lease portfolios grow beyond 50 to 100 contracts, spreadsheet errors become inevitable. You can’t scale manual calculations across 500 leases without formula mistakes, missing updates, and version confusion. This is when most organizations recognize they need IFRS 16 software to scale their data management.

How IFRS 16 Software Simplifies Data Collection

The right approach to lease data collection and classification involves technology that can handle the complexity without introducing new errors. Many organizations find that implementing IFRS 16 software designed specifically for lease accounting eliminates entire categories of problems.

Centralized Lease Repositories

A centralized lease repository replaces scattered spreadsheets and fragmented systems. Your organization inputs lease data once into the IFRS 16 software. Finance accesses current information from that central location. Real estate updates lease terms in the same IFRS 16 software. When finance needs to modify assumptions, those changes appear immediately everywhere.

That centralized approach within IFRS 16 software eliminates version control problems. Everyone works from the same lease data through the platform. When someone updates a lease payment schedule in IFRS 16 software, that change propagates to all calculations automatically. When lease modifications occur, the IFRS 16 software updates the relevant lease without requiring manual spreadsheet changes across multiple files.

Centralized repositories in IFRS 16 software also enable validation. The system enforces data completeness. You can’t save a lease record in IFRS 16 software without entering required fields. Validation rules flag impossible dates, negative payment amounts, and other data errors before they propagate through calculations.

Automated Data Validation and Controls

The best IFRS 16 software includes automated validation that catches data errors before they affect calculations. Your IFRS 16 software validates that lease commencement dates precede lease termination dates. It validates that lease payment frequencies match the contract. It flags unusual interest rates that might indicate data entry errors.

Automated controls in IFRS 16 software also track lease modifications. When payment amounts change, the system flags that modification and requires documentation of the change authorization. When lease terms extend, the IFRS 16 software highlights that modification and recalculates the lease liability automatically.

That automation within IFRS 16 software reduces the manual effort while improving data quality. Finance teams spend time analyzing lease data rather than hunting formula errors.

Transition Approaches and Data Readiness

Your organization must choose between full retrospective and modified retrospective application of IFRS 16. That choice affects how much historical lease data you need and your implementation timeline for IFRS 16 software.

Full Retrospective vs Modified Retrospective

Full retrospective application requires restating all prior year comparatives as though IFRS 16 applied since inception. That requires extracting lease data from historical periods, estimating lease terms from contracts that may have already concluded, and determining what renewal options were in place historically.

Modified retrospective application allows using practical expedients. You can use a single discount rate across all similar leases rather than determining each lease’s specific incremental borrowing rate. You can use hindsight in determining lease terms rather than assessing what was reasonably certain at lease commencement.

Full retrospective provides more complete financial information but requires extensive historical data extraction and IFRS 16 software sophistication. Modified retrospective simplifies implementation but provides less comparative transparency.

Data Gaps That Delay IFRS 16 Adoption

Organizations implementing IFRS 16 consistently discover data gaps when they attempt calculations. Lease contracts sometimes lack information about interest rates, making it impossible to calculate appropriate lease liabilities without estimation. Equipment leases sometimes omit residual value guarantees that affect classification.

Those data gaps force estimation or delay implementation. When your lease contract doesn’t specify the implicit interest rate, you must determine your incremental borrowing rate. That’s a judgment requiring analysis. When contracts lack clear renewal option language, you must contact lessors to clarify terms.

Building time into your IFRS 16 project for data clarification prevents surprises during the audit phase. Set aside budget and resources to contact lessors, clarify ambiguous contract language, and estimate missing data.

Audit, Controls, and Ongoing Compliance Risks

IFRS 16 compliance extends beyond implementation. Auditors scrutinize lease accounting controls to ensure ongoing accuracy. Having robust IFRS 16 software controls in place strengthens your audit position significantly.

Audit Trail and Documentation Requirements

The challenge of maintaining complete audit trails becomes manageable when you implement robust IFRS 16 compliance software designed specifically for lease accounting.

Quality IFRS 16 compliance software maintains automatic documentation of every classification decision, calculation assumption, and modification you make. Rather than digging through spreadsheets and email chains to reconstruct how you arrived at a number, your auditors can drill into the system and see exactly what input values you used, when you made changes, and who authorized modifications.

This complete audit trail within IFRS 16 compliance software transforms what would normally be a stressful audit process into a straightforward verification of your controls and methodology. When you can show auditors that your lease accounting process followed consistent, documented rules across your entire portfolio, audit findings drop dramatically and the process accelerates.

Maintaining Data Accuracy Post-Transition

Ongoing compliance requires more than just accurate data. You need visibility into your lease position at any point in time, which is where a quality IFRS 16 reporting platform becomes essential. An IFRS 16 reporting platform that integrates with your lease data repository allows you to generate required disclosures immediately whenever you need them.

Rather than assembling information from multiple sources and manually building note disclosures, your IFRS 16 reporting platform pulls directly from your centralized lease database and generates audit-ready disclosures in minutes. The platform tracks opening balances, additions, modifications, payments, interest accretion, depreciation, and closing balances automatically.

When the IASB issues guidance updates or your auditors ask specific questions about your lease population, your IFRS 16 reporting platform delivers answers in real time rather than requiring days of manual analysis.

How IFRS 16 software supports year-round compliance with structured timelines and audit-ready controls.

Best Practices for a Smooth IFRS 16 Transition

Organizations that successfully implement IFRS 16 follow consistent practices that prevent common errors and ensure completeness.

Cross-Functional Data Ownership

Successful transitions involve collaboration across finance, real estate, procurement, operations, and treasury. Each department owns lease data relevant to their function. Real estate owns property leases. Procurement owns equipment leases. Finance coordinates data collection and ensures completeness.

That cross-functional approach prevents silos. It ensures that someone owns responsibility for finding leases in every system. It creates accountability. Each department knows what information they must provide and when.

Matching Your Approach to Portfolio Size

As portfolio sizes grow, manual processes break down. Spreadsheets become unwieldy. Formula errors multiply. Version control becomes impossible. Scaling beyond 100 to 200 leases requires moving beyond spreadsheets.

The transition from manual processes to technology-enabled approaches happens at different scales for different organizations. Some organizations need comprehensive solutions for managing thousands of leases globally. Others need simpler approaches for smaller portfolios that might grow over time.

What matters is matching your approach to your portfolio size while building capacity to scale. Starting with approaches that work for current lease populations but won’t scale as you add leases creates problems. Building systems capable of handling future growth from day one requires slightly more upfront investment but prevents rework as your portfolio expands.

Finance teams interested in professional guidance on navigating these decisions can explore IFRS 16 advisory services available through Prima Consulting.

Summary and Recommended Next Steps

IFRS 16 implementation success depends fundamentally on finding, classifying, and maintaining accurate lease data. The data extraction phase determines whether you’ll achieve clean audit findings or spend the audit answering questions about leases you missed.

Your organization should begin by systematically identifying all locations where lease agreements exist. That means ERP systems, procurement databases, real estate management systems, vendor portals, email archives, and department files. You should document lease judgment policies before implementation to ensure consistent classification across all entities. You should evaluate whether manual spreadsheet processes will scale to your lease portfolio size or whether more sophisticated approaches will prevent formula errors and version control problems.

The finance teams that execute these steps most rigorously complete IFRS 16 transitions with the fewest audit findings, the cleanest implementations, and the most reliable ongoing compliance. The teams that skip these steps discover problems late: during testing, during audit fieldwork, or worse, after financial statements issue and corrections become necessary.

Invest upfront in comprehensive lease identification and appropriate data management. That investment pays dividends through audit phases and throughout your organization’s ongoing IFRS 16 compliance lifecycle.

Frequently Asked Questions

What is the difference between a lease and an embedded lease?

A lease is a contract granting the right to control an identified asset. An embedded lease is a lease component within a larger contract: like the right to use space within a facility management agreement. You must identify and separate embedded leases from the service components within those same contracts.

How do I determine my incremental borrowing rate if my lease contract doesn’t specify an implicit interest rate?

Your incremental borrowing rate is the rate you’d pay to borrow funds over the lease term for a similar amount. Consider your credit rating, debt levels, collateral value, and prevailing market rates. Different entities might have different incremental borrowing rates. Different lease terms might warrant different rates based on security, term length, and market conditions.

Can I exclude renewal options from my lease term assessment?

Only if renewal is not reasonably certain. If facts and circumstances indicate you’ll likely exercise renewals because the equipment is critical, replacement costs are high, or historical patterns show you renew similar leases, you must include those renewal periods in your lease term.

What happens if I discover a lease after I’ve completed my IFRS 16 implementation?

You must recognize the lease, calculate its right-of-use asset and lease liability, and adjust comparative periods if you used full retrospective application. If you used modified retrospective, you adjust the current period. Either way, you must update your lease population and establish processes to prevent missing leases in the future.

How detailed do my lease data records need to be for audit purposes?

Auditors require sufficient detail to verify calculations. That means storing lease commencement dates, lease terms, payment amounts, payment schedules, interest rates used, initial direct costs, any modifications, and the classification methodology you applied. Supporting contracts should be accessible and cross-referenced to your lease records.

Are variable lease payments automatically excluded from lease liability calculations?

Only contingent payments are excluded initially. Payments based on indices or rates (like lease payments tied to inflation) are included in the lease liability using the index or rate at lease commencement. Truly contingent payments (those depending on future events like sales thresholds) are excluded from the lease liability.

What lease data should I prioritize first if I have limited extraction resources?

Start with property leases because they typically involve larger values and have longer terms. Move to equipment leases next. Address embedded leases in service contracts last if resources are constrained. Documenting your prioritization approach helps auditors understand your implementation methodology.

How often should I update my lease data after initial IFRS 16 implementation?

At minimum, quarterly when you perform financial close procedures. New leases should be captured immediately upon signing. Lease modifications should trigger data updates within the period they occur. Consider more frequent updates (monthly) if your organization signs leases regularly or experiences frequent modifications.

Should I track lease data separately by entity or consolidate at the corporate level?

Track at the entity level where the lease legally exists. Consolidate to the corporate level for financial reporting. This approach allows entity-level audit trails while providing consolidated visibility to corporate finance. Entity-level tracking also supports intercompany lease accounting when one entity leases to another.

What documentation should I maintain to prove my embedded lease identification process?

Document your criteria for identifying embedded leases. Show how you evaluated contracts. Maintain a listing of contracts reviewed with your conclusions on whether embedded leases existed. Keep sample contracts showing your separation of lease and non-lease components. Document your assumptions about standalone pricing when you couldn’t directly observe it.