TL;DR

Finance teams choosing between pension actuarial valuation software and traditional consultants face different tradeoffs. Software-led processes deliver speed, consistency, and direct control—you get results in minutes instead of weeks. Consultants provide professional judgment but introduce delays and recurring costs with each valuation cycle. The best fit depends on your valuation frequency, internal capabilities, data quality, and multi-entity complexity. Organizations running quarterly calculations or managing multiple pension plans typically see clear financial benefits from automation. Prima Consulting helps you evaluate both paths and implement solutions that match your specific situation, budget constraints, and timeline requirements.

Finance teams face a choice when handling pension obligations. You can rely on traditional consultants or adopt pension actuarial valuation software. Each path offers distinct advantages and challenges.

The global pension administration software market reached USD 4.93 billion in 2025. Organizations worldwide recognize the value of automated systems for employee benefit calculations.

This article compares both approaches. You’ll see how software-led processes differ from consultant-dependent methods in accuracy, speed, cost, and control.

What Is Pension Actuarial Valuation Software?

Pension actuarial valuation software automates the calculation of defined benefit obligations. The system processes employee data, applies actuarial assumptions, and generates compliant reports.

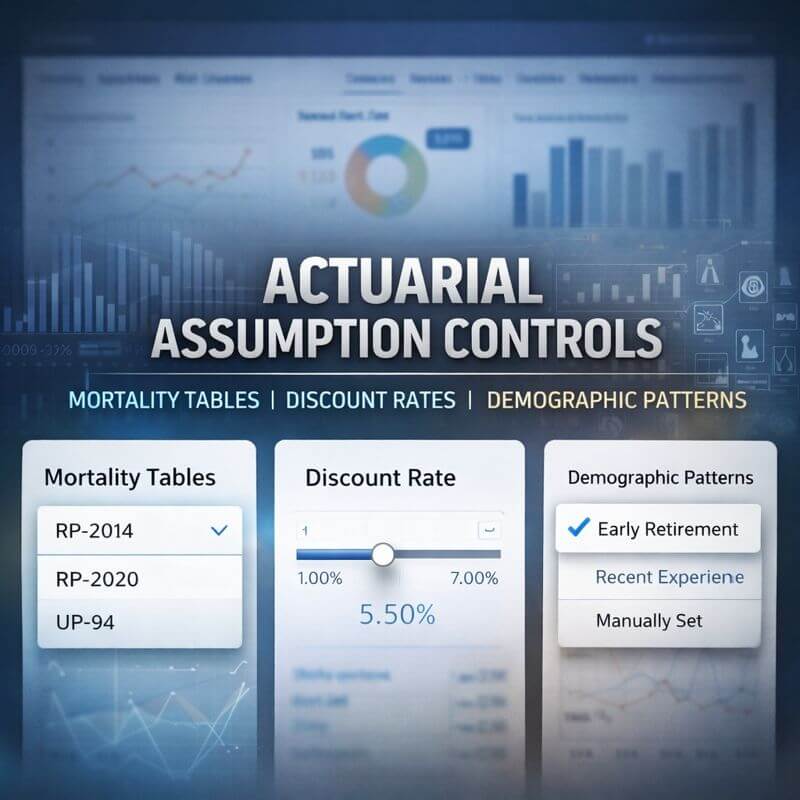

The software connects directly to HR systems. Data flows automatically without manual entry. Built-in algorithms apply mortality tables, discount rates, and salary growth projections based on demographic analysis.

Most systems include features like scenario testing, sensitivity analysis, and automated disclosure notes. You can adjust assumptions and rerun calculations instantly. Reports generate in formats ready for financial statements and audit review.

IAS 19 actuarial valuation software specifically addresses international financial reporting standards. These platforms build compliance into every calculation step.

How Automated Pension Actuarial Valuation Software Works

The automation process starts with data extraction. Software pulls employee information from your HR platform through secure connections. Demographics, service history, salary data, and benefit provisions transfer automatically.

Next comes assumption application. The system analyzes workforce characteristics and applies appropriate actuarial assumptions. This includes mortality rates, turnover patterns, retirement ages, and economic factors.

Calculation engines process this data using actuarial formulas. Defined benefit obligations, service costs, and interest costs calculate in minutes. The software tracks each employee’s benefit accrual and projects future liabilities.

Report generation happens last. The system produces signed valuation reports, disclosure notes, and supporting schedules. Everything exports in formats compatible with accounting systems.

You can run unlimited scenarios. Change the discount rate, adjust salary growth assumptions, or modify retirement patterns. Each iteration produces complete documentation without starting over.

Traditional Consultant-Led Actuarial Valuations Explained

Traditional consultants handle pension valuations through manual processes. Your team extracts data from HR systems and sends it to the actuarial firm.

Consultants receive the data and begin analysis. They apply professional judgment to demographic assumptions and economic factors. Calculations happen using proprietary models and actuarial software.

The process typically takes 15 to 30 days. Consultants must review data quality, make assumption decisions, run calculations, and prepare reports. Any errors in data require additional cycles of correction and recalculation.

Communication happens through emails and calls. If you need to test different assumptions, consultants must rerun their models. Each iteration extends the timeline and increases costs.

Final deliverables include valuation reports, disclosure notes, and assumption documentation. These arrive as completed documents ready for financial statement integration.

Automated vs Traditional Actuarial Valuation: Key Differences

Accuracy, Consistency, and Error Reduction

Automated systems eliminate data transcription errors. Information flows directly from source systems without manual handling. This reduces mistakes from copying data between spreadsheets.

Software applies assumptions consistently across all calculations. Once you set demographic patterns or economic factors, the system uses identical logic for every employee. Manual processes can introduce variation in how consultants apply assumptions.

Validation rules catch data issues immediately. The software flags incomplete records or questionable values before calculations start. Traditional methods might not identify problems until consultants begin their review.

That said, professional actuaries bring expertise to assumption selection. Consultants consider industry trends, economic forecasts, and plan-specific factors. Software provides consistency but may lack the nuanced judgment experienced actuaries offer.

Speed, Reporting Timelines, and Audit Readiness

Pension actuarial valuation software generates results in minutes. You upload data, review assumptions, and receive signed reports the same day. This speed compresses financial close cycles from weeks to days.

Traditional consultants need 15 to 30 business days for standard valuations. The timeline includes data review, calculation processing, report preparation, and quality checks. Rush services cost extra and still require several days.

Scenario testing illustrates the speed difference clearly. Software lets you test five discount rate scenarios in an hour. Consultants might need several days to process the same requests.

Audit trail documentation also differs. Automated systems maintain complete records of all assumptions, calculations, and changes. Auditors can review the entire process through built-in documentation. Consultant reports provide final results but may not include the same level of calculation detail.

Cost Structure and Long-Term Scalability

Software typically involves annual subscription fees. You pay based on plan size, employee count, or entity volume. Initial costs include implementation and HR system integration.

Consulting fees accumulate per valuation. Each year-end calculation, interim update, or assumption change generates new invoices. Large organizations with multiple plans or frequent valuations see significant annual expenses.

The crossover point depends on valuation frequency. Organizations running quarterly or monthly valuations benefit from software economics. Those with annual valuations only might find consulting fees comparable to software costs.

Scalability favors automated systems. Adding entities, plans, or employees typically costs less than proportional consultant fee increases. Software handles volume growth without linear cost expansion.

Data Security, Controls, and Governance

Automated pension actuarial valuation platforms maintain enterprise-grade security. Data encryption protects information during transmission and storage. Access controls limit who can view sensitive employee records.

Organizations retain direct control over their data. Files stay within company systems or approved cloud environments. You decide who accesses calculations and when reports generate.

Traditional consulting relationships involve data sharing. Employee information transfers to external firms through secure channels. While consultants maintain professional standards, data leaves your direct control during the valuation period.

Compliance documentation also differs. Software generates complete audit trails automatically. Every assumption change, calculation run, and report modification gets logged. Consultants provide documentation but you rely on their internal processes.

IAS 19 Valuation Requirements for Pension Plans

IAS 19 establishes accounting standards for employee benefits. Organizations must measure defined benefit obligations using specific actuarial techniques. This includes applying appropriate discount rates based on high-quality corporate bonds.

The standard requires detailed disclosure notes. Financial statements must show plan assets, benefit obligations, expense components, and assumption sensitivity. Changes in actuarial assumptions must be tracked through other comprehensive income OCI vs P&L classifications.

Actuarial valuations must happen at each reporting date. This means annual calculations at minimum for year-end financials. Organizations with interim reporting need more frequent valuations.

Qualified actuaries must certify the calculations. Reports need professional signatures confirming the methodology and results meet accounting standards.

How Software Supports IAS 19 Compliance

Best pension valuation tools build IAS 19 software requirements into their calculation engines. The software applies correct discount rate methodologies based on reporting jurisdiction. OCI and P&L components calculate automatically according to standard requirements.

Disclosure note generation happens through built-in templates. The system produces all required schedules showing obligation movements, expense components, and assumption impacts. You don’t need to manually prepare these disclosures.

Assumption documentation maintains audit-ready records. The software tracks which mortality tables, economic factors, and demographic patterns applied to each calculation. This supports the actuarial certification process.

Multi-entity reporting consolidates results across subsidiaries. Organizations can run valuations for multiple legal entities and roll up results for group reporting.

Risks of Manual IAS 19 Valuation Processes

Manual IAS 19 valuation risks become apparent when organizations rely solely on traditional processes. Waiting weeks for consultant deliverables delays financial close. This becomes critical during tight reporting deadlines.

Assumption changes require complete recalculation cycles. If auditors question a discount rate or mortality assumption, consultants must reprocess the entire valuation. This extends close timelines further.

Documentation gaps sometimes emerge. Consultants provide final reports but supporting calculation details may not include every intermediate step. Auditors requesting additional detail can face delays while consultants prepare supplementary documentation.

Version control gets complicated. Multiple assumption scenarios generate separate report sets. Tracking which version uses which assumptions requires careful file management.

When Does Pension Valuation Software Make Sense?

Software works best for organizations with specific characteristics. Frequent valuations justify the investment. If you run quarterly calculations or test multiple scenarios regularly, automation delivers clear value.

In-house capability matters. Your team needs basic actuarial knowledge to set assumptions appropriately. Software provides calculation power but requires informed users making assumption decisions.

System integration capability influences success. Organizations with modern HR platforms and good IT support implement software more easily. Legacy systems or limited technical resources complicate deployment.

Data quality plays a role. Clean, complete employee records feed automated calculations smoothly. Organizations with data quality issues should address these before implementing software.

Best Fit for Large and Multi-Entity Pension Schemes

Large pension schemes benefit significantly from automation. Plans covering thousands of employees generate calculation complexity that software handles efficiently. Manual processing becomes impractical at scale.

Multi-entity organizations face coordination challenges with consultants. Different subsidiaries need synchronized valuations for group reporting. Software centralizes this process and maintains consistent methodologies across entities.

Organizations operating globally need IAS 19 software for multi-entity reporting. International groups must comply with various local standards while maintaining group-level consistency. Automated systems handle these requirements through built-in compliance frameworks.

Frequent assumption testing suits software capabilities. Large schemes regularly model different scenarios for planning purposes. Software makes this analysis practical where consultant costs would be prohibitive.

Hybrid Models: Software Plus Actuarial Oversight

Many organizations combine automation with professional support. They implement pension actuarial valuation software for routine calculations while retaining consultants for assumption review and special analyses.

This hybrid approach offers advantages. Software handles standard quarterly or monthly valuations. Consultants review annual assumption changes, conduct experience studies, and provide regulatory guidance.

Costs balance between extremes. You pay subscription fees for software but reduce consultant engagement to advisory services. This often costs less than full outsourcing while maintaining professional oversight.

Risk management improves through dual validation. Internal calculations run through software while external actuaries verify methodology and assumption appropriateness. This provides additional comfort for audit purposes.

Key Features to Look for in Pension Actuarial Software

Assumption management matters most. The software should let you set mortality tables, economic assumptions, and demographic patterns with flexibility. Look for systems allowing plan-specific customization rather than rigid default assumptions.

HR system integration capabilities determine ease of use. Direct connections to major enterprise HR platforms eliminate manual data handling. Verify the software supports your specific HR technology before committing.

Reporting flexibility affects usability. You need systems generating standard disclosure notes but also allowing custom report formats. Financial statement integration requires outputs matching your accounting system requirements.

Security features protect sensitive employee data. Look for encryption during data transmission and storage. Access controls should let you restrict who views calculations and employee information.

Audit trail functionality supports compliance. The software must track all assumption changes, calculation runs, and report modifications. Auditors increasingly request this documentation during reviews.

Calculation transparency helps users understand results. The best systems show how they arrive at defined benefit obligations and service costs. Black box calculations create audit challenges when questions arise.

Technical support quality varies significantly between vendors. Evaluate whether the provider offers actuarial consulting alongside software licensing. Implementation assistance and ongoing support affect long-term success.

How to Choose Between Software and Consultants in 2026

Start by assessing valuation frequency. Organizations needing monthly or quarterly calculations benefit more from software. Annual valuations only might not justify automation costs.

Evaluate internal capabilities honestly. Do you have staff with actuarial knowledge? Can your IT team handle system implementation? Lacking these resources favors maintaining consultant relationships.

Consider budget structure. Software requires upfront investment and ongoing subscriptions. Consultants bill per engagement. Calculate total cost over three to five years for fair comparison.

Think about control priorities. Software gives you direct access to calculations and instant scenario testing. Consultants provide professional judgment but take longer for assumption changes.

Review your reporting timeline pressure. Tight financial close deadlines favor automation speed. More flexible reporting schedules accommodate consultant timeframes.

Assess data quality and system capabilities. Clean employee data and modern HR systems make software implementation easier. Legacy data or disconnected systems complicate automation.

Multi-year planning helps decision making. Organizations growing rapidly or adding pension plans should consider future needs. Software scales more easily than consultant relationships as complexity increases.

Some organizations pilot both approaches. Run parallel calculations using software and consultants for one cycle. Compare results, timeline, and cost before making long-term commitments.

Frequently Asked Questions

What’s the typical implementation timeline for pension valuation software?

Implementation usually takes 2 to 4 months. This includes HR system integration, data validation, assumption setup, and user training. Organizations with clean data and modern HR platforms finish faster.

Can small organizations justify the cost of automating employee benefit calculations?

Small organizations should evaluate based on valuation frequency. Companies running quarterly calculations or managing multiple small plans often benefit. Annual valuations only might not justify software costs unless growth is planned.

How do automated systems handle gratuity valuation requirements?

Software for gratuity valuation applies the same automation principles. Systems calculate end-of-service benefits based on salary, tenure, and applicable regulations. This works particularly well for organizations in GCC markets with standardized gratuity rules.

What happens if actuarial assumptions need changing mid-year?

Software lets you update assumptions instantly and rerun calculations. The system maintains version history showing which assumptions applied when. Consultants require new engagement cycles for assumption changes.

Do auditors accept automated pension valuations without consultant involvement?

Auditors focus on methodology correctness and assumption appropriateness. Software-generated valuations with qualified actuarial certification meet audit requirements. Some organizations retain consultants for assumption review to provide additional assurance.

How does pension actuarial valuation software handle plan amendments?

Most systems let you model plan changes before implementation. You can test impact of benefit improvements, early retirement programs, or other amendments. The software recalculates obligations based on modified provisions.

Moving Forward with Your Pension Valuation Approach

Organizations face different circumstances when choosing between pension actuarial valuation software and traditional consultants. Neither approach wins universally. Your decision should reflect valuation frequency, internal capabilities, budget structure, and control preferences.

Software delivers speed, consistency, and scalability. You gain instant scenario testing and compressed reporting timelines. Organizations with frequent valuations or multiple entities find clear value here.

Consultants provide professional judgment and hands-off service. They handle assumption selection and bring industry expertise. Organizations with annual valuations only or limited internal resources often prefer this approach.

Hybrid models combine both strengths. Use software for routine calculations while retaining consultants for assumption guidance. This balances cost control with professional oversight.

The pension administration market continues growing as organizations recognize automation value. Technology advances make sophisticated calculations accessible to more finance teams. You don’t need to choose between accuracy and speed anymore.

Prima Consulting helps organizations evaluate their pension valuation needs. Our team reviews your current processes and recommends approaches matching your specific situation. We implement IAS 19 actuarial valuation software for clients choosing automation or provide traditional actuarial services for those preferring consultant support.

Contact Prima Consulting to discuss your pension valuation challenges. We’ll analyze your requirements and suggest solutions that improve accuracy while meeting your timeline and budget constraints.